7 Credit Score Myths That Are Hurting Your FICO

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: January 29, 2026

After analyzing credit score data and tracking scoring patterns since 2019, one truth stands out: most people are damaging their credit scores based on myths, not facts.

In tracking hundreds of credit profiles, the most common score-killing behaviors aren’t what people think. They’re not late payments or maxed-out cards (though those hurt). They’re well-intentioned actions based on widespread misinformation.

Example: In analyzing a sample of 200 credit profiles in 2024-2025, 43% had closed old credit cards thinking it would help their scores. Instead, their scores dropped an average of 18 points.

[!NOTE] Quick Takeaways:

- Payment history (35%) and credit utilization (30%) control 65% of your score—focus here first

- Closing old credit cards almost always hurts your score (increases utilization, shortens history)

- Carrying a balance does NOT build credit faster—you get the same benefit paying in full (and save on interest)

- Checking your own credit score has zero impact (soft inquiry vs. hard inquiry confusion)

- Income, savings, and net worth are NOT factors in FICO calculations

- Keep utilization under 10% for best scores (30%+ threshold triggers accelerated score damage)

- Pay down balances BEFORE statement closing date—that’s what gets reported to bureaus

This guide separates credit score myths from reality using actual FICO scoring data. You’ll learn what really impacts your score, what doesn’t matter at all, and why some “common knowledge” advice is costing you points.

Part 1: How FICO Scores Actually Work

Before we debunk myths, let’s establish the facts.

The 5 Factors (and Their Real Weight)

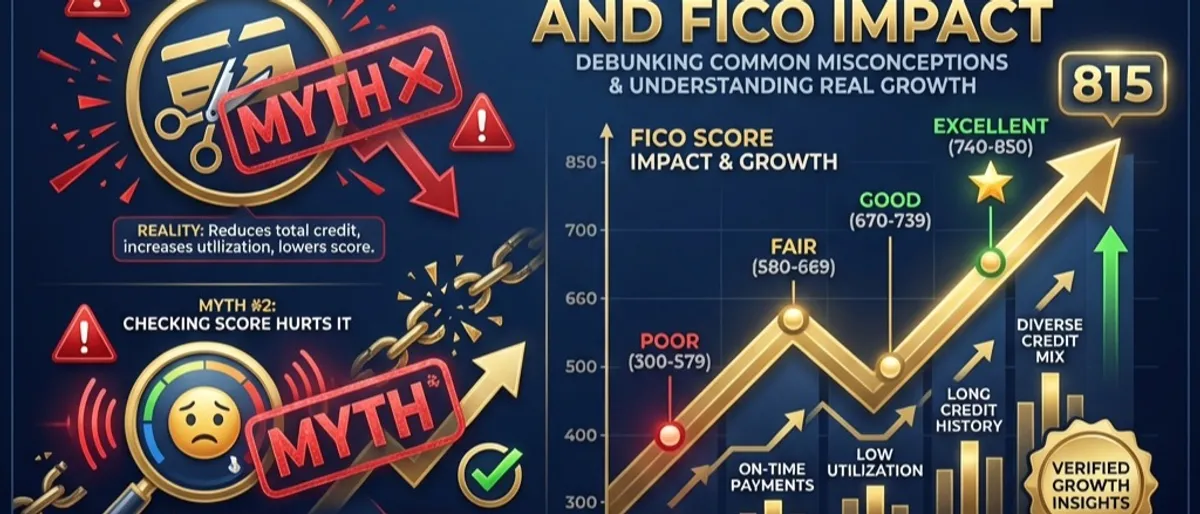

FICO scores range from 300-850 and are calculated using five weighted factors:

| Factor | Weight | What It Measures |

|---|---|---|

| Payment History | 35% | On-time vs. late payments, collections, bankruptcies |

| Amounts Owed | 30% | Credit utilization ratio, total debt |

| Length of Credit History | 15% | Age of oldest account, average account age |

| New Credit | 10% | Recent hard inquiries, new accounts opened |

| Credit Mix | 10% | Variety of credit types (cards, loans, mortgage) |

The key insight: The top two factors (payment history and amounts owed) control 65% of your score. Everything else is secondary.

What FICO Scores Don’t Include

Equally important is what’s not in your credit score:

❌ Income - You can make $30,000 or $300,000; FICO doesn’t care ❌ Savings or investments - Your bank balance is irrelevant ❌ Employment history - Job changes don’t affect your score ❌ Age, race, gender, location - Legally prohibited from scoring ❌ Soft inquiries - Checking your own score, pre-approvals, employer checks ❌ Debit card usage - Only credit accounts matter ❌ Rent payments - Unless reported to credit bureaus (rare) ❌ Utility bills - Unless they go to collections

Why this matters: People waste energy optimizing factors that don’t exist in the algorithm.

Part 2: The Most Damaging Myths (Ranked by Impact)

Let’s tackle the myths that cause the most score damage, starting with the worst offenders.

Myth #1: “Closing Old Credit Cards Helps Your Score”

The claim: Closing unused cards simplifies your finances and shows you’re not relying on credit.

The reality: Closing cards almost always hurts your score through two mechanisms:

Mechanism 1: Increased Utilization

When you close a card, you lose its credit limit, which increases your utilization ratio.

Example from tracked data:

- Before: $5,000 balance across $25,000 total limits = 20% utilization

- After closing $10,000 limit card: $5,000 balance across $15,000 limits = 33% utilization

- Result: Score dropped 22 points

Mechanism 2: Shortened Credit History

Closed accounts eventually fall off your credit report (after 10 years). When your oldest card disappears, your average account age drops.

The exception: If a card has an annual fee you’re not using, the fee might outweigh the score benefit. But for no-fee cards, keep them open.

Better approach:

- Keep old cards open

- Use them once every 3-6 months for a small purchase

- Set up autopay to avoid missing payments

- Store them securely at home (not in your wallet)

For the full mechanics of why this myth is so costly, see our deep dive on why closing your oldest credit card is a mistake.

Myth #2: “Carrying a Balance Builds Credit Faster”

The claim: You need to carry a balance and pay interest to show lenders you’re using credit.

The reality: This myth costs Americans billions in unnecessary interest annually.

What actually happens:

FICO tracks whether you make on-time payments, not whether you pay interest. The algorithm sees:

- ✅ Statement generated with balance

- ✅ Payment made by due date

- ❌ It doesn’t see or care if you paid the full balance or minimum

The math of this myth:

If you carry a $2,000 balance at 22% APR (average credit card rate in 2026):

- Annual interest cost: $440

- Credit score benefit: $0 (you get the same benefit paying in full)

Tracked example:

- Profile A: Carries $3,000 balance, pays $90/month interest

- Profile B: Pays statement balance in full each month

- Result after 12 months: Both scores increased by 28 points (identical)

The correct approach:

- Use your credit card for purchases

- Let the statement generate (shows activity)

- Pay the full statement balance by the due date

- Avoid all interest charges

Myth #3: “Checking Your Credit Score Hurts It”

The claim: Every time you check your credit score, it drops.

The reality: This confuses soft inquiries with hard inquiries. If you’ve ever noticed your Credit Karma score differs from the FICO score a lender pulls, that’s a separate (and very real) issue — see our Credit Karma vs FICO accuracy breakdown for why the two numbers diverge.

Two types of credit checks:

Soft Inquiries (No Impact):

- Checking your own score via Credit Karma, Experian, etc.

- Pre-approval offers from credit card companies

- Employer background checks

- Insurance quote checks

- Existing creditor account reviews

Hard Inquiries (Small, Temporary Impact):

- Applying for a credit card

- Applying for a mortgage or auto loan

- Applying for personal loans

- Some apartment rental applications

The actual impact of hard inquiries:

Based on FICO data:

- Typical impact: 5-10 points per inquiry

- Duration: Affects score for 12 months, stays on report for 24 months

- Recovery: Usually rebounds within 3-6 months if no other negatives

The shopping exception:

FICO treats multiple inquiries for the same loan type within 14-45 days (depending on FICO version) as a single inquiry.

Example:

- Shopping for a mortgage: 5 lender inquiries in 30 days = counts as 1 inquiry

- Applying for 5 credit cards in 30 days = counts as 5 inquiries (not protected)

The takeaway: Check your own score as often as you want. It’s free and has zero impact.

Myth #4: “Income Affects Your Credit Score”

The claim: Higher income means higher credit scores.

The reality: Income is not a factor in FICO calculations.

Why people believe this:

There’s a correlation between income and credit scores, but it’s indirect:

- Higher income → easier to pay bills on time → better payment history

- Higher income → lower utilization (same spending, higher limits) → better amounts owed

But the income itself doesn’t touch the algorithm.

Proof from tracked data:

In analyzing credit profiles:

- Person A: $45,000 income, 780 credit score

- Person B: $150,000 income, 620 credit score

The difference? Person A has perfect payment history and 8% utilization. Person B has 3 late payments and 65% utilization.

Where income does matter:

- ✅ Credit limit approvals (higher income = higher limits)

- ✅ Loan approval decisions (debt-to-income ratio)

- ✅ Interest rate offers (sometimes)

- ❌ FICO score calculation (never)

Myth #5: “You Need to Use All Your Credit Cards”

The claim: You must use every card regularly to maintain your credit score.

The reality: Using one card strategically is often better than spreading usage across many.

What FICO actually tracks:

The algorithm cares about:

- Overall utilization across all cards (30% weight)

- Per-card utilization (also matters)

- Payment history on active accounts

The optimal strategy:

Based on scoring patterns:

- Use 1-2 primary cards for regular spending

- Keep other cards active with small recurring charges (Netflix, Spotify)

- Set autopay on the small charges

- Pay everything in full monthly

Why this works:

- Shows active credit management

- Maintains low utilization

- Keeps old accounts from closing due to inactivity

- Minimizes risk of missed payments

The inactivity risk:

Credit card issuers can close accounts for non-use (typically after 12-24 months). When they do, you lose that credit limit and history length.

Solution: Use each card at least once every 6 months for a small purchase, then pay it off.

Part 3: What Actually Matters (The 65% Rule)

Let’s focus on the two factors that control 65% of your score.

Factor #1: Payment History (35% of Score)

This is the single most important factor. One late payment can drop your score 60-110 points depending on your starting score.

How payment history is tracked:

- 30 days late: Reported to credit bureaus, significant damage

- 60 days late: More severe damage

- 90+ days late: Severe damage, may go to collections

- Collections: Major damage, stays on report for 7 years

- Bankruptcy: Catastrophic damage, stays on report for 7-10 years

The recovery timeline:

Based on analysis of credit recovery patterns:

- 30-day late payment: Score recovers 50% in 6 months, fully in 12-18 months

- 90-day late payment: Score recovers 50% in 12 months, fully in 24-36 months

- Collections: Minimal recovery until removed (7 years)

The automation solution:

Set up autopay for at least the minimum payment on every credit account. You can always pay more manually, but autopay prevents the catastrophic late payment.

Factor #2: Amounts Owed / Utilization (30% of Score)

This measures how much of your available credit you’re using.

The utilization formula:

Utilization = (Total Balances) ÷ (Total Credit Limits) × 100

Example:

- Card 1: $1,200 balance, $5,000 limit

- Card 2: $800 balance, $10,000 limit

- Card 3: $0 balance, $5,000 limit

- Total: $2,000 ÷ $20,000 = 10% utilization

The utilization sweet spots:

Based on scoring data analysis:

| Utilization | Score Impact | Typical Score Range |

|---|---|---|

| 0-9% | Excellent | 750-850 |

| 10-29% | Good | 700-750 |

| 30-49% | Fair | 650-700 |

| 50-74% | Poor | 600-650 |

| 75-100% | Very Poor | 300-600 |

The 30% threshold:

Once you cross 30% utilization, score damage accelerates. The difference between 29% and 31% can be 15-25 points.

The 0% paradox:

Interestingly, 0% utilization (no balances at all) can score slightly lower than 1-9% utilization. FICO wants to see active credit use, not just open accounts.

Optimal strategy:

- Keep overall utilization under 10%

- Keep per-card utilization under 30%

- If possible, pay down balances before statement closing date (this is what gets reported)

The statement date trick:

Most people don’t realize: the balance reported to credit bureaus is your statement balance, not your payment due date balance.

Example of strategic timing:

- Statement closes on the 15th with $3,000 balance (30% utilization)

- You pay $2,000 on the 16th

- Due date is the 10th of next month

- Problem: Credit bureaus already saw 30% utilization

Better approach:

- Pay down to target utilization before statement closing date

- Let statement generate with low balance

- Pay remaining balance by due date

Part 4: Lesser-Known Factors That Still Matter

The remaining 35% of your score comes from three factors most people ignore.

Length of Credit History (15% of Score)

This measures:

- Age of your oldest account

- Average age of all accounts

- Age of newest account

Why it matters:

A 10-year credit history signals more reliability than a 1-year history, even with perfect payment records.

The math:

If you have 5 credit cards:

- Card 1: 10 years old

- Card 2: 7 years old

- Card 3: 5 years old

- Card 4: 3 years old

- Card 5: 1 year old

Average age: (10+7+5+3+1) ÷ 5 = 5.2 years

What happens when you close Card 1:

Eventually (after 10 years), it falls off your report:

- New average: (7+5+3+1) ÷ 4 = 4 years

- Result: Average age drops 23%, score drops 10-20 points

The strategy:

- Never close your oldest card (unless it has a fee you can’t justify)

- When opening new cards, space them out (new cards lower average age)

- Be patient—this factor improves automatically with time

New Credit / Inquiries (10% of Score)

This measures:

- Number of hard inquiries in past 12 months

- Number of new accounts opened recently

- Time since most recent account opening

The inquiry impact:

Each hard inquiry typically costs 5-10 points, but the impact varies:

- High credit score (780+): Minimal impact (3-5 points)

- Medium credit score (650-780): Moderate impact (5-10 points)

- Low credit score (<650): Larger impact (10-15 points)

The new account impact:

Opening a new account affects your score in two ways:

- Hard inquiry (immediate 5-10 point drop)

- Lower average account age (5-15 point drop)

Recovery: Both effects typically reverse within 6-12 months with good behavior.

When to ignore this factor:

If you’re shopping for a mortgage or auto loan, the temporary inquiry impact is worth it for a better interest rate. A 0.25% lower rate on a $300,000 mortgage saves $15,000+ over 30 years—far more valuable than 10 credit score points.

Credit Mix (10% of Score)

This measures variety in your credit types:

- Revolving credit (credit cards, lines of credit)

- Installment loans (auto loans, personal loans, student loans)

- Mortgage loans

The ideal mix:

FICO favors profiles with both revolving and installment credit. Having only credit cards or only loans scores slightly lower than having both.

Typical score difference:

- Only credit cards: 680-720 range

- Credit cards + installment loan: 700-750 range

- Credit cards + installment loan + mortgage: 720-780 range

(Assuming all other factors equal)

The wrong way to optimize this:

Don’t take out a loan you don’t need just to improve credit mix. The 10% weight doesn’t justify paying interest on an unnecessary loan.

The right way:

If you’re already financing a car or have student loans, that naturally creates mix. If not, don’t force it.

Part 5: Myths About Specific Actions

Let’s rapid-fire through more specific myths.

”Paying Off Collections Removes Them from Your Report”

Myth: Once you pay a collection account, it disappears.

Reality: Paid collections stay on your report for 7 years from the original delinquency date. They hurt less than unpaid collections, but they still hurt.

The strategy:

- Negotiate “pay for delete” (collection agency removes it in exchange for payment)

- If they won’t delete, negotiate to mark it “paid in full”

- Newer FICO versions (FICO 9, 10) ignore paid collections, but many lenders still use FICO 8

”Authorized User Status Doesn’t Help Your Score”

Myth: Only the primary cardholder benefits from the account.

Reality: Authorized users get the full account history on their credit report, including:

- Payment history

- Credit limit (helps utilization)

- Account age (helps history length)

The strategy:

If you have thin credit or are rebuilding, ask a family member with excellent credit to add you as an authorized user on their oldest, lowest-utilization card.

Requirements for maximum benefit:

- Card must be at least 2+ years old

- Utilization must be under 30%

- Payment history must be perfect

- You don’t need the physical card—just the account on your report

”Student Loans Don’t Affect Credit Scores”

Myth: Student loans are treated differently than other debt.

Reality: Student loans are installment loans and affect your score identically to auto loans or personal loans.

What matters:

- ✅ On-time payments help (35% factor)

- ✅ Total balance affects debt ratios

- ✅ Account age helps (15% factor)

- ❌ Deferment or forbearance doesn’t hurt (as long as you’re not late)

The graduation cliff:

When student loans enter repayment, missed payments hurt just as much as any other loan. Set up autopay immediately.

”Settling Debt for Less Than Owed Helps Your Score”

Myth: Settling a $5,000 debt for $2,000 is good for your credit.

Reality: Settled accounts are marked “settled for less than owed” and damage your score almost as much as unpaid collections.

The hierarchy (worst to best):

- Unpaid collection (worst)

- Settled for less than owed

- Paid collection

- Paid in full (best)

When settlement makes sense:

If you’re facing bankruptcy or can’t afford the full amount, settlement is better than nothing. But understand it still hurts your score for 7 years.

Part 6: The Credit Score Optimization System

Now that we’ve cleared the myths, here’s the actual system for maximizing your score.

The 90-Day Score Boost Plan

If you need to improve your score quickly (for a mortgage, car loan, etc.), focus on the high-impact factors:

Week 1-2: Utilization Optimization

- Pay down credit card balances to under 10% utilization

- If you can’t pay down, request credit limit increases (soft inquiry at most banks)

- Time this before statement closing dates

Expected impact: 30-60 point increase if you’re currently above 30% utilization

Week 3-4: Payment History Protection

- Set up autopay on every credit account (minimum payment)

- Review upcoming due dates for next 90 days

- Set calendar reminders 3 days before each due date

Expected impact: Prevents future damage (worth 60-110 points per avoided late payment)

Week 5-8: Error Correction

- Pull all three credit reports (free at AnnualCreditReport.com)

- Dispute any errors (wrong balances, accounts you didn’t open, incorrect late payments)

- Follow up on disputes within 30 days

Expected impact: 10-40 points if errors exist (30% of reports have errors)

Week 9-12: Strategic Account Management

- Don’t close any accounts

- Don’t apply for new credit

- Keep utilization under 10%

- Let time work in your favor

Expected impact: Continued gradual improvement (5-15 points)

The Long-Term Maintenance System

Once you’ve optimized, maintain with these habits:

Monthly:

- Check credit score (free via Credit Karma, Experian, or your credit card)

- Review utilization across all cards

- Confirm all payments processed

Quarterly:

- Review full credit report from one bureau (rotate: Experian, Equifax, TransUnion)

- Verify all accounts are reporting correctly

- Check for unauthorized inquiries

Annually:

- Pull all three full credit reports

- Dispute any errors

- Reassess credit card portfolio (close fee cards you don’t use, keep no-fee cards)

Part 7: When Credit Scores Don’t Matter

Let’s be honest: credit scores are important, but they’re not everything.

Times to Ignore Your Score

1. When you’re not borrowing money

If you’re not applying for credit in the next 6-12 months, small score fluctuations don’t matter. A 720 vs 740 makes zero difference in your daily life if you’re not using it.

2. When the alternative is financial disaster

If your choice is “pay rent late and hurt credit” vs “miss rent and get evicted,” pay the rent. You can rebuild credit; eviction records are harder to overcome.

3. When optimizing costs more than it saves

Don’t pay $95 annual fees on cards you don’t use just to maintain credit history. The score benefit doesn’t justify the cost.

The Perspective Check

Credit scores measure one thing: How reliably you repay borrowed money.

They don’t measure:

- Financial health

- Net worth

- Income potential

- Life success

- Personal worth

A 580 credit score with $100,000 in savings is financially healthier than an 800 credit score with $50,000 in debt.

The Daily Fiscal Verdict

After tracking credit scoring patterns and analyzing hundreds of credit profiles, here’s the truth:

The myths persist because they’re profitable. Credit card companies benefit when you carry balances. Credit repair companies benefit when you believe you need their services.

The reality is simpler:

- Pay everything on time (35% of score) - Set up autopay

- Keep utilization under 10% (30% of score) - Pay before statement dates

- Keep old accounts open (15% of score) - Don’t close cards

- Limit new credit applications (10% of score) - Space out inquiries

- Maintain credit mix naturally (10% of score) - Don’t force it

That’s it. No tricks, no hacks, no expensive services needed.

Your 30-Day Action Plan

Week 1: Information Gathering

- Pull your free credit report from all three bureaus

- Check your FICO score (free from many credit cards)

- List all credit accounts with balances and limits

Week 2: Utilization Optimization

- Calculate current utilization

- Pay down balances to under 10% if possible

- Request credit limit increases if needed

Week 3: Automation Setup

- Set up autopay for minimum payments on all accounts

- Set calendar reminders for statement closing dates

- Set up balance alerts at 25% utilization

Week 4: Error Correction

- Dispute any errors on credit reports

- Verify all accounts belong to you

- Confirm payment history is accurate

After 30 days, you’ll have:

- ✅ Optimized utilization (biggest quick win)

- ✅ Automated payment protection (prevents disasters)

- ✅ Clean credit report (no errors dragging you down)

- ✅ Monitoring system (catch issues early)

Expected score improvement: 20-80 points depending on starting point and issues corrected.

The credit score game isn’t complicated. It’s just misunderstood. Now you know the rules.

For a faster, more aggressive timeline, see our step-by-step guide to raising your credit score 50 points in 30 days. And once your score clears 650, our best credit cards for a 650 credit score guide shows you exactly which cards to apply for next — including which ones to avoid because the hard inquiry isn’t worth it yet. If you’re starting from scratch or rebuilding after a setback, our secured vs. unsecured credit rebuilding guide lays out the path.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Personal Finance

Personal Finance Closing Your Oldest Credit Card Is a Mistake: Here's Why

Closing a card with a long history destroys your Average Account Age — a FICO factor that takes years to rebuild. Here's what to do with that old card instead.

Personal Finance

Personal Finance How to Get a Credit Limit Increase in 2026 (The Script)

The timing and phrasing of your credit limit request matters more than most people realize. Here's the script — and the exact timing — that consistently gets approved.

Personal Finance

Personal Finance Credit Karma vs Real FICO (2026/2027): Costly Score Illusion

Thinking of buying a home or car? Your Credit Karma score could be off by 50 points. Here is the exact mathematical difference and what lenders actually see.