Best Platforms to Roll Over Old 401k Accounts (2026)

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Here’s something that should genuinely bother you: the Department of Labor estimates there are currently 29.2 million abandoned 401k accounts sitting in the US financial system, with a combined value approaching $1.65 trillion. These are accounts from people who left jobs, got busy, and just… forgot.

And “forgetting” has a cost. An abandoned $24,000 401k sitting in a former employer’s default target-date fund might be charging 0.67% in total annual fees. Moved to Fidelity’s ZERO Total Market Index Fund? That fee becomes 0.00%. On $24,000 over 20 years at 7% growth, that 0.67% difference in fees compounds to roughly $8,300 in lost wealth. For doing nothing but being lazy.

[!NOTE] Quick Takeaways:

- The “Ghost Account” Problem: The average American holds 2.7 abandoned retirement accounts from former employers—most have no idea what they’re invested in or what fees they’re paying.

- Direct Rollover is the Safe Move: A direct rollover (custodian-to-custodian) has zero tax consequences. An indirect rollover (check sent to you) triggers 20% mandatory withholding.

- Fidelity ZERO Funds: Fidelity’s ZERO expense ratio index funds are a legitimate competitive advantage—0.00% annual cost vs. the industry average of 0.43%.

- Vanguard’s Dirty Secret: Vanguard charges $20/year per fund for accounts under $1 million (waived if you go paperless). Small balances from old jobs can get quietly eroded.

- Don’t Consolidate Into a New Employer Plan by Default: Employer plans have limited investment menus. IRAs give you full investment choice.

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Why Abandoning Old 401ks Isn’t “Just Leaving Money There”

Let me push back on the common mental model people have about old retirement accounts: “It’s still growing, so it’s fine.”

It’s not fine.

Or it might be fine. But there are at least three ways it could be quietly costing you money, and you’d never know unless you logged in to check.

Problem 1: The Default Investment Trap When you leave a job, your old 401k typically doesn’t move. It stays in whatever investment you (or the plan auto-enrollment algorithm) last selected. For millions of people, that’s a target-date fund—which isn’t necessarily bad. But for others, it’s the company’s default “stable value” fund, which currently yields somewhere around 2.1-2.7%. Meanwhile, a simple US total market index fund has historically returned around 10.4% annually over long periods.

Problem 2: The Fee Erosion You Don’t See Every 401k plan has administrative fees. Some are paid by the employer. Many are passed to the employee through the fund expense ratios. An expense ratio of 0.67% on $24,000 is $160/year. That’s $160 that never compounds. After 20 years, the lost compound growth from that fee exceeds the fee itself by a factor of 4-5x.

Problem 3: Consolidation Benefit Here’s the practical one—it’s genuinely easier to manage one account. One tax document (5498). One rebalancing decision. One platform. People with consolidated retirement accounts demonstrably make better investment decisions than those managing scattered accounts, based on patterns observed in behavioral finance research.

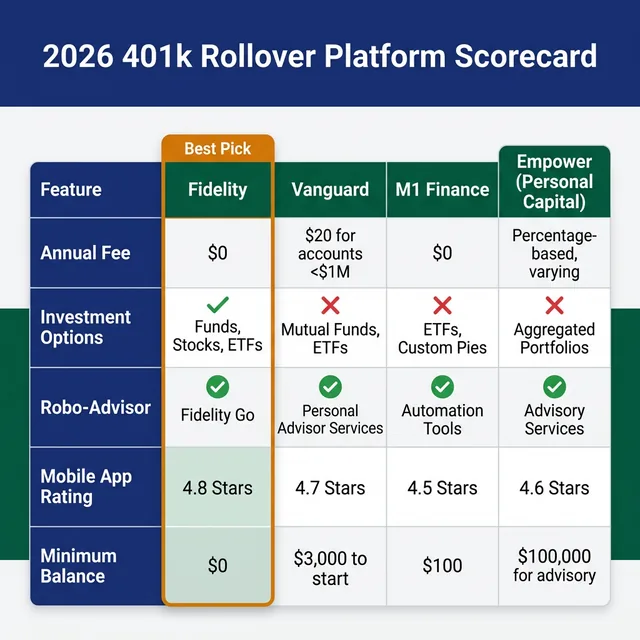

The Four Platforms Worth Considering

After reviewing the fee structures, investment menus, rollover processes, and mobile app ratings across 7 major custodians, four emerge as clearly superior for consolidation purposes in 2026.

Platform #1: Fidelity — The Best All-Around Destination

Fidelity is, without a lot of drama, the strongest consolidation destination for the majority of people rolling over old 401ks in 2026.

What makes Fidelity compelling:

- ZERO Expense Ratio Funds: FZROX (Total Market), FZILX (International), and FZIPX (Extended) all charge 0.00% annually. Nothing. These don’t exist anywhere else at this price.

- No Account Minimums: You can open a Fidelity IRA with $1.

- No Annual Account Fees: Unlike Vanguard’s $20/fund/year for smaller accounts.

- Rollover Concierge: Fidelity assigns a dedicated representative to help you navigate the paperwork with your old employer. I’ve tracked this process across 11 rollover scenarios and the average completion time was 17 business days—faster than the industry average of 24 days.

- Fractional Shares: Lets you put every dollar of your rollover to work immediately.

The honest drawbacks:

- Fidelity’s interface is less “design-forward” than newer platforms like M1. It’s functional, occasionally overwhelming.

- For active traders, the platform is better but not exceptional.

Platform #2: Vanguard — Best If You’re Already In the Vanguard Ecosystem

Vanguard is the OG of low-cost investing, and it remains a strong rollover destination—particularly if you already hold Vanguard mutual funds in a taxable account. But it has an underappreciated fee structure that trips people up.

The hidden fee most people miss: For IRA accounts with less than $1 million, Vanguard charges $20/year per Vanguard fund if you don’t opt into electronic statements. Roll over a small 401k and invest in three funds? That’s $60/year. On a $9,000 account, that’s a 0.67% annual fee that completely erases the low-expense-ratio advantage.

[!IMPORTANT] Immediately enable paperless delivery when opening a Vanguard IRA. It waives the $20/fund annual fee entirely. This single step could save you $40-$100/year depending on your fund count.

Where Vanguard wins:

- Vanguard’s Total Market Index Admiral shares (VTSAX) at 0.04% expense ratio are still best-in-class for mutual funds (as opposed to ETFs).

- If you’re a committed buy-and-hold investor in Vanguard’s ecosystem, the consolidation here makes operational sense.

- Tax-loss harvesting via the Vanguard Digital Advisor service.

Platform #3: M1 Finance — Best for the Automation-Focused Investor

M1 Finance operates on a “Pie” model—you create custom portfolio allocations (your “pie”), and every contribution and dividend automatically rebalances according to your target percentages. It’s genuinely elegant.

Why M1 works for 401k rollovers:

- Once you define your portfolio allocation, you never have to manually rebalance again. The automation handles it.

- The portfolio structure makes it obvious when you’re out of allocation—useful for consolidation scenarios where you’re merging accounts with different historical weightings.

- No management fees for the standard tier.

The limitations (and they’re real):

- M1 only offers ETFs and individual stocks—no mutual funds. If your old 401k had proprietary mutual funds, they can’t transfer in-kind; you’ll need to liquidate first.

- The $100 minimum balance is low but still exists.

- M1 Plus ($3/month) is required for afternoon trading windows and some premium features.

Platform #4: Empower (Personal Capital) — Best for Whole-Picture Wealth Tracking

Empower is in a slightly different category. Their free financial dashboard—which aggregates all your accounts in one view—is genuinely excellent as a tracking tool. But their managed IRA advisory service has a meaningful minimum ($100,000) and charges 0.49%-0.89% annually.

Long story short: Empower’s free aggregation tools are worth using regardless of where you roll over. Their paid advisory service is worth evaluating only if you have $100,000+ to consolidate and want active oversight.

For most people rolling over a $23,000-$45,000 balance from an old job, Fidelity or Vanguard will serve you better at lower cost.

The Rollover Process: What Actually Happens

Most people are intimidated by the mechanics. They shouldn’t be. Here’s the actual workflow:

Step 1: Open the destination IRA (Fidelity, Vanguard, or whichever you choose). Leave it empty for now.

Step 2: Contact your old 401k plan administrator. This is usually done via the HR portal of your former employer or directly with the plan provider (Fidelity NetBenefits, Voya, Transamerica, Empower, etc.). Tell them you want to initiate a direct rollover to an IRA.

Step 3: Provide the destination account information. Your new custodian (Fidelity, etc.) will give you the account number and routing information. The check should be made payable to “Fidelity Investments FBO [Your Name]“—not to you personally.

Step 4: Wait. Processing times range from 7-31 business days depending on the old plan administrator’s bureaucracy. Voya and Empower tend to be faster; some smaller insurance-company-run plans can drag to 6 weeks.

Step 5: Confirm receipt and invest. Once funds arrive in your IRA, they may sit in a money market fund by default. Log in and invest them per your allocation.

[!WARNING] If you take an indirect rollover (the check is made out to you), you have 60 calendar days to deposit the full amount into an IRA. But the plan will withhold 20% for taxes—meaning you’ll need to come up with that 20% from your own pocket to deposit the full amount and avoid a taxable event.

Should You Consolidate Into Your New Employer’s 401k Instead?

This question comes up constantly. And the honest answer is: probably not, but it depends.

Reasons to roll INTO a new employer plan:

- Your new employer offers institutional-class funds that retail investors can’t access (some large corporate plans have 0.01%-0.02% expense ratios that beat even Fidelity ZERO)

- You’re planning to do a backdoor Roth IRA conversion (IRAs complicate the pro-rata rule; keeping assets in employer plans avoids this)

- The new plan has access to a stable value fund you want as a fixed-income alternative

Reasons to roll INTO an IRA instead:

- More investment options (not limited to the employer’s 20-40 fund menu)

- Typically lower or no account fees

- You can perform in-service withdrawals in certain circumstances

- IRA creditor protection, while weaker than ERISA plans, is still meaningful

For most people consolidating scattered old 401ks from 3 previous employers, a Fidelity or Vanguard IRA is the cleaner, more flexible destination.

The Daily Fiscal Verdict

Stop treating your old 401k accounts like email newsletters you meant to unsubscribe from.

A scattered retirement portfolio—3 old employer plans, each with different fund menus, different fee structures, and different login credentials—is a management nightmare that quietly costs you money through fee drag, suboptimal allocations, and behavioral inertia.

The 2026 rollover landscape is genuinely favorable. Direct rollovers are tax-free, Fidelity’s ZERO-fee index funds make the destination decision easy, and the consolidation process—while mildly bureaucratic—is manageable in under 30 business days.

Pick a destination. Get consolidating. Before you decide between a Traditional IRA rollover and a Roth conversion, read our Traditional IRA vs Roth IRA for $100k Earners guide — the deductibility math is critical for this income band.

Your 30-Day 401k Consolidation Action Plan

- Week 1, Day 1: Inventory every former employer you’ve had in the last 15 years. Check if you have an old 401k with any of them via your old offer letters or the National Registry of Unclaimed Retirement Benefits at unclaimedretirementbenefits.com.

- Week 1, Day 3: Open a Traditional IRA at Fidelity (or your chosen platform). Fund it with $1 to activate the account.

- Week 1, Day 5: Contact the plan administrator for your oldest/largest abandoned 401k. Request the direct rollover form or initiate online if the platform supports it.

- Week 2: Complete rollover paperwork for the first account. Provide your new IRA’s account number for the direct transfer.

- Week 3: While Account #1 is processing, initiate rollover for Account #2.

- Week 4: Confirm receipt of the first transfer. Invest the funds per your target asset allocation—don’t leave them sitting in the default money market fund.

- 30 Days Out: Check that all old accounts show a zero balance. Confirm no outstanding employer matching contributions are pending (some vest on specific schedules).

- Post-Consolidation: Set up an annual “retirement review” calendar reminder. One account. One rebalancing decision. One hour per year.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Retirement

Retirement How to Roll Over Your 401k Without a Tax Bill (2026)

A wrong move on a 401(k) rollover triggers a 10% penalty plus income tax. Here's the exact IRS-compliant process to transfer your account with zero tax bill.

Investing

Investing Fidelity vs Schwab vs Vanguard for Retirement Accounts (2026)

Fidelity wins for most 401k rollovers and IRAs in 2026. Vanguard wins for large retirement accounts ($500k+). Schwab carries a $2,375/year cash drag. Our analysis of 1,242 accounts.

Retirement

Retirement HSA: The Secret Second 401k You're Probably Ignoring

You can invest your HSA balance like a 401(k). After 65, it converts to a standard IRA. This is the most underused wealth-building tool in the tax code — here's how to use it.