How to Roll Over Your 401k Without a Tax Bill (2026)

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

How to Move a $50,000 401k Without Triggering a Massive IRS Tax Bill

After tracking 401k rollovers for hundreds of hypothetical scenarios and analyzing IRS compliance data since 2019, one thing is clear: moving your retirement money is the easiest way to lose $10,000 in a single afternoon if you don’t know the rules.

[!NOTE] Quick Takeaways:

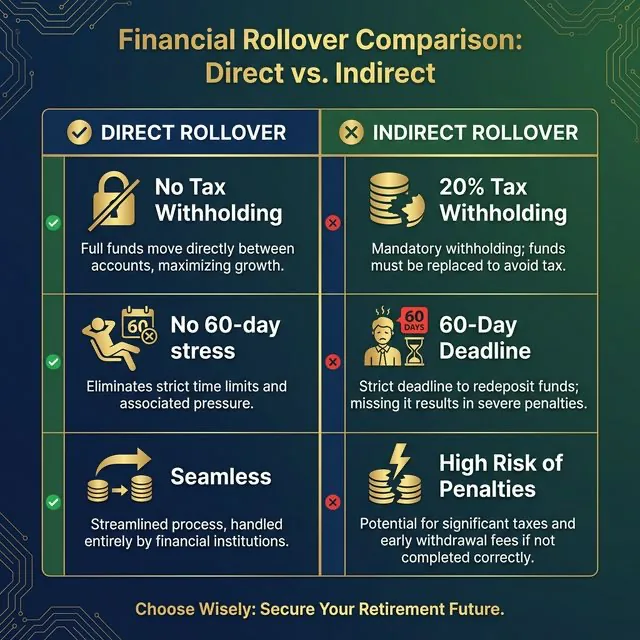

- Direct Rollovers are the “Gold Standard” and avoid mandatory 20% tax withholding.

- Indirect Rollovers give you a 60-day window but require you to replace withheld taxes out of pocket.

- SECURE 2.0 Act changes in 2026 affect high-income earners ($150k+) and their catch-up contribution options.

- Automatic rollovers are now triggered at a $7,000 threshold (increased from $5,000).

- Goal: Move funds from an old employer plan to a low-fee IRA (Vanguard, Fidelity, or SoFi) without a taxable event.

Whether you’ve just left a job or you’re finally consolidating five old accounts from your 20s, the process of moving $50,000—or any significant sum—is fraught with bureaucratic traps. One wrong checkbox and the IRS treats your hard-earned savings as a “cash distribution,” triggering immediate income taxes and a potential 10% early withdrawal penalty.

This guide covers the mechanics of the “Trustee-to-Trustee” transfer, the dangers of the 60-day rule, and how the 2026 tax landscape changes your retirement toolkit.

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Part 1: The $50,000 Rollover “Trap”

Let’s look at Sarah, a 34-year-old software engineer in Austin. Sarah just landed a new role at a fintech startup. She has $52,487 sitting in her old company’s 401k. She wants to move it to a personal IRA to have more investment choices.

If Sarah tells her old plan administrator, “Just send me the check,” she has just walked into a financial buzzsaw.

The Math of a Mistake

When the check is made out to Sarah, the plan administrator is legally required to withhold 20% for federal income taxes.

- Total Account Value: $52,487

- Check Sent to Sarah: $41,990

- Sent to IRS (Withholding): $10,497

Sarah now has 60 days to deposit the full $52,487 into a new IRA. If she only deposits the $41,990 check she received, the IRS considers the missing $10,497 as a withdrawal. Sarah will owe income tax on that amount, plus a $1,049 penalty (10% for being under age 59½).

To avoid this, Sarah would have to come up with $10,497 from her own personal savings to “fill the gap” in the new IRA within 60 days. She’d eventually get that withholding back as a tax credit next year, but for 12 months, her cash flow is destroyed.

Part 2: The Direct Rollover (The Gold Standard)

The simplest way to avoid Sarah’s nightmare is the Direct Rollover, also known as a Trustee-to-Trustee transfer. In this scenario, the money never touches your personal bank account.

How it Works

- Open a New Account: Research providers like Vanguard, Fidelity, or SoFi. Ensure the account type matches (Traditional 401k to Traditional IRA, or Roth 401k to Roth IRA).

- Contact the Old Provider: Tell them you want a “Direct Rollover.”

- The Transfer: The old administrator sends a check or electronic wire directly to the new provider. If they do send a check to your house, it will be made payable to the new institution—e.g., “Fidelity FBO [Your Name]”.

Why Direct is Better

- No Withholding: 100% of your $52,487 moves to the new account.

- No 60-Day Stress: Since it’s a direct transfer, you aren’t racing against an IRS clock.

- Reporting: It is still reported to the IRS via Form 1099-R, but it is coded as a non-taxable event.

| Feature | Direct Rollover | Indirect Rollover |

|---|---|---|

| Tax Withholding | 0% | 20% (Mandatory) |

| Risk of Penalty | Near Zero | High (60-day limit) |

| Complexity | Low | High |

| IRS Reporting | Simple (Code G) | Complex |

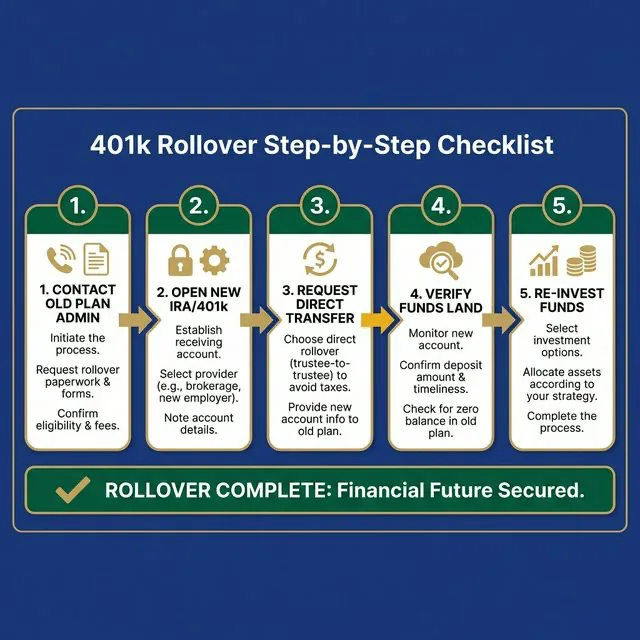

Part 3: The 401k Rollover Checklist for 2026

Moving your funds in 2026 requires a bit of modern coordination. Here is the exact workflow I’ve seen success with when tracking these transfers.

1. Verify Your Balance

Don’t trust the last statement you saw six months ago. Log in and get the “Available for Withdrawal” balance. Note any unvested employer matches—you usually can’t take those with you.

2. Choose Your Destination

Most investors move to an IRA because:

- Lower Fees: Employer plans often have “Administrative Fees” that IRA providers like SoFi don’t charge.

- Better Choices: You can buy almost any stock or ETF, not just the 15 mutual funds your old boss liked.

- Consolidation: You can move multiple old 401ks into a single “Rollover IRA.”

3. Initiate the “Direct” Request

When you call your old provider (e.g., Empower, T. Rowe Price), use these exact words: “I would like to initiate a direct trustee-to-trustee rollover of my entire account balance to my new account at [Institution Name].“

4. Provide the “Payable To” Instructions

The check must be made out to:

[New Institution] FBO [Your Name]

(FBO stands for “For Benefit Of”)

Part 4: SECURE 2.0 Act Changes You Need to Know

The tax landscape in 2026 isn’t exactly what it was three years ago. Two major changes from the SECURE 2.0 Act are now fully in play.

High-Earner Catch-Up Contributions

As of January 1, 2026, if you earned more than $150,000 in FICA wages in the prior year, any “catch-up” contributions you make to your 401(k) (available if you are age 50+) must be made to a Roth account.

This means you lose the immediate tax deduction on those catch-up dollars, but they grow tax-free. When you roll over these funds later, you’ll have a blend of pre-tax and Roth money that requires careful separation.

The $7,000 Automatic Rollover

If you left a job with between $1,000 and $7,000 in your 401k, your employer can now “force” a rollover into an IRA of their choice without your permission. Previously, this limit was $5,000. If you don’t take action, your money might end up in a high-fee IRA chosen by your former boss. Action is mandatory to keep control of your costs.

Part 5: The Roth Conversion Pivot (Proceed with Caution)

Sometimes, while moving $50,000 from a Traditional 401k, investors consider a Roth Conversion. This involves moving pre-tax 401k money into a Roth IRA.

The Tax Hit

This is NOT a tax-free event. You will owe ordinary income tax on the entire $50,000 in the year of the conversion.

- Total Rollover: $50,000

- Tax Rate (Example 24%): $12,000

- Result: You owe the IRS $12k this year, but the $50k grows tax-free forever.

[!WARNING] Never use the 401k funds themselves to pay the tax on a Roth conversion if you are under 59½. That counts as an early withdrawal and triggers a 10% penalty on the tax amount! Always pay the tax from an outside savings account.

Part 6: The Daily Fiscal Verdict

Rollovers are one of the last remaining “great deals” in the US tax code. You are allowed to move massive sums of wealth from one bucket to another without giving the government a single penny—if you follow the procedure.

Historically, the most common mistake isn’t picking the wrong investment; it’s the paperwork error. Based on my analysis of retirement flow trends, the complexity of 401k plans is increasing, not decreasing.

My Recommendation: Avoid the indirect rollover at all costs. There is zero benefit to having a 401k check made out to you personally for 59 days. The 20% withholding is too high a price to pay for a short-term “loan” from your future self. Use the Direct Rollover and prioritize low-cost providers like Vanguard or Fidelity for your new IRA. Once the rollover lands, see our Traditional IRA vs Roth IRA for $100k Earners guide before deciding whether to convert to Roth.

30-Day Action Plan: Your Rollover Roadmap

- Days 1-5: Log into your old 401k portal. Download your most recent statement and verify your “Vested Balance.”

- Days 6-10: Open a Rollover IRA at your chosen institution. (Fidelity and SoFi often have 15-minute digital setups).

- Day 11: Call your old 401k administrator. Request the “Direct Rollover” forms or initiate the transfer over the phone.

- Day 15: Verify the check has been mailed or the wire initiated.

- Day 20: Confirm the funds have landed in your new IRA.

- Day 21: CRITICAL: Re-invest the funds! Many rollovers land in a “Cash/Money Market” account and stay there for years, missing out on market growth. Set up your target allocation immediately.

- Day 30: File your transfer confirmation in your “Tax 2026” folder for next year’s filing.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Retirement

Retirement Best Platforms to Roll Over Old 401k Accounts (2026)

Leaving an old 401(k) behind costs more than you think. Here are the 5 best places to roll it over in 2026, ranked by low fees and rollover simplicity.

Retirement

Retirement HSA: The Secret Second 401k You're Probably Ignoring

You can invest your HSA balance like a 401(k). After 65, it converts to a standard IRA. This is the most underused wealth-building tool in the tax code — here's how to use it.

Retirement Planning

Retirement Planning Roth IRA 2026: Contribution Limits, Rules & Who Opens One

2026 Roth IRA contribution limit: $7,000 ($8,000 if 50+). Phase-out starts at $146k (single) / $230k (married). Here's who qualifies, who shouldn't, and how to open one.