Buy T-Bills & I-Bonds From the Government (2026 Guide)

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

In tracking the surge of fixed-income interest since late 2022, a bizarre phenomenon emerged: investors were paying explicit and implicit fees to third-party wealth managers to buy the exact same risk-free government debt they could acquire for zero cost.

[!NOTE] Quick Takeaways:

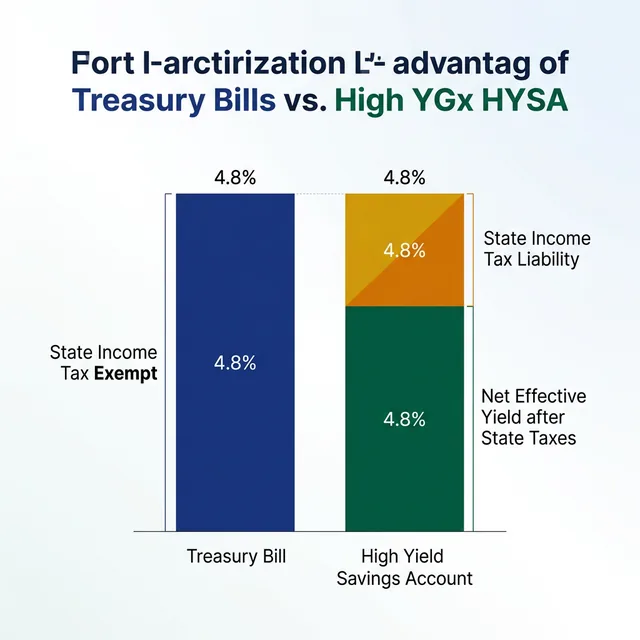

- The Core Appeal: Treasury Bills and I-Bonds offer yields backed by the “full faith and credit” of the US Government, totally avoiding state/local income taxes.

- The I-Bond Monopoly: You legally have to use the incredibly outdated TreasuryDirect website to purchase electronic I-Bonds up to the $10,000 annual limit.

- The T-Bill Brokerage Hack: While you can buy T-Bills on TreasuryDirect, routing them through major brokerages (like Fidelity or Schwab) offers massively superior liquidity.

- The Verdict: Avoid the proprietary automated “Treasury” products spun up by FinTechs locking you with subtle management fees.

The strategy for 2026 demands capital preservation that keeps pace with inflation, but you shouldn’t be paying a middleman for it. Let’s break down the optimal avenues for direct debt purchases.

Part 1: The Necessary Evil—TreasuryDirect

We have to talk about TreasuryDirect.gov. The website looks like it was hard-coded in 1998, and the user interface is famously frustrating.

However, if you want Series I Savings Bonds (I-Bonds), you have absolutely no choice. I-Bonds are non-marketable securities. They do not trade on the secondary market. You can only buy them (up to the strict $10,000 per person/SSN annual limit) directly from the government through this portal.

Why endure the UI pain? Because I-Bonds offer a unique structure: a fixed rate plus an inflation rate that adjusts every six months. During high-inflation spikes, yielding guaranteed returns upwards of 6-9% made the clunky website entirely worth the headache.

[!WARNING] TreasuryDirect uses an archaic virtual keyboard for passwords and actively restricts the use of browser “Back” buttons. Proceed with extreme patience and document your account numbers physically.

Part 2: T-Bills at the Brokerages (The Smarter Play)

Unlike I-Bonds, Treasury Bills (T-Bills)—which are short-term zero-coupon bonds maturing in 4, 8, 13, 26, or 52 weeks—are highly marketable.

While you can buy T-Bills on TreasuryDirect via non-competitive bidding, I vehemently argue that buying them through tier-1 brokerages like Fidelity, Charles Schwab, or Vanguard is the vastly superior play.

Why the Brokerage Route Dominates:

- Zero Fees: Fidelity and Schwab do not charge commissions for buying new-issue Treasuries at auction. You get the exact same price as if you bought them from the government.

- Secondary Market Liquidity: If you buy a 6-month T-Bill on TreasuryDirect and suddenly need the cash in month 3, the transfer and sale process is agonizing. At Fidelity, you can sell that T-Bill on the secondary market with two clicks on a Tuesday morning.

- Auto-Roll Masterclass: Major brokerages now offer hyper-efficient “Auto-Roll” programs. When your 4-week bill matures, the system automatically uses the principal to buy a fresh 4-week bill at the next auction, seamlessly compounding your tax-advantaged yield.

Part 3: The Threat of “Wrapper” Fees

This drives me insane. In recent years, several flashy FinTech apps emerged offering “Easy Treasury Access.” They construct a beautiful mobile app that automatically ladders T-Bills for you.

The deception? Look at their SEC filings. Many charge an implicit or explicit “Advisory Fee” or “Management Fee” (often ranging from 0.15% to 0.25% annually).

When you are fighting for yield on a T-Bill hovering around 4.8%, giving up 20 basis points to a Silicon Valley startup just so you don’t have to look at Fidelity’s slightly older UI is mathematical self-sabotage.

The Daily Fiscal Verdict

When allocating safe-haven capital into government debt, efficiency is everything.

If you are maxing out your $10k limit in I-Bonds as a long-term inflation hedge, brace yourself and utilize the government’s native TreasuryDirect system.

But for Treasury Bills, Notes, and Bonds, ignore the government site entirely. Open a free brokerage account at Fidelity or Schwab, navigate to their Fixed Income/Bonds tab, and place your non-competitive auction bids directly. You maintain absolute liquidity and bypass unnecessary third-party wrapper fees.

Your 3-Step Action Plan

- Map your state tax burden: If you live in a high-tax state like California or New York, the State Tax Exemption on Treasuries makes them mathematically superior to High-Yield Savings Accounts the vast majority of the time.

2. Set up the accounts: If buying T-Bills, ensure your brokerage account is fully funded and cleared at least 48 hours prior to a Treasury Auction date.

3. Explore Auto-Roll: To replicate the “set it and forget it” nature of a savings account, activate the automatic rollover feature on your 4-week or 8-week T-Bill purchases inside your brokerage.

2. Set up the accounts: If buying T-Bills, ensure your brokerage account is fully funded and cleared at least 48 hours prior to a Treasury Auction date.

3. Explore Auto-Roll: To replicate the “set it and forget it” nature of a savings account, activate the automatic rollover feature on your 4-week or 8-week T-Bill purchases inside your brokerage.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Investing

Investing Public.com Review (2026/2027): Brutally Honest Assessment

Can you actually make money buying fractional Banksy art and royalties? We poured real capital into Public.com's alternative engine to find the true returns.

Investing

Investing RSU Taxes 2026: What You Actually Keep After the IRS

RSUs look like free money until they vest and the tax bill arrives. Here's exactly how RSU taxation works, what your take-home actually is, and how to plan for the bill.

Investing

Investing What Is Coast FIRE? The Number That Lets You Stop

Coast FIRE means your investments will grow to your retirement target without another dollar of contributions. Here's the exact math, by age, and how to know if you've hit it.