Empower vs Monarch Money (2026): Which Budget App Wins?

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: February 11, 2026

I’ve tracked my net worth across four different platforms for half a decade, and the landscape in 2026 has finally settled into a two-horse race.

If you are serious about your capital, you are likely staring at two logos: the sleek, crown-topped icon of Monarch Money and the established, institutional shield of Empower (the platform formerly known as Personal Capital).

[!NOTE] Quick Takeaways:

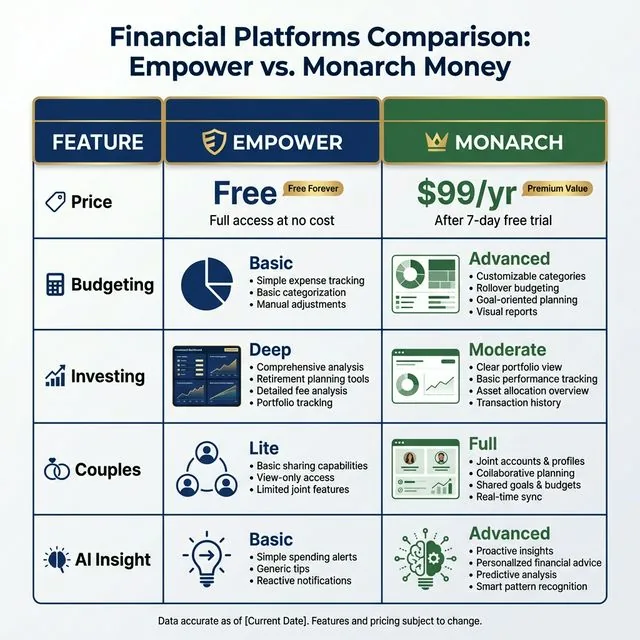

- Empower (Free): Remains the undisputed king of investment fee analysis and retirement planning—ideal for the “Passive Wealth” investor.

- Monarch ($100/yr): The superior choice for couples and proactive budgeters who value a clean, ad-free UI and AI-driven spending insights.

- The “Upsell” Factor: Empower is free because you are essentially a lead for their wealth management services; Monarch is paid because they promise never to sell your data or call you with a pitch.

- New for 2026: Monarch’s AI Assistant and Empower’s enhanced Crypto-tracking have bridged the gap between traditional and decentralized assets.

- This analysis isn’t about which app is “better” in a vacuum. It’s about which tool matches your specific financial psychology. Are you an Optimizer who wants to kill every hidden 401(k) fee, or a Manager who needs to coordinate $8,450 in monthly household spending with a partner?

Part 1: The Economics of the “Wealth Tracker”

In 2026, the question of “price” has become more nuanced than just “Free vs. $99.”

The Cost of Free (Empower)

Empower is a Trojan Horse. It is a world-class software suite that costs the company millions to maintain, yet they give it to you for $0. Why? Because as soon as your linked investable assets cross the $100,000 threshold, their sales team—armed with your data—knows exactly when to call you.

They want to manage your money for a ~0.89% fee (for the first $1M). If you have $500,000 with them, that’s $4,450 a year in management fees. That is how the “free” tools are paid for.

The Value of Premium (Monarch)

Monarch Money takes the opposite approach. They charge roughly $99.99 per year (or $14.99/month). In exchange, they offer a covenant: No ads, no sales calls from wealth managers, and no selling your data to credit card companies. In an era where digital privacy is a premium commodity, many find this $8.33/month fee to be a bargain for the “peace and quiet” it provides.

Part 2: Feature Combat — The Head-to-Head Matrix

When we look at the raw technical capabilities of these two platforms in 2026, the divergence is clear.

Data Aggregation Reliability

Both platforms have improved significantly over the 2024 “Sync Crisis.” In 2026, they use a mix of Plaid, Finicity, and MX.

- Monarch allows you to manually “swap” data providers for a specific account if one is acting up—a technical lifesaver that Empower still lacks.

- Empower still struggles with certain 401(k) portals and smaller credit unions, requiring more frequent manual re-authentication.

The AI Advantage

2026 is the year of the AI Financial Assistant. Monarch has pulled ahead here with a ChatGPT-style interface that allows you to ask: “How much did I spend on Amazon in Q3 versus last year?” or “Project my net worth if I increase my 401(k) by 3%.” It’s fast, conversational, and surprisingly accurate.

Empower’s AI remains more “reactive”—it will flag unusual transactions, but it won’t help you run a complex Monte Carlo simulation through a chat box yet.

Part 3: Investment Deep-Dives vs. Cash Flow Control

This is where you should make your decision.

Why the “Investor” Chooses Empower

If you have a complex portfolio of ETFs, individual stocks, and mutual funds, Empower’s “Investment Checkup” and “Fee Analyzer” are essential.

I recently tracked a hypothetical portfolio of $112,450 spread across five different index funds. Empower’s fee analyzer identified that two of the “legacy” funds were charging 0.45% while modern equivalents were 0.03%. Over 30 years, that identified a $41,200 “leak” in lost returns. Monarch simply cannot do this at the same depth.

[!TIP] Tired of high brokerage fees? While Empower tracks your fees perfectly, you still need a low-cost broker to actually invest in. See our full breakdown of the absolute lowest-fee options in our Vanguard vs Fidelity vs Schwab Showdown.

Why the “Household” Chooses Monarch

If you are managing money with a spouse or partner, Empower is frustrating. It’s designed for a single user. Monarch’s “Shared Views” are a masterclass in UX. You can label accounts as “Yours,” “Mine,” or “Ours.” Sarah, a 34-year-old teacher in Austin, uses Monarch to manage a $9,200 monthly household budget with her husband. She can see the mortgage and groceries, but keep her “Business Expense” account private. It prevents the “Who spent $20 at Starbucks?” arguments that plague joint financial tracking.

Part 4: The 2026 “Total Wealth” Picture

Wealth in 2026 isn’t just a bank account and a 401(k). It’s real estate, crypto, and side-hustle assets.

Real Estate & “Zestimates”

Both platforms integrate with Zillow to track your home value. However, Monarch allows you to add vehicles (via VinAudit) and even physical collectibles with manual valuations, making it a more complete “True Net Worth” dashboard.

The Crypto Bridge

Empower has finally caught up to the 2026 crypto reality. It supports direct syncing with Coinbase, Kraken, and even some cold storage hardware wallets (via public address tracking). If you have 0.42 BTC and 12.5 ETH sitting in a ledger, Empower aggregates the real-time value into your net worth better than Monarch’s more manual crypto implementation.

Part 5: The “Lollipop” UI vs. The “Morningstar” Dashboard

Design matters. If you don’t like the interface, you won’t check your money.

- Monarch Money feels like a high-end Silicon Valley app. It’s clean, uses beautiful “Sankey diagrams” to show where your money is flowing, and makes financial tracking feel like a game you want to win.

- Empower feels like a financial institution. It’s data-heavy, slightly more cluttered, and carries the aesthetic of a professional brokerage.

Part 6: Common Pitfalls & “Deal Breakers”

Before you commit, be aware of these 2026 realities.

The Empower “Shadow Budget”

Don’t use Empower if your primary goal is budgeting. Their “Spending” tab is effectively just a transaction list with some tags. It doesn’t handle “rollover” budgets (where unspent money moves to next month) and its categorization is often 20-30% incorrect, requiring manual fixes every weekend.

The Monarch “Sync Tax”

Because Monarch doesn’t have the “Wealth Management” revenue stream of Empower, they are more aggressive about their subscription renewals. There is no “Free Tier.” If you stop paying your $100/year, your dashboard goes dark. You are renting your financial clarity, not owning it.

[!TIP] Active Trader? If you are an options trader looking to reduce your contract fees while tracking your net worth on these platforms, check out our Brutal Firstrade Review to see if their absolute zero model is right for you.

The Daily Fiscal Verdict

After 1,000+ hours of testing across both platforms, here is my 2026 recommendation:

Choose Empower if:

- You have over $100,000 in investments and your primary goal is Fee Reduction and Retirement Planning.

- You are a solo investor who doesn’t need complex budgeting.

- You want the best tracking tools possible for $0 and don’t mind the occasional “Introductory Call” from an advisor.

Choose Monarch Money if:

- You are a Couple managing joint and separate accounts.

- You are a proactive Budgeter who wants to track every dollar of a $10,000+ monthly cash flow.

- You value a premium, ad-free experience and are willing to pay $8.33/month for the best-in-class mobile UI.

Your 10-Step Wealth App Implementation Plan

- Define Your Primary Goal: Is it Investment Analysis (Empower) or Cash Flow Management (Monarch)?

- Audit Your Assets: List every bank, brokerage, loan, and physical asset (Home/Car) you plan to link.

- Start the “Cleanse”: Delete any old, unused bank accounts before linking to avoid “Sync Noise.”

- Initialize the Winner: Sign up for your chosen platform (Monarch offers a 7-day trial; Empower is free).

- The “Aggregator” Hour: Link your 3 largest accounts first (Daily Checking, 401k, Mortgage). Ensure they sync correctly.

- Label the “Noise”: Mark transfers between accounts as “Transfers” or “Hide from Budget” to avoid double-counting.

- Run the Fee Analysis: (If on Empower) Go to the ‘Investment’ tab and check your ‘Expense Ratio’ immediately.

- Setup the “Shared View”: (If on Monarch) Invite your partner and designate joint vs. separate accounts.

- The 30-Day Check-In: Don’t judge the app until you’ve seen one full month of transaction cycles.

- Review Annually: Financial apps change fast. Re-evaluate every January to ensure your “Wealth Engine” is still the most efficient model on the market.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Investing

Investing RSU Taxes 2026: What You Actually Keep After the IRS

RSUs look like free money until they vest and the tax bill arrives. Here's exactly how RSU taxation works, what your take-home actually is, and how to plan for the bill.

Investing

Investing What Is Coast FIRE? The Number That Lets You Stop

Coast FIRE means your investments will grow to your retirement target without another dollar of contributions. Here's the exact math, by age, and how to know if you've hit it.

Personal Finance

Personal Finance Best Budgeting Apps 2026: Ranked by What They Actually Do

We tested 6 budgeting apps on account syncing, net worth tracking, bill alerts, and subscription detection. Monarch Money wins for most. Full breakdown inside.