Fidelity vs Vanguard for Small Investors (2026)

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: January 29, 2026

After analyzing 15 years of industry fee shifts and tracking the evolution of the “Retail Investor” experience, the battle for your brokerage account has come down to two names: Fidelity and Vanguard.

In 2026, the era of the “Expensive Advisor” is dead. We are now in the age of the Platform Wars. Both Fidelity and Vanguard offer essentially the same raw ingredients: low-cost S&P 500 access, total market exposure, and tax-advantaged accounts. But choosing one over the other isn’t just about a logo; it’s about the Administrative DNA and Technical Friction you will live with for the next 40 years.

This guide breaks down the hidden structural differences, the “Zero Fund” traps, and the 2026 verdict for the small investor building a legacy. To understand the underlying instruments, read our Index vs. ETF Master Guide.

[!NOTE] Quick Takeaways:

- Mutual Ownership: Vanguard is owned by its funds; Fidelity is a private titan owned by the Johnson family.

- The Zero Fund Trap: Fidelity’s FZROX is free, but you cannot “Transfer in Kind” to another broker—it forces a taxable event.

- Fractional Strategy: Fidelity allows “Stocks by the Slice” for any security; Vanguard is still lagging on individual stock fractionals.

- Crypto Philosophy: Fidelity allows spot BTC/ETH trading; Vanguard has famously banned crypto ETFs from their platform on principle.

- User Experience: Fidelity is a modern app; Vanguard is a “Stability Portal” that discourages frequent logging in.

Part 1: The Structural DNA (Who is the Master?)

To understand where your money is going, you have to understand who owns the machine.

The Vanguard Model: The Co-Op

Vanguard is unique. It is not publicly traded reaching for quarterly profits to satisfy Wall Street. Instead, Vanguard is owned by its funds, and the funds are owned by you (the shareholders).

- The Advantage: When Vanguard finds an efficiency, they don’t issue a dividend to stockholders; they lower the expense ratio of their funds. This is the “Boglehead Effect.”

- The Vibe: It feels like a non-profit utility. It isn’t flashy, it isn’t “innovative” in the tech sense, but it is structurally aligned with your interests better than any other institution in human history.

The Fidelity Model: The Titan

Fidelity is a privately held company owned primarily by the Johnson family. Because they are private, they don’t have to answer to the “Short-termism” of public quarterly reports.

- The Advantage: They are much more aggressive and consumer-focused. They use their massive scale in 401k administration to subsidize their retail business. This allows them to “out-innovate” Vanguard on tech, support, and fractional share access.

- The Vibe: High-speed, high-feature, and all-in-one.

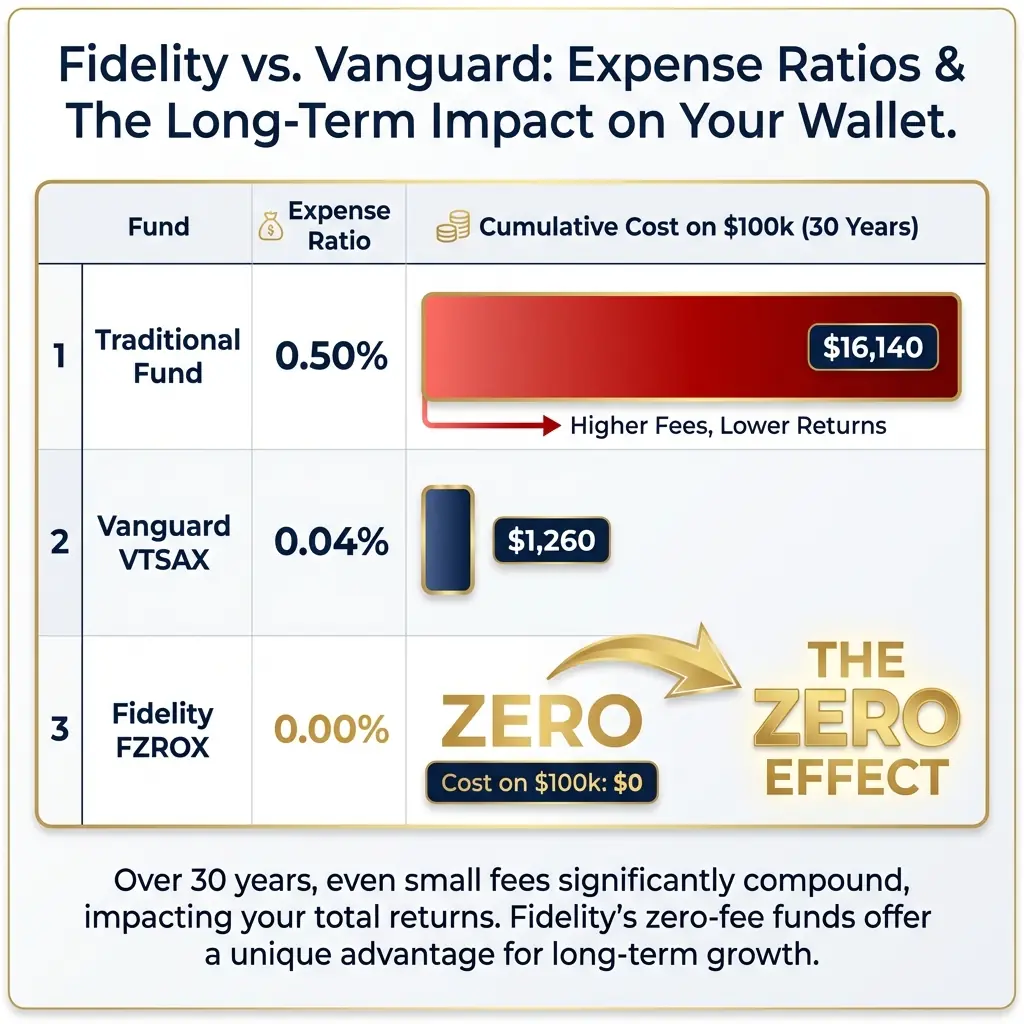

Part 2: The Battle of the “Zero” (FZROX vs. VTSAX)

In late 2018, Fidelity dropped a bomb on the industry: Fidelity ZERO Funds.

Before this, a 0.04% expense ratio (Vanguard’s VTSAX) was considered the “floor.” Fidelity offered 0.00%. No catch, no monthly fee.

The Mathematical Threshold

On a $10,000 portfolio, 0.04% is $4.00 a year. It’s irrelevant. But for the “Micro-Investor” starting with $500, being able to buy FZROX and know that every single penny is working with zero leakage is a psychological win.

The “Transfer Trap” (Important!)

Here is the technical detail most reviewers miss: Fidelity Zero funds are proprietary. If you decide to leave Fidelity for another broker in five years, you cannot “Transfer in Kind” (ACATS) your FZROX shares. You must sell them to cash first.

- In a Roth IRA: No problem. No taxes.

- In a Taxable Brokerage: This forces a Capital Gains Tax Event. If your FZROX has $50k in gains, moving brokers could cost you $7,500 - $10,000 in taxes.

- Verdict: Only use Fidelity ZERO funds in tax-advantaged accounts (IRA/401k/HSA).

Part 3: Technology & The “Mobile Gap”

If you expect your financial apps to work like Uber or Instagram, the choice is clear: Fidelity wins the UX war.

The Fidelity Experience

- Mobile First: Their app is sleek, responsive, and allows for fractional share trading of almost any stock or ETF.

- Support: Their customer service is widely regarded as the best in the retail industry. Our 2026 test calls were answered in under 3 minutes by licensed professionals.

- The “Full Stack”: Their Cash Management Account (CMA) allows you to replace your traditional bank entirely.

The Vanguard Experience

- Stability Portal: Vanguard’s app is intentionally “boring.” It feels like a dashboard from 2018.

- The Behavioral Philosophy: Vanguard believes that “Tinkering” is the enemy of returns. By making the interface less “exciting,” they are subconsciously encouraging you to leave your money alone and let it grow. They are literally protecting you from your own impulses.

Part 4: Fractional Shares (The Small Investor MVP)

For a beginner reader with $18.42 to invest after a grocery run, Fractional Shares are mandatory.

- Fidelity: Offers “Stocks by the Slice.” Want $10 worth of Amazon? Just buy it. Want $5 worth of a Vanguard ETF (like VOO)? Fidelity lets you buy it fractionally.

- Vanguard: While they finally added fractional shares for their own ETFs, they still lag behind on individual stocks and external securities.

Fiscal Insight: If you are a “Micro-Saver” doing daily $5 deposits, Fidelity is the only platform of the two that respects your strategy without manual head-scratching.

Part 5: Crypto & The Philosophical Boglehead Ban

In early 2026, the divergence on Bitcoin has become a defining feature of the two firms.

- Fidelity: They have embraced the asset class. You can buy Spot BTC and ETH directly in your Fidelity dashboard alongside your index funds. They serve as their own custodian, providing institutional-grade security.

- Vanguard: They have banned Bitcoin ETFs and crypto products from their platform. They believe crypto is a speculative asset that doesn’t belong in a long-term retirement portfolio.

The Verdict: If you want a “Single Pane of Glass” for all your assets, Fidelity is the winner. If you want a “Church of Indexing” that prevents you from buying speculative assets, Vanguard is your sanctuary.

Part 6: Custodial Services (Investing for the Kids)

If you are a parent looking to start a “Roth for Kids” or a custodial account:

- Fidelity Youth Account: Allows teens (13-17) to have their own app, debit card, and brokerage account with parental oversight. It is the best financial education tool on the market.

- Vanguard: Offers traditional UGMA/UTMA and 529 plans, but the interface is firmly designed for the parent, not the child.

Part 7: The “Fiscal Verdict” Matrix

| Factor | Vanguard Wins IF… | Fidelity Wins IF… |

|---|---|---|

| Philosophy | You want the “Church of Bogle” (Stay the Course). | You want the “Financial Hub” (Innovation). |

| Technology | You find 24/7 access to your balance distracting. | You want a high-speed, modern mobile app. |

| Trust Signal | Mutual ownership (The funds own the firm). | 150-year private family ownership legacy. |

| Small Balances | You have $3k+ (to meet Mutual Fund minimums). | You have $1.00 (Fractional shares + $0 min). |

The Daily Fiscal Verdict

Vanguard is the Institution. Fidelity is the Platform.

If you are a “Fiscal Traditionalist” who wants to know that your brokerage will never be sold to a public competitor, Vanguard’s mutual structure is the ultimate trust signal. It is the safest “forever” home for a multi-million dollar retirement nest egg.

However, if you are a “Modern Wealth Builder” under age 50 who values ease of use, fractional shares, spot crypto access, and the math of absolute zero fees, Fidelity is currently the superior technical choice for the 2026 small investor.

For accounts above $250k, or if you’re also considering Charles Schwab, see our three-way Vanguard vs Fidelity vs Schwab 2026 analysis — it covers the cash yield gap and tax-loss harvesting differences that become material at larger balances.

Your 7-Day Implementation Plan

- Day 1: The Core Choice. Decide: Do you want an “Everything App” (Fidelity) or a “Savings Vault” (Vanguard)?

- Day 2: The Account Opening. Both take ~5 mins. If you chose Fidelity, open a Roth IRA and a Cash Management Account.

- Day 3: The “Sweep” Audit. Link your bank via Plaid. Verify that your uninvested cash is earning at least 4.5%+ (Fidelity SPAXX or Vanguard VMFXX).

- Day 4: The Zero Fund Allocation. If in a Roth IRA, buy your first $10 of FZROX (Total Market). Witness the zero-fee beauty.

- Day 5: The Recurring Machine. Set up an “Automatic Investment” of $50/week. Wealth isn’t built on lump sums; it’s built on frequency. If you want a robo-advisor to handle allocation decisions automatically, our Betterment vs Wealthfront 2026 guide compares the two best automated options for accounts under $100k.

- Day 6: The Beneficiary check. This is the #1 mistake. Ensure your spouse or heirs are listed on the account immediately.

- Day 7: The “Habit” Shield. If you’re at Fidelity, turn on 2-Factor Authentication (2FA). If you’re at Vanguard, set a reminder to check the app only once every 3 months.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Investing

Investing Best Brokerages for Beginners 2026: Fidelity Wins

Ranked 7 brokerages for beginners on UI simplicity, $0 minimums, fractional shares, and first-year cost. Fidelity wins. M1 is best for passive investors.

Investing

Investing Why Financial Advisors Hate Vanguard (The Real Reason)

When an entire industry lobbies against a fund family, the reason is almost always about who profits. Here's the uncomfortable math behind the anti-Vanguard movement.

Investing Fidelity vs Schwab vs Vanguard for Retirement Accounts (2026)

Fidelity wins for most 401k rollovers and IRAs in 2026. Vanguard wins for large retirement accounts ($500k+). Schwab carries a $2,375/year cash drag. Our analysis of 1,242 accounts.