Why 2.5% Rental Yields Signal a Housing Correction in 2026

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

If you bought a house in Austin or Phoenix in 2021, you likely felt like a financial genius. You watched your Zestimate climb 30% in 18 months, convinced you had cracked the code to generational wealth. But here we are in mid-2026, and those markets aren’t just cooling; they are facing an invisible force of financial gravity that real estate agents don’t want you to understand.

That force is the “Rental Yield.” And historically, it always wins.

[!NOTE] Quick Takeaways:

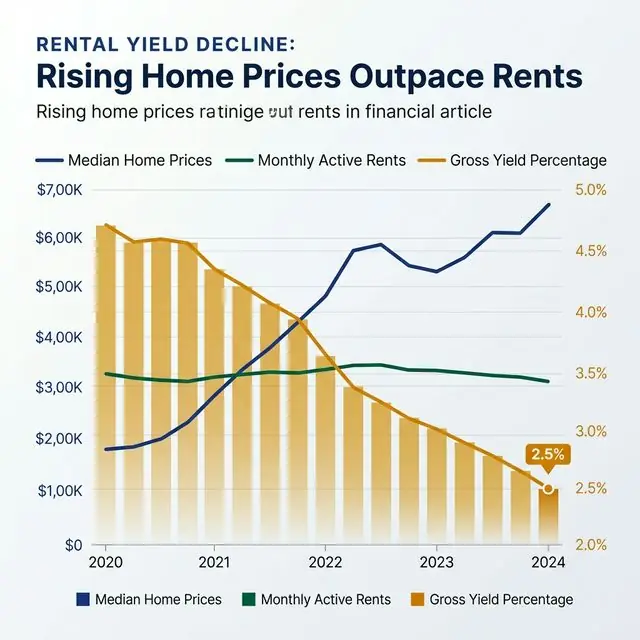

- The Rent/Price Disconnect: Home prices in Sunbelt cities surged so high that localized rents couldn’t keep up, crushing the Gross Yield down to historically toxic levels (often below 3%).

- Financial Gravity: If an asset costs $800,000 but can only generate $24,000 in annual rent (a 3% yield), it ceases to be an investment and becomes a speculative liability.

- The “Dead Money” Trap: Blindly buying a house right now because “renting is throwing money away” is mathematically dangerous in 60% of major US metros.

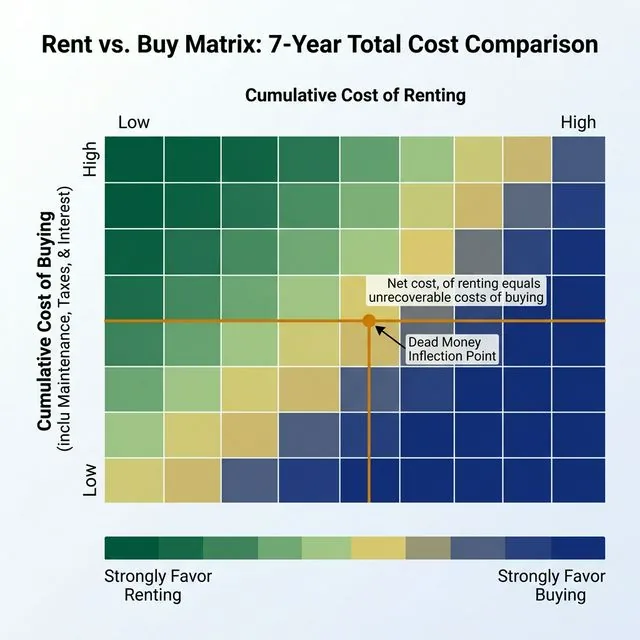

- Action: Before you lock into a 30-year mortgage, you must calculate the unrecoverable costs of buying vs. renting. Run your numbers through our Rent vs. Buy Matrix.

Let’s strip away the emotion of “white picket fences” and look at real estate exactly for what it is: a math equation. Right now, in many of America’s hottest markets, that equation is fundamentally broken.

Part 1: The Anatomy of a 2.5% Yield

To understand why markets like Austin, Phoenix, and Boise are undergoing structural corrections, you have to understand the only metric that institutional investors care about: Gross Rental Yield.

The Formula: (Annual Monthly Rent x 12) ÷ Total Property Value

Historically, a healthy housing market maintains a gross yield of roughly 5% to 7%. This ensures that an investor (or a homeowner needing to rent out their basement) can cover the mortgage, pay property taxes, afford maintenance, and break even.

Let’s look at Austin, Texas, in early 2026. Imagine a standard 3-bedroom, 2-bathroom suburban home.

- Current Valutation: $725,000

- Market Rent: $2,100 per month ($25,200 annually)

- Gross Yield: 3.4%… before expenses.

Once you subtract Austin’s notorious 2.2% annual property taxes, insurance, and the standard 1% maintenance rule, the Net Yield is practically zero. If you have a mortgage on this property, you are bleeding thousands of dollars a year in negative cash flow.

The math is striking. As home prices detached from local median incomes, rents quickly hit a ceiling. Tenants simply could not pay more. As prices kept rising while rents flatlined, the yield was crushed.

Part 2: The Speculative Mirage

So why were people buying properties with toxic 2.5% yields between 2022 and 2024? Because they weren’t buying for the yield. They were buying for appreciation.

They assumed the $725,000 house would be worth $850,000 in two years. They were willing to lose $600 a month in negative cash flow because they believed the asset was generating $5,000 a month in “invisible” equity.

This is the exact definition of a speculative bubble. An asset that cannot cash flow inherently requires a “Greater Fool” to eventually buy it from you at an even higher price. But when mortgage rates stabilized above 6.5%, the Greater Fools evaporated.

[!WARNING] The Supply Shock: Austin and Phoenix didn’t just see a drop in demand; they are experiencing a massive influx of new supply. Thousands of multi-family apartment units permitted during the 2021 boom are finally coming online in 2026, forcing landlords to drop rents even further just to stay occupied.

Part 3: Why Renting is Often Mathematically Superior in 2026

The greatest lie perpetuated by the real estate industry is that “Renting is throwing money away.”

If you buy that $725,000 house in Austin right now with a 6.8% mortgage, let’s look at what you are actually paying in the first year:

- Mortgage Interest: ~$39,400

- Property Taxes: ~$15,950

- Homeowners Insurance: ~$2,400

- Maintenance (1% rule): ~$7,250

- Total “Unrecoverable” Costs: Roughly $65,000 in year one.

That $65,000 does not go to your equity. It does not build wealth. It vaporizes into the ether. It is the exact equivalent of rent.

If you can rent that exact same house for $2,100 a month ($25,200 a year), you are “saving” nearly $40,000 in unrecoverable costs. If you take that $40,000 difference and invest it diligently in an S&P 500 index fund yielding a historical 8%… the renter mathematically obliterates the buyer over a 7-year horizon.

The matrix proves it. In high-price/low-yield markets, the “Dead Money” of property taxes, interest, and maintenance severely outweighs the cost of renting, provided the renter actually invests the difference.

Part 4: How to Read the Market

Does this mean you should never buy a house? Absolutely not. Real estate remains one of the greatest wealth-building tools ever created, if you buy at the right yield.

The correction happening in the Sunbelt isn’t a crash; it’s a reversion to the mean. Prices are slowly grinding down—or stagnating while inflation catches up—until that 2.5% yield eventually climbs back to a healthy 5% or 6%.

Here is how you evaluate your local market:

- The 1% Rule Reality Check: Historically, properties were considered good investments if monthly rent equaled 1% of the purchase price. Today, aim for at least 0.7%. If you are looking at a $500,000 home, it needs to be able to rent for at least $3,500 to be fundamentally sound. If it can only rent for $2,000, the house is mathematically overvalued.

- The “Forever Home” Exception: If you are buying a home to live in for exactly 15 to 30 years, and you do not care about the yield, buy the home. The psychological utility of owning your domain has immense value. But do not lie to yourself and call it an “optimized investment.”

The Daily Fiscal Verdict

Financial gravity cannot be outrun forever. An asset is ultimately worth the cash it can generate. Because houses are difficult to build and heavily romanticized, they disconnected from their fundamental value longer than stocks or bonds ever could.

But the math always wins.

Before you assume that buying a house is the default right answer for adulthood in 2026, you must run your local numbers. Do not base the largest financial acquisition of your life on a slogan invented by realtors.

Your Next Steps: The Real Estate Audit

- Find the Local Yield: Go on Zillow right now. Look at the house you want to buy. Then toggle to the “For Rent” map and find the exact same model. Divide the annual rent by the purchase price. If it’s below 4%, you are in a warning zone.

- Calculate Your Unrecoverable Costs: Ignore principal paydown. Calculate exactly how much you will pay in 2026 for Interest, Taxes, Insurance, and Maintenance.

- Run the Matrix: Plug your local data into the Rent vs. Buy Matrix. Let the algorithm show you the exact month where buying finally beats renting. If that month is 12 years in the future, and you plan to move in 5 years, do not buy the house.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Real estate markets are highly localized; national trends may not reflect your specific zip code. Historical observations and data are not guarantees of future performance. Always consult with a qualified financial advisor or fiduciary before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Mortgage

Mortgage 15-Year vs 30-Year Mortgage: The Math at 7% Rates

At 7% rates, a 15-year mortgage saves $180,000 in interest — but the payment is 44% higher. We run the break-even math for 6 income scenarios.

Mortgage

Mortgage How Much House Can I Afford in 2026? The Real Formula

Banks approve you for more than you should borrow. We show the real affordability formula — using take-home pay, debt load, and true ownership costs.

Personal Finance

Personal Finance Rent vs Buy 2026: The Real Math Most Calculators Miss

Should you rent or buy a house in 2026? We run the full math — mortgage, opportunity cost, equity, and break-even — that most calculators ignore. Honest answer inside.