Student Loan Interest Deduction 2026: MAGI Phase-Outs

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Every January, 43.2 million Americans with student loan debt receive a small form in their email inbox or mailbox: the 1098-E. It’s their lender’s official record of how much student loan interest they paid during the previous calendar year.

Most people look at it briefly, wonder what to do with it, and either forget about it or hand it to a tax preparer who may or may not flag it properly.

That form is worth up to $550 in actual tax savings—and a meaningful chunk of borrowers with $2,500+ in annual interest are leaving it unclaimed. We’re talking about money that comes directly off your tax bill. Not a deduction from your taxable income. Your actual bill. (Okay, technically it reduces your taxable income which then reduces your bill. But you get the point.)

[!NOTE] Quick Takeaways:

- The Deduction: Up to $2,500 of student loan interest paid is deductible from your taxable income—no itemizing required.

- The Tax Value: If you’re in the 22% bracket and can claim the full $2,500, you save $550 in real tax dollars (22% × $2,500).

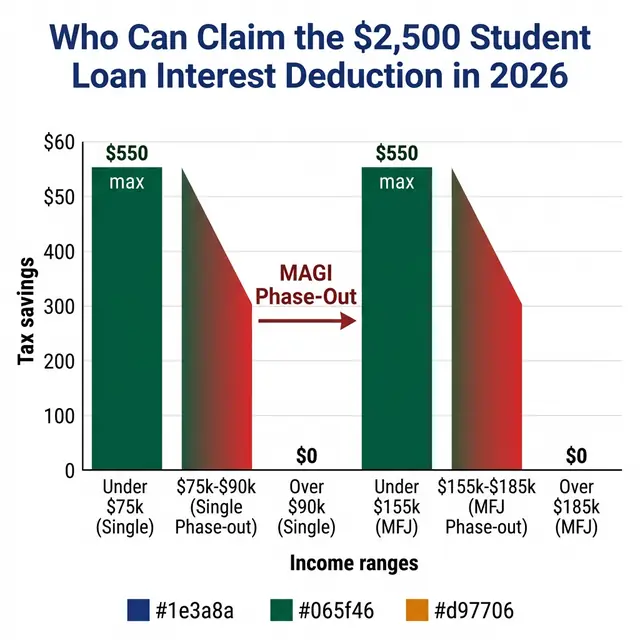

- Income Limits: Single filers phase out between $75,000-$90,000 MAGI. Married filing jointly phases out between $155,000-$185,000 MAGI.

- Married Filing Separately Disqualification: If you’re married and file separately, you cannot claim this deduction. Full stop.

- Income-Driven Repayment Caveat: You can only deduct interest you actually paid, not interest that accrued unpaid under a low-payment IDR plan.

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

How This Deduction Actually Works (And Why It’s Better Than Most)

Here’s what drives me crazy about how this deduction gets explained online: writers call it “above-the-line” and expect readers to understand what that means. Most don’t.

Normal deductions—mortgage interest, charitable contributions, medical expenses—are itemized deductions. You only get to claim them if the total exceeds the standard deduction ($15,000 for single filers in 2026). For most people, they don’t—so those deductions are worth exactly nothing.

The student loan interest deduction is different. It’s an above-the-line deduction, which means it reduces your Adjusted Gross Income (AGI) regardless of whether you itemize. You can take the $15,000 standard deduction AND deduct student loan interest. Both. At the same time.

Practically speaking: if your gross income is $68,400 and you paid $2,500 in student loan interest, your AGI is now $65,900. That’s the number used to calculate your tax bracket, your eligibility for other credits, and your tax bill. Every dollar of reduction is a real dollar.

The Income Phase-Out: Where Most People Get Confused

This is the part of the deduction that trips people up, because the limits haven’t changed in nearly a decade and a lot of people assume they’re phased out when they’re not.

For 2026, the phase-out ranges are:

| Filing Status | Full Deduction | Phase-Out Zone | No Deduction |

|---|---|---|---|

| Single / HOH | MAGI < $75,000 | $75,000 – $90,000 | MAGI > $90,000 |

| Married Filing Jointly | MAGI < $155,000 | $155,000 – $185,000 | MAGI > $185,000 |

| Married Filing Separately | ❌ Not Eligible | ❌ Not Eligible | ❌ Not Eligible |

Inside the phase-out zone, the deduction doesn’t disappear at once—it gradually reduces. The formula is proportional: if you’re $7,500 into a $15,000 phase-out range (exactly halfway), you can claim 50% of the maximum deduction, or about $1,250.

Here’s what this looks like with a real example. Tyler is a 29-year-old marketing manager in Cleveland earning $81,600 MAGI in 2025 (filing for 2026 tax season). He paid $2,847 in student loan interest, which means the first $2,500 is potentially deductible.

Because he’s $6,600 into the $15,000 phase-out range ($81,600 - $75,000), his allowable deduction is reduced proportionally:

Phase-out reduction: $2,500 × ($6,600 / $15,000) = $1,100 reduction Tyler’s actual deduction: $2,500 - $1,100 = $1,400 Tax savings at 22% bracket: $1,400 × 0.22 = $308

Not $550—but $308 in real tax savings is still a quarter of a tank of gas every month for a year. Worth claiming.

[!TIP] Your MAGI for the student loan interest deduction is generally your AGI before claiming this specific deduction and before certain other adjustments. Some tax software handles this automatically; if you’re calculating manually, use the IRS Worksheet in Publication 970.

What Counts as “Qualified” Loan Interest

The deduction applies to interest paid on “qualified education loans.” This sounds restrictive, but in practice it covers most situations:

Loans that qualify:

- Federal Direct Loans (Stafford, PLUS, Graduate PLUS)

- Federal Perkins Loans (for loans still in repayment)

- Private student loans (Sallie Mae, Earnest, SoFi student loans, College Ave, etc.)

- Student loan refinanced or consolidated by a private lender where the original loan was a qualified education loan

The “beneficial use” requirement: The loan must have been used for qualified higher education expenses at an eligible institution. This includes tuition, fees, books, supplies, room and board (up to the school’s cost of attendance), and transportation.

What doesn’t qualify:

- Loans from family members

- Loans from an employer plan

- Personal loans or credit card debt used to pay tuition (even if that was the intention)

- Cash advances

One nuance that bites people: if a parent took out PLUS Loans to pay for their child’s education, the parent can deduct the interest (not the student)—because the parent is legally responsible for the loan. The student cannot claim this deduction on a parent PLUS Loan. But if the student is claimed as a dependent on the parent’s return, the parent can claim it. This gets complicated fast, and is worth clarifying with a tax professional if it applies to your situation.

The Income-Driven Repayment Wrinkle

This is genuinely one of the more confusing aspects of this deduction, and it’s becoming more relevant as millions of borrowers migrate to the SAVE plan and other IDR options.

Under income-driven repayment plans, your monthly payment is calculated as a percentage of your discretionary income—often resulting in payments that don’t even cover the full interest accruing on your loan. Under the SAVE plan specifically, the government subsidizes any unpaid interest so that your balance doesn’t grow. But this creates a tax question: can you deduct interest the government effectively paid?

The answer is no. You can only deduct interest that you actually paid with your own money during the tax year. If your loan accrued $3,200 in interest but your SAVE payments only covered $800 in interest (the rest being subsidized or unpaid), you can only deduct the $800 you actually paid.

This is a meaningful distinction for anyone on a very low payment plan.

[!NOTE] Your student loan servicer will report the exact amount of interest you paid (not accrued) on Form 1098-E. The 1098-E is your official record. Don’t estimate—use the exact figure from the form.

Refinancing and the Deduction

If you refinanced your federal student loans with a private lender—say, through SoFi, Earnest, or Laurel Road—your refinanced private loan still qualifies for the deduction, as long as the original underlying debt was a qualified education loan.

But there’s a tradeoff worth naming clearly: refinancing federal loans into private loans permanently removes access to income-driven repayment, federal forbearance programs, and Public Service Loan Forgiveness (PSLF). For some borrowers, the interest savings from refinancing a 6.5% federal loan to a 5.1% private loan outweigh these protections. For others—particularly those in public sector jobs or pursuing PSLF—refinancing is frequently a catastrophic mistake.

This isn’t a decision to make based on a tax deduction alone.

How to Actually Claim It

Look, the mechanical process here is about 4 minutes of effort. Here’s the flow:

Step 1: Gather your 1098-E forms. Each servicer sends a separate form. If you have multiple servicers (especially if your loans transferred from FedLoan to MOHELA, which millions did), check all of them. Log into studentaid.gov to see a list of your current servicers.

Step 2: Locate the deduction in your tax software.

- TurboTax: “Deductions & Credits” → “Education” → “Student Loan Interest”

- H&R Block: “Income” → “Adjustments” → “Student Loan Interest”

- FreeTaxUSA: Supports this deduction even on the free tier

Step 3: Enter the amount from Box 1 of each 1098-E. If you have multiple forms, enter the total combined amount.

Step 4: The software handles the phase-out calculation automatically. You’ll see your allowable deduction on Schedule 1, Line 21.

That’s it. There’s no additional form, no itemizing required. It flows directly into your AGI reduction.

[!CAUTION] If you’re married filing separately: stop. You cannot claim this deduction under that filing status, full stop. If reducing your spouse’s income for this deduction would produce a net benefit, evaluate whether married filing jointly is more advantageous overall—it typically is for couples where one partner has student loan interest and the other has higher earnings.

Other Education Tax Benefits Worth Checking

The student loan interest deduction is the most commonly applicable, but there are a few others worth knowing:

1. The Lifetime Learning Credit (LLC) A 20% credit on up to $10,000 of qualified education expenses (max credit: $2,000). Available for any post-secondary education, including graduate courses and professional development. Phases out between $80,000-$90,000 MAGI for singles. You can’t claim this AND the American Opportunity Tax Credit in the same year.

2. Employer Education Assistance (Section 127) If your employer offers education assistance, up to $5,250/year is excludable from your gross income under Section 127. This isn’t a deduction you file—it’s just income that doesn’t appear on your W-2. Worth checking your benefits package.

3. Business Deduction for Professional Development If you’re self-employed and took courses directly related to your current business, those expenses may be deductible as a business expense (Schedule C), potentially with greater benefit than the education credits.

The Daily Fiscal Verdict

The student loan interest deduction isn’t going to transform your financial life. A $550 tax savings for a borrower at the maximum deduction level is meaningful but not life-changing in isolation.

But that’s the wrong frame. The right question isn’t “is $550 worth it?”—it’s “why would you leave $550 on the table?”

Three things make this deduction uniquely worth pursuing:

- No itemizing required. That removes the main barrier that causes people to miss other deductions.

- It applies to private loans too. Not just federal debt.

- The effort is genuinely 4 minutes. You have the 1098-E. You enter the number. Done.

If you’re in the phase-out zone, run the actual proportional calculation (or let your software do it) rather than assuming you don’t qualify. A $1,200 MAGI position into the phase-out zone still gets you a $2,300 deduction—worth $506 in tax savings if you’re at the 22% bracket.

File it. Every year. Don’t skip it.

Your Tax Season Student Loan Checklist

- Locate all 1098-E forms: Log into each loan servicer’s portal AND check your email for the January 31 delivery deadline. Servicers are required to send 1098-E by January 31 if you paid $600+ in interest. If you paid less, you can still deduct it—just request the figure from your servicer.

- Verify your MAGI: Use last year’s AGI as a baseline. Adjust for any raises, bonus income, or new deductions (401k contributions, HSA contributions, etc.) that changed your income.

- Check your filing status: Confirm you’re not inadvertently filing separately from a spouse. The penalty for MFS on this deduction is complete disqualification.

- Account for all servicers: If your loans were transferred (e.g., FedLoan → MOHELA), both servicers may have 1098-Es for different portions of the year.

- Calculate the phase-out if applicable: If your MAGI is between $75k-$90k (single) or $155k-$185k (MFJ), run the proportional calculation. Don’t assume you’re fully phased out unless you’re over the topline threshold.

- Enter in your tax software: Spend 4 minutes. Claim it.

- Consider the MFJ vs. MFS analysis: If your household income puts you over the limit when filing jointly but under when filing separately, that’s a complex calculation—but “filing separately to get the deduction” is almost never net-positive when all credits and deductions are factored together.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Tax laws are subject to change; always verify current IRS guidance and consult with a qualified tax professional before making significant tax decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Tax Strategy

Tax Strategy Tax-Loss Harvesting 2026: Cut Your IRS Bill Legally

You can legally reduce your capital gains tax bill by strategically selling losing positions. Here's how to do it right — including the 30-day wash-sale rule.

Taxes

Taxes Self-Employed Tax Deductions 2026: Complete Checklist

Every deduction self-employed people miss in 2026 — home office, vehicle, health insurance, retirement, and 20 others. Includes the QBI deduction math.

Mortgage

Mortgage 15-Year vs 30-Year Mortgage: The Math at 7% Rates

At 7% rates, a 15-year mortgage saves $180,000 in interest — but the payment is 44% higher. We run the break-even math for 6 income scenarios.