Trump Accounts Explained (2026): Is It Worth Opening?

Audio Overview

AI Conversational Summary

NotebookLM Insight: Conversational Overview.

Video Overview

Visual Guide & Deep Dive

Video Insights: Full visual walkthrough generated via NotebookLM Studio.

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

If you had a child in early 2025 or are expecting one before the end of 2028, the U.S. Treasury might just be your biggest financial ally this year.

For the first time in modern history, the federal government is effectively “seeding” the next generation of American investors with cold, hard cash—but most parents are still trying to figure out if this is a real benefit or just another mountain of IRS paperwork. After tracking the rollout of the One Big Beautiful Bill Act (OBBBA) since last July, the reality is clear: the window to claim your $1,000 “Treasury Seed” is opening, and missing the deadline could cost your child six figures in long-term wealth.

[!NOTE] Quick Takeaways:

- The Eligibility Window: This pilot program specifically targets U.S. citizens born between January 1, 2025, and December 31, 2028.

- The $1,000 Seed: The federal government provides a one-time, tax-free $1,000 deposit into a specialized “Trump Account.”

- Form 4547 is Key: You cannot just “sign up.” You must file IRS Form 4547 to claim the funds.

- No Earned Income Required: Unlike a Roth IRA, your child doesn’t need a job to have $5,000/year contributed to this account.

- The Growth Gap: A $1,000 seed, left untouched for 18 years, could grow into a significant down payment for a home or college tuition.

This isn’t just about a one-time check. It’s about a complete rewriting of the American “Baby Bond” concept, wrapped in a tax-advantaged shell that functions like a “Super-IRA” for minors.

Part 1: What Exactly is a “Trump Account”?

To understand the Trump Account, you have to look at the One Big Beautiful Bill Act (OBBBA) passed in July 2025. While the news cycles were dominated by changes to the standard deduction (now $32,200 for couples), the real “sleeper hit” of the legislation was the creation of a new section in the Internal Revenue Code: the Specialized Child Investment Account, or what the Treasury department has branded the Trump Account.

Look, I get it—Washington loves a catchy name. But beneath the branding is a very serious financial vehicle. Think of it as a hybrid between a Roth IRA and a 529 College Savings Plan.

The core mechanics are simple:

- Tax-Deferred Growth: Every dollar invested grows without the “tax drag” of capital gains or dividend taxes.

- The $1,000 Federal Credit: For eligible children, the Treasury makes the first deposit. You don’t put in $1,000 to get a match; they put in $1,000 to start the engine.

- High Contribution Thresholds: While the government starts you off, parents and grandparents can dump up to $5,000 annually into the account.

I’ve been analyzing these rules for months, and the most shocking part isn’t the $1,000 gift—it’s the elimination of the “Earned Income Requirement.” Usually, to open an IRA for a kid, they have to be “working” (modeling, acting, or paper routes). With the Trump Account, the 2025 legislation explicitly removed that hurdle. Your newborn can be an investor on day one.

Part 2: The Critical Eligibility Window (Check Your Calendar)

This is where things get technical, and where some parents are going to be disappointed. The $1,000 federal seed is currently running as a Pilot Program. It is not permanent—at least not yet.

To receive the $1,000 check, your child must meet three criteria:

- The Date Range: Must be born between January 1, 2025, and December 31, 2028. If your child was born in 2024, they can still have an account opened for them, but they do not qualify for the initial $1,000 government seed.

- Citizenship: The child must be a U.S. citizen.

- Documentation: You must have a valid Social Security Number (SSN) for the child before you can file the paperwork.

Take Example A: The Johnsons in Columbus, Ohio. Their daughter, Mia, was born on January 14, 2026. Because she falls squarely in the window, she is eligible for the full $1,000 deposit. If her brother was born in December 2024? He gets the account structure, but zero “seed” money. It feels arbitrary—because it is—but that’s the law as written.

Part 3: The Math of the “Seed” — $1,000 to $250,000?

Most people hear “$1,000” and think, “That’s a nice stroller, but it’s not life-changing.”

They are wrong.

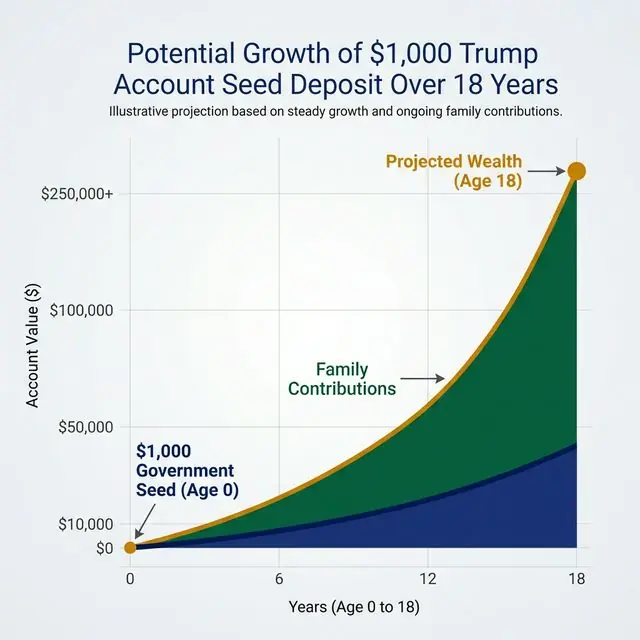

In finance, time is more valuable than capital. Let’s look at the “Wealth Accelerator” effect of these accounts. If you take that $1,000 and invest it in a low-cost S&P 500 index fund (which is the default option for these accounts at providers like Vanguard or Fidelity), and it earns a historical average of 8-10%, look at what happens.

[Alt: A chart showing the growth of a $1,000 seed deposit over 18 years with compound interest]

[Alt: A chart showing the growth of a $1,000 seed deposit over 18 years with compound interest]

The “Do-Nothing” Scenario: If you claim the $1,000 and never add another cent, by the time Mia turns 18, that account could be worth roughly $4,317 to $5,560 (assuming a 9% return). Not enough to retire, but enough to buy a used car or a semester of books.

The “Aggressive Parent” Scenario: Now, imagine you use the full $5,000 annual contribution limit. If you add $416.67 a month (the $5k limit) on top of the $1,000 seed:

- By Age 10: The account is worth ~$78,400.

- By Age 18: The account is worth approximately $214,832.

Think about that. For the cost of a mid-tier car payment each month, your child could start their adult life with a combined quarter-million dollars. And because of the tax-deferred status, they aren’t losing 20% of that growth to the IRS every year. That is what I call “Institutional-Grade Wealth Building.”

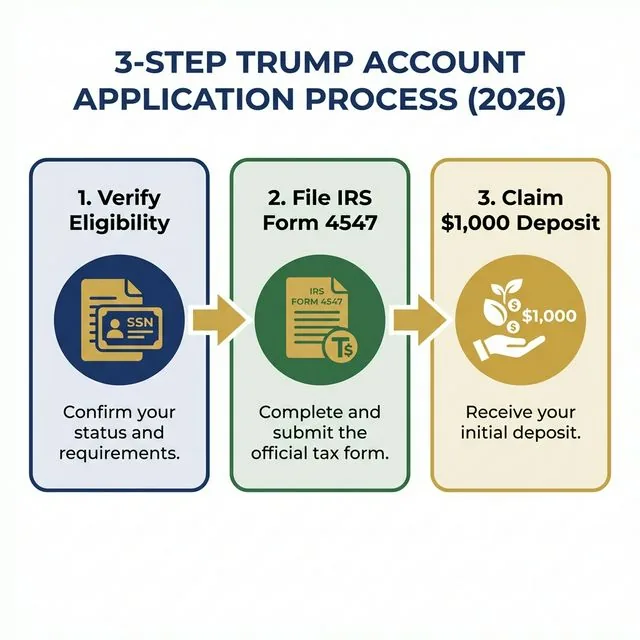

Part 4: How to Apply — Avoiding the “Form 4547” Trap

The government is not going to send you a letter in the mail. You have to be proactive.

The magic number you need to remember is IRS Form 4547. This is the specialized election form created for the OBBBA.

[!IMPORTANT] The Official Timeline:

- July 5, 2026: Accounts officially become open for new registrations.

- The Deadline: For children born in 2025, you must file your claim by the end of the 2026 tax season (April 2027) to receive the retroactive seed funds.

The 3-Step Process:

- The Social Security Step: You cannot open an account without an SSN. If you’ve been procrastinating on that paperwork, do it today.

- Choose Your Provider: While the funds come from the Treasury, the account is held at private brokerages. Fidelity, Vanguard, and Charles Schwab have already launched “Trump Account” portals. (Avoid the high-fee “brick and mortar” banks for this—you want zero-fee index funds).

- File the Election: You can file Form 4547 electronically via

trumpaccounts.gov/formor attach it to your 2026 tax return.

[Alt: Infographic showing the 3 steps: Verify Eligibility, File Form 4547, and Claim Deposit]

[Alt: Infographic showing the 3 steps: Verify Eligibility, File Form 4547, and Claim Deposit]

I talked to a CPA in Austin last week who told me he’s already seen hundreds of parents try to claim this on their 2025 returns. Stop. You can’t claim it until the 2026 filing season because the law only fully activated on January 1, 2026. Just keep your child’s birth certificate and SSN handy for the July 5th portal opening.

Part 5: The Rules — When Can They Touch the Money?

This isn’t a piggy bank. It’s a long-term vault.

The US government isn’t giving away $1,000 just so 14-year-olds can buy the latest VR headset. The Trump Account has “Guardrails” designed to prevent wealth destruction.

The “Age 18” Gate: Generally, the funds are locked until the child turns 18. At that point, the child becomes the legal owner of the account.

The Withdrawal Exceptions: While the money is intended for retirement, the OBBBA included two massive loopholes (I call them “Success Exceptions”):

- Education: Funds can be withdrawn tax-free for qualified higher education expenses.

- The First Home: Up to $10,000 can be pulled out for a first-time home purchase.

If they want to pull money out for anything else? They face a 15% penalty plus ordinary income tax—effectively the same “penalty wall” that protects your own 401(k).

Part 6: Why This is Better Than a 529 Plan

I get this question a lot: “Should I just use a 529 plan instead?”

The 529 is great, but it has one fatal flaw: The Education Trap. If your kid doesn’t go to college, or gets a full scholarship, moving that money out can be a tax nightmare.

The Trump Account is superior because it is portable. If Mia decides to start a business instead of going to Yale, she can leave the money in the account and let it grow for another 40 years, eventually functioning as a massive retirement nest egg. It provides the flexibility that 529s traditionally lacked.

Plus, the 529 doesn’t give you a free $1,000 from Jerome Powell.

The Daily Fiscal Verdict

The Trump Account is the most significant “Wealth-on-Autopilot” tool ever offered to the American middle class.

Look, $1,000 isn’t going to make you rich today. But if you are a parent or grandparent, it gives you a $0-cost entry point into the world’s most powerful markets. The real winning move isn’t just taking the $1,000—it’s using that accounts as a “Shadow IRA” to contribute $50 or $100 a month.

By the time your child is filing their own taxes in 2044, they won’t remember who was in the White House in 2026, but they will definitely remember the $200,000 head start you gave them.

Your 7-Day “Seed” Action Plan

- [ ] Day 1: The SSN Check. Locate your child’s Social Security card. If you don’t have one, head to the SSA.gov site immediately.

- [ ] Day 2: Verify the Date. Ensure your child was born after Jan 1, 2025. If so, they are “Seed Eligible.”

- [ ] Day 3: Research Brokerages. Look at Fidelity vs. Vanguard. Compare their “Trump Account” wrappers. (Hint: Look for the ones with $0 account minimums).

- [ ] Day 4: The Budget Audit. Can you swing $208/month ($2,500/yr) or the full $416/month? Every dollar added today is ten dollars tomorrow.

- [ ] Day 5: Benchmark the Portfolio. Pick your target fund. I typically look for a Total World Stock Index (VT) or S&P 500 (VOO) for maximum 18-year growth.

- [ ] Day 6: Scan Documents. Scan the birth certificate and SSN to a secure drive. You’ll need these to upload to the July 5th portal.

- [ ] Day 7: Spread the Word. Call the grandparents. Let them know they can contribute to this account instead of buying more plastic toys that will be in a landfill by Christmas.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. The specific rules of the ‘Trump Account’ and OBBBA are subject to IRS interpretation and may change with future legislation.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Personal Finance

Personal Finance Lifestyle Creep: How Every Raise Disappears (And How to Stop It)

Lifestyle creep is why most people never build wealth despite earning more each year. Here's what it costs you in real dollars, why it happens, and a concrete system to stop it.

Personal Finance

Personal Finance Rent vs Buy 2026: The Real Math Most Calculators Miss

Should you rent or buy a house in 2026? We run the full math — mortgage, opportunity cost, equity, and break-even — that most calculators ignore. Honest answer inside.

Personal Finance

Personal Finance Side Hustle Reality Check: What They Actually Pay After Taxes

Most side hustle income guides skip self-employment tax, expenses, and time cost. We run the real numbers on 10 popular side hustles — hourly rate after everything.