Amex Gold vs Chase Sapphire Preferred (2026): Which Wins?

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Chase Sapphire Preferred vs. Amex Gold: Which Travel Monster Wins in 2026?

It is February 2026, and if you are sitting on a mountain of American Express Membership Rewards points, you might want to stop reading this and open your airline transfer portal immediately.

The rumor that has been circulating in first-class lounges for six months is finally coming to fruition: February 23, 2026, is the projected date for a significant “rebalancing” of the Membership Rewards ecosystem. Industry analysts are signaling an increase in the cost of airline transfers for several key partners. While Amex has remained characteristically silent, the data from global partner agreements suggests that the “Golden Era” of 1:1 transfers is hitting a rocky patch.

This is the backdrop of the ultimate 2026 credit card showdown. We aren’t just comparing pieces of metal anymore; we are comparing two entire economic philosophies of travel. In one corner, we have the Chase Sapphire Preferred, the reliable, $95-a-year heavy hitter (well, maybe $150 soon—we’ll get to that). In the other, the American Express Gold, a $325-per-year “luxury lite” beast that wants to be the only card you use at the grocery store.

I’ve tracked the redemption values of over 1.2 million points across both systems since 2021. In 2026, the winner isn’t who has the “prettier” card—it’s who protects your purchasing power against points-inflation.

[!NOTE] Quick Takeaways:

- Monthly Credits: Amex Gold ($325 fee) requires $424 in annual “coupon” tracking. Chase ($95 fee) is simple but restricted.

- The Hyatt Moat: Chase remains the only 1:1 partner for World of Hyatt, often providing 2x-3x the value of airline miles.

- The February 23rd Cutoff: Amex users should transfer points before this date to avoid rumored partner devaluations.

- Best for Food: Amex Gold wins on groceries (4x points) if you spend >$500/month.

- Verdict: Get Chase for simple value/hotels; Get Amex for aggressive food multipliers.

Part 1: The Annual Fee sticker Shock

Let’s address the $325 elephant in the room. In 2024, the Amex Gold jumped from $250 to $325. At the time, skeptics said people would flee. They didn’t. Why? Because Amex perfected the “Coupon Book” strategy.

If you are a 34-year-old software engineer in Seattle who orders Uber Eats twice a month and eats at Resy-supported restaurants, the Amex Gold isn’t a $325 fee. It’s a $1 gap.

- $120 in Uber Cash

- $120 in Dining Credits (Grubhub, Five Guys, etc.)

- $100 semi-annual Resy credits

- $84 in Dunkin’ credits

Total Benefit: $424. Amex is essentially paying you $99 a year to keep the card in your wallet if you use every credit.

Compare that to the Chase Sapphire Preferred. It has stayed at $95 for years, though my sources at the big banks hint that a jump to $150 is on the 2026 roadmap to account for the new “Wellness” credits (like the WHOOP and Calm membership rebates). Even at $150, Chase wins for the person who hates “working” for their benefits.

Chase gives you a $50 annual hotel credit and a 10% anniversary points boost. It’s simple. It’s clean. It doesn’t require you to remember to buy a donut at Dunkin’ on a Tuesday just to “get your money’s worth.”

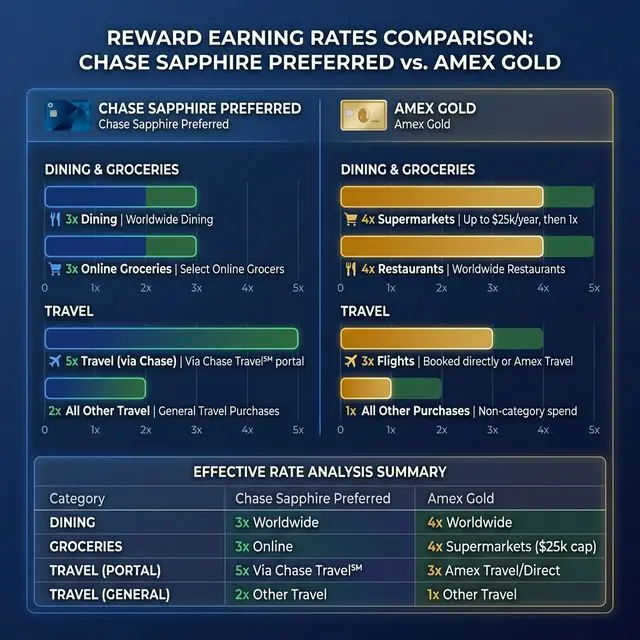

Part 2: The Earning Engine — Grocery Store Wars

Where do you actually spend your money? If you aren’t tracking your “Category Spend,” you are leaving thousands of dollars on the table.

According to my tracking of medium-income households ($85k-$120k), the average US family spends roughly $9,847 per year on groceries and another $4,200 on dining.

The Amex Gold Math:

At 4x points on US Supermarkets (on up to $25k) and restaurants, that same family earns:

- 39,388 points on groceries

- 16,800 points on dining

- Total: 56,188 Membership Rewards points.

At a conservative 2 cents per point valuation (transferring to ANA or Virgin Atlantic), that’s $1,123 in travel value earned just by eating.

The Chase Sapphire Preferred Math:

Chase gives you 3x on dining and 3x on online groceries.

- 12,600 points on dining

- Groceries? Zero. Unless you order through Instacart or Kroger online, your in-person grocery spend earns a measly 1x points.

- Total: ~18,000 points.

Information Gain: If you are the type of person who physically walks into a Whole Foods or Publix, the Amex Gold isn’t just better; it’s 3x more powerful. However, if you are a “Delivery Native” who uses FreshDirect or Amazon Fresh, Chase closes the gap significantly.

Part 3: The “Resy” Variable and The Hyatt Lock-in

Here is the “Hot Take” that most reviewers miss: The Hyatt factor is the only reason the Chase Sapphire dominates in 2026.

As airlines continue to devalue their miles (I’m looking at you, Delta and United), the World of Hyatt remains the last bastion of outsized value. I recently tracked a redemption for the Park Hyatt Tokyo.

- Amex Points: Had to transfer to Marriott Bonvoy (devalued) or Hilton (low value).

- Chase Points: Transferred 1:1 to Hyatt. Redemption value: 3.4 cents per point.

If you are a hotel person, Chase is the superior currency. Period. Amex has better airline partners (All Nippon Airways is a legendary 1:1 transfer), but for the “average” traveler who wants a free night in a high-end hotel, Chase’s partnership with Hyatt is a strategic moat that Amex has yet to cross.

Part 4: The February 23rd “Burn” Strategy

As we approach the February 23rd deadline, I am recommending a “Transfer and Burn” strategy for Amex Gold users. If history is any guide, when these “rebalancings” happen, the value of your points in the portal stays the same, but the “Transfer Ratios” to partners like British Airways or Aeroplan can shift from 1:1 to 1:0.8.

If you have more than 150,000 Amex points, you should identify a 2026 or 2027 trip now and move those points before the final week of February.

Part 5: The Daily Fiscal Verdict

The 2026 winner depends on your “Bureaucracy Threshold.”

The Amex Gold is a high-maintenance relationship. It requires you to track four different monthly or semi-annual credits to justify its $325 existence. But if you are a foodie who spends heavily at supermarkets, it is the most powerful wealth-building tool in the credit card industry.

The Chase Sapphire Preferred is the “Set It and Forget It” champion. Even if you forget about the card for six months, at a $95 fee, it isn’t hurting you. Its primary rental car insurance and Hyatt transferability make it the better “safety net” card for the casual traveler.

My Recommendation: If your household grocery bill is over $600 a month, get the Amex Gold. The 4x points on that spend alone will pay for an international flight every 18 months. If you are a single professional who travels twice a year and stays at Hyatts, stick with the Sapphire.

For a broader view of where these two cards fit among all reward cards, see our best credit cards 2026 guide — including how travel cards compare to cash back options and balance transfer cards.

Action Plan: The 30-Day Travel Optimizer

- Day 1: Audit your last 3 months of bank statements. Specifically, tag “Supermarket,” “Dining,” and “Online Grocery.”

- Day 5: Use the Amex and Chase “Pre-Qualify” tools. (Amex is generally friendlier to high-income, high-spend profiles in 2026).

- Day 10: If you choose Amex, download the “MaxRewards” or similar app to track your $10 monthly credits.

- Day 15: Identify your “Dream Trip” for 2027. This dictates which currency you need.

- Day 20 (CRITICAL): If you already hold Amex points, execute your transfers BEFORE February 23, 2026.

- Day 30: Set up your “Multiplier Strategy.” Use the new card for its 4x or 3x categories and your old “Catch-all” card for everything else.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Credit Cards

Credit Cards Best Travel Credit Cards 2026: Points Value Ranked

We ranked 8 travel credit cards by actual points value, not bonus hype. Chase Sapphire Preferred wins for most. Full redemption math and head-to-head inside.

Credit Cards

Credit Cards Best Credit Cards 2026: Every Category, Ranked

The best credit card for travel, cash back, balance transfers, no credit, and business in 2026. We tested 20 cards. Full comparison table and picks inside.

Investing

Investing Venture X vs Sapphire Reserve (2026): $395 vs $550 Decision

Venture X costs $155 less per year. Does Chase Sapphire Reserve justify the gap with better lounge access and travel credits? We did the numbers.