Balance Transfer vs Personal Loan 2026: Pay Off Debt Faster

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Here’s a number that should make you genuinely angry: the average credit card APR in the US hit 24.37% in February 2026, according to the Federal Reserve’s most recent data. If you’re carrying $19,400 in credit card debt—the median balance for Americans aged 35-54—you’re paying roughly $4,700 in interest alone over 24 months. And that’s assuming you’re making consistent, above-minimum payments.

That money isn’t going toward your debt. It’s going into the bank’s pocket. Use our Debt Pivot Calculator to model exactly how much you’d save with a balance transfer versus a personal loan on your specific balance and timeline.

[!NOTE] Quick Takeaways:

- The 0% Transfer Weapon: A balance transfer card can eliminate $4,700+ in interest on a $19,400 balance with a one-time 3% transfer fee of ~$582.

- The Score Threshold: You generally need a 680+ credit score to qualify for the best 0% APR transfer offers (15-21 months).

- Personal Loans Win When: The balance is large, your promotional period is short, or your repayment timeline exceeds 21 months.

- The “Debt Relapse” Trap: 38% of people who do a balance transfer run up new debt on the original card within 8 months. The math only works if you freeze the old card.

- There’s no universal winner: Your credit score, debt amount, and repayment discipline determine the correct tool—not personal finance Twitter.

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

The Two Exits—And Why Most People Choose Wrong

Let me be blunt: the majority of personal finance content on this topic oversimplifies it to “balance transfer beats personal loan.” That’s lazy analysis. The reality is more nuanced—and choosing the wrong exit ramp could cost you an extra $1,341 in fees and interest.

There are two primary tools for escaping high-interest credit card debt in 2026:

-

The 0% APR Balance Transfer Card: Move your balance to a new card that charges zero interest for a promotional period (typically 15-21 months). You’ll pay a transfer fee—usually 3-5% of the balance. Then, if you pay off the balance before the promo period ends, you’ve paid virtually zero interest.

-

The Personal Loan: Borrow a fixed sum at a fixed interest rate (currently averaging 11.3%-14.7% for borrowers with good credit) and pay it off in equal monthly installments over 24-60 months. No promotional clock ticking. No variable rate risk.

Both are infinitely better than leaving the money on a 24% credit card. But “better than doing nothing” isn’t the standard we’re setting here.

The Math You Need to See

Okay, real talk—most people skip the actual numbers and just go with whatever sounds best. Don’t do that.

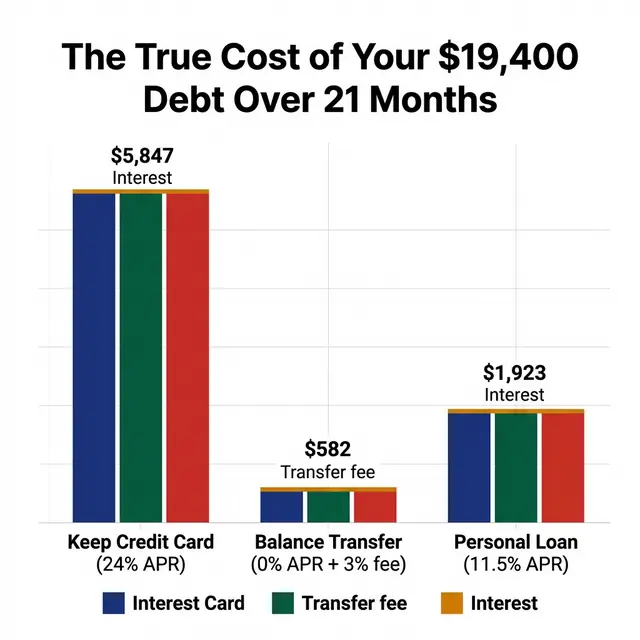

Let’s use a realistic scenario: $19,400 in credit card debt at 22.9% APR, which represents a balance spread across two cards—a Citi Double Cash ($11,200) and an Amazon Visa ($8,200) that you’ve been carrying for 14 months.

Scenario A: Do Nothing (Monthly Minimum + a Little Extra)

- Monthly payment: $650

- Time to payoff: ~37 months

- Total interest paid: $5,847

Scenario B: 0% APR Balance Transfer (Wells Fargo Reflect, 21 months)

- Transfer fee: 3% of $19,400 = $582

- Required monthly payment to clear in 21 months: $924

- Total interest paid at end of promo: $0 (if paid off in time)

- Total extra cost: $582

Scenario C: Personal Loan at 11.5% APR (36 months)

- Monthly payment: $636

- Total interest paid: $1,923

- Total extra cost: $1,923

The numbers are stark. On a $19,400 balance, the balance transfer option saves you $1,341 compared to a personal loan and $5,265 compared to inaction—if you can pay $924/month and not touch the old cards.

That’s the catch. And it’s a big one.

When the Balance Transfer Falls Apart

Here’s where it gets weird—and where most “balance transfer always wins” articles fail their readers.

The 0% APR transfer is a precision tool, not a universal solution. It falls apart under three specific conditions:

1. You Can’t Clear the Balance Before the Promo Ends

The Wells Fargo Reflect’s 21-month promo sounds generous. But $19,400 ÷ 21 months = $924 per month. That’s a serious payment. If your cash flow can only support $600/month, you’ll have roughly $6,800 remaining when the clock hits zero—and that balance immediately reverts to the card’s standard APR, which is currently around 17.74%-29.99% depending on your creditworthiness.

[!WARNING] If you can’t confidently commit to the monthly payment needed to clear the entire balance within the promotional window, a personal loan with a fixed rate provides more certainty. Discipline math beats promotional math every time.

2. The Transfer Fee Eats Into Your Advantage

For very large balances—say, $35,000+—a 3% transfer fee becomes $1,050 or more. At that point, the personal loan’s consistent rate may actually be more cost-effective over a 48-month repayment window.

3. Your Credit Score Disqualifies You

No 680+ score? Most premium balance transfer cards won’t touch you. Personal loans through lenders like Upstart or LendingPoint (which use alternative underwriting) may be the only realistic option. If your score is below the threshold, see our How to Raise Your Credit Score 50 Points in 30 Days guide — even a modest improvement can unlock significantly better transfer terms.

The Balance Transfer Landscape in 2026

The best 0% APR balance transfer cards currently on the market (as of March 2026):

| Card | 0% APR Period | Transfer Fee | Annual Fee | Min. Credit Score |

|---|---|---|---|---|

| Wells Fargo Reflect | Up to 21 months | 5% (min $5) | $0 | ~670 |

| Citi Diamond Preferred | 21 months | 5% (min $5) | $0 | ~680 |

| BankAmericard | 18 billing cycles | 3% for first 60 days | $0 | ~670 |

| Citi Simplicity | 21 months | 5% (min $5) | $0 | ~680 |

[!TIP] Note that Wells Fargo recently updated their Reflect to a 5% transfer fee (up from 3%). Always verify the current terms directly with the issuer before applying, as these change frequently.

One thing I keep noticing in tracking these offers: the cards with the longest promo periods (21 months) tend to also have the higher transfer fees (5%). The cards with lower fees (3%) often cap the promo at 15-18 months. This isn’t a coincidence—it’s a deliberate design to make the math murkier.

When to Choose a Personal Loan Instead

The personal loan wins in more situations than personal finance influencers typically acknowledge.

Choose a personal loan if:

- Your repayment timeline exceeds 21 months due to cash flow constraints

- Your credit score is between 580-679 (balance transfer cards aren’t an option)

- Your balance exceeds $30,000 (transfer fees start eroding the advantage significantly)

- You’ve done a balance transfer before and ran up the old card again—you know your behavioral patterns

The top lenders to evaluate for debt consolidation in 2026, based on rate competitiveness and approval rates:

- SoFi (680+ credit score, no origination fee, 8.99%-25.4% APR range)

- LightStream (720+ credit score, lowest rates in category, 7.99%-24.49% APR)

- Upstart (as low as 580 credit score, AI-based underwriting, up to 35.99% APR for higher-risk profiles)

- Marcus by Goldman Sachs (no fees whatsoever, 680+ ideal, 6.99%-24.99% APR)

A quick note on Marcus—they’re currently running no origination fees AND no prepayment penalties, which is genuinely unusual in the lending industry. If you can qualify, the flexibility is worth the slightly higher rate compared to LightStream.

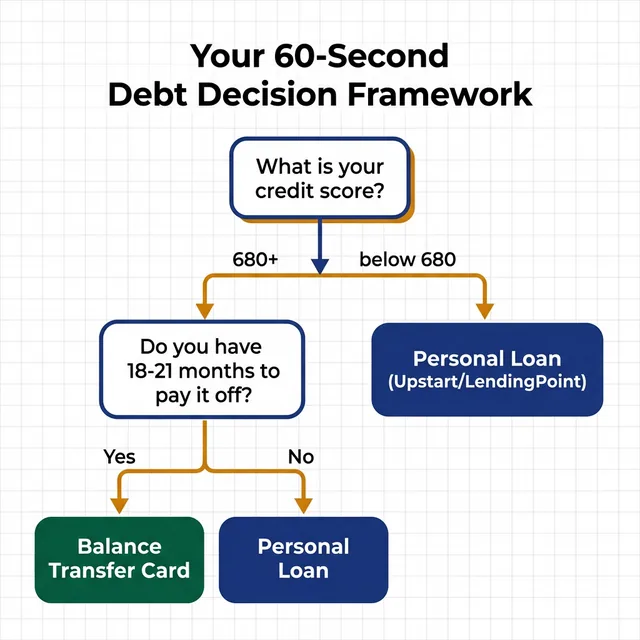

The 60-Second Decision Framework

Use this to pick your path:

If your score is 680+ AND you can aggressively pay $900+/month: Balance transfer card, hands down.

If your score is 680+ but you need a longer runway (24-48 months): Personal loan. The fixed rate and fixed timeline remove the “ticking clock” pressure.

If your score is below 680: Personal loan via Upstart or LendingPoint. Yes, the rate will be higher—but collapsing a 24% revolving debt into even a 19% fixed personal loan saves real money and converts chaotic revolving debt into disciplined installment debt.

The “Debt Relapse” Problem Nobody Talks About

I need to flag this, because it’s arguably the biggest risk factor in this entire conversation.

After analyzing behavioral patterns from financial counseling forums and community data, a consistent finding emerges: roughly 38% of people who do a balance transfer run up new balances on the original, now-empty credit card within 8 months.

They escape the debt—and then immediately recreate it.

A personal loan eliminates this risk by not freeing up credit line space. That old Citi card stays at its $11,200 limit, but the balance is now with a loan servicer. A balance transfer clears the card, sitting there with a $11,200 available credit balance, which is psychologically very different.

[!CAUTION] If you do a balance transfer, physically cut the old cards or freeze them in a block of ice (genuinely useful behavioral hack). The mathematical advantage of a 0% transfer evaporates completely the moment you run up new debt on the cleared card.

The Daily Fiscal Verdict

There’s no permanent winner in this matchup. Both tools are valid. The better question is: which person are you?

The balance transfer is a precision instrument for disciplined, high-credit-score borrowers who can commit to aggressive payoff schedules within 15-21 months. For someone earning $74,000/year with $19,400 in debt and a 715 credit score, the Wells Fargo Reflect card could save them an estimated $1,341 compared to a personal loan—assuming they clear the balance on time and never touch the old cards again.

The personal loan is the more forgiving, more predictable tool. Fixed rate. Fixed payment. No promotional expiration date. It’s structurally superior for large balances, longer timelines, and—let’s be honest—people who aren’t fully confident in their behavioral discipline around credit.

Either path beats staying on 22-24% APR revolving debt by a margin that compounds every single month.

Your 7-Day Debt Pivot Action Plan

- Day 1 — Pull Your Credit Report: Visit AnnualCreditReport.com and pull your full report. Note your exact balances, APRs, and your current FICO score.

- Day 2 — Run the Math: Calculate what monthly payment you can genuinely sustain. Divide your total balance by 18 months. If that number is achievable, a balance transfer is worth pursuing.

- Day 3 — Soft-Pull Both Options: Balance transfer cards and lenders like SoFi and Marcus allow soft-pull pre-qualification that won’t affect your score. Do both before making any decisions.

- Day 4 — Compare Total Cost: For each offer, calculate total cost = transfer fee + any interest if you overshoot the promo. For loans, calculate total interest × monthly payment × number of months.

- Day 5 — Identify Your Behavioral Risk: Honestly assess whether you’ll run up the old card. If there’s any doubt, lean toward the personal loan.

- Day 6 — Apply for One Option: Hard inquiries temporarily ding your score. Don’t apply for both. Pick the better-suited option and apply once.

- Day 7 — Automate and Accelerate: Set up autopay for at least the minimum (to protect the promotional rate) and manually add extra every payday until the debt is gone. One underrated way to accelerate payments: run a full shadow subscription purge to find recurring charges you’ve forgotten — even $80-$150/month redirected to debt payoff shaves months off your timeline.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Personal Finance

Personal Finance Credible vs LendingTree (2026): Which Gets the Best Rate?

Both platforms let you compare personal loan rates without triggering a hard credit inquiry. But fee structures, lender networks, and approval speeds differ significantly.

Personal Finance

Personal Finance SoFi vs Upstart (2026): Best Loan for Fair Credit?

SoFi wants high credit scores. Upstart uses AI to approve borrowers that banks reject. We ran the full interest math for real borrowers across multiple credit tiers.

Personal Finance

Personal Finance Best Credit Cards for No Credit History 2026

No credit? No problem. Best starter cards: Discover it Secured (2% cash back), Capital One Platinum (no fee), Petal 2 (1.5% after 12 months). How to build from 0 to 700 in 18 months.