The HELOC Trap: Why 'Free Money' Can Destroy Home Equity

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: March 24, 2026

[!IMPORTANT] Verified Data Source: Home equity rate benchmarks and regulatory lending data are sourced from the Federal Reserve Board (H.15) and CFPB Consumer Home Lending reports. Last verified: March 2026.

Let me paint a scenario that played out a few thousand times in 2023-2024, and is setting up to replay in the next 18 months.

A homeowner in suburban Atlanta has $140,000 in equity. Their home, purchased in 2019 for $310,000, is now appraised at $467,000. Their remaining mortgage balance is $327,000. In 2022, their bank offers them a HELOC up to $112,000 at “prime minus 0.25%” — which at the time meant about 2.75%. They take $60,000. They renovate the kitchen, consolidate some credit card debt, and buy an investment piece of furniture from an auction house (I’m not making this up).

By Q3 2023, prime rate sat at 8.5%. Their HELOC rate had climbed to 8.25%. What was a $275/month payment became $1,034/month. Their home, meanwhile, had plateaued in value—the Atlanta market softened after 2022’s spike.

[!NOTE] Quick Takeaways:

- HELOCs are variable-rate debt. In 2026, that variable rate remains elevated—most are priced at prime + margin (currently 7.5-9.5% for typical profiles).

- Your home is collateral. Missing HELOC payments can trigger foreclosure proceedings.

- The “draw period” illusion: paying interest-only feels manageable until the repayment period begins and payments can double or triple.

- Better alternatives exist: for home improvements specifically, HELOANs (fixed-rate home equity loans) or FHA Title I loans often make more sense.

- The 2026 risk scenario is specific: home values in many markets are flat-to-declining; tapping equity now locks you into high-rate debt against potentially shrinking collateral.

Why Banks Love Selling HELOCs Right Now

Before analyzing the risks, it’s worth acknowledging why your bank is marketing HELOCs aggressively in 2026. Banks are sitting on large portfolios of low-rate mortgages from 2020-2021 (many at 2.5-3%). They cannot profitably refi those customers at today’s rates, and those customers have no incentive to move.

But HELOC originations? Those are new, high-margin business. At 8-9% on a variable-rate product priced to the prime rate, HELOC interest income is substantially more profitable per dollar than the mortgages in their existing portfolio.

When your relationship banker calls to tell you that “you’re sitting on untapped equity,” understand the incentive structure behind that call. They’re not wrong—you may have significant equity. But the product they’re selling you benefits them at current rate levels.

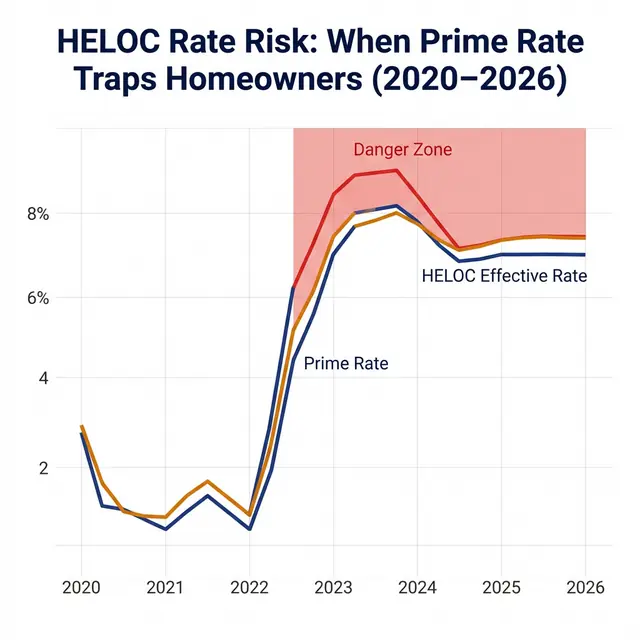

The Rate Chart That Should Give You Pause

That chart tells a specific story that most HELOC marketing literature doesn’t include. From 2020 to early 2022, prime rate sat near historic lows—3.25%. Borrowers who opened HELOCs in this window locked into what felt like nearly free money.

Then the Fed raised rates 11 times in 18 months. Prime climbed to 8.5%. By December 2023, a borrower who had opened a $50,000 HELOC at 2.75% in 2021 was now paying 8.25% on their outstanding balance—an interest cost increase of nearly $2,750 per year on that single line of credit.

As of March 2026, prime has moderated to approximately 7.5% following two Fed cuts. HELOC effective rates for typical borrowers sit around 7.25–8.9%, depending on creditworthiness and margin. That is not “nearly free money.” That is expensive, variable-rate debt secured by your most important asset.

[!WARNING] Many homeowners who opened HELOCs during 2020-2022 are still in their draw period and only paying interest. These borrowers are heading toward the repayment period (typically 10 years after opening) where they must repay both principal and interest simultaneously. Monthly payments can increase by 100-200%+ when the repayment period begins. If you’re in this situation, calculating your “repayment cliff” date is urgent.

The Three HELOC Traps That Catch People Off-Guard

Trap #1: The Interest-Only Draw Period Illusion

During the draw period (typically 10 years), most HELOCs allow interest-only payments. On a $60,000 HELOC at 8.5%, your monthly interest payment is approximately $425/month. That feels manageable.

But here’s what’s hiding at year 10: the repayment period begins, and now you’re paying principal plus interest over 20 years. That same $60,000 balance at 8.5% (assuming rates hold in this illustrative scenario) could become approximately $522/month—and if rates were to rise to 10%, the estimated payment climbs to around $580/month. These are hypothetical illustrations; actual payments depend on your specific loan terms and prevailing rates at each point. The transition is often abrupt with little gradual adjustment.

Trap #2: The Declining Collateral Risk

HELOCs are specifically dangerous in markets where home values are declining or flattening, and 2026 presents exactly this scenario in many metros. The National Association of Realtors has reported year-over-year appreciation of less than 2% in markets like Austin (+0.3%), Phoenix (-1.1%), and Nashville (+1.7%) as of late 2025. These markets saw 30-40% gains from 2020-2022 and are now in a correction.

If you borrowed $80,000 against what was $150,000 in equity, and your home’s value drops 8%, your equity shrinks to approximately $78,000. You’re now “equity-poor” on a line of credit that demands repayment. And unlike with unsecured debt, the bank can pursue your home.

Trap #3: The Psychological “Spending Account” Loop

This is the one the financial industry never talks about because it’s behavioral, not mathematical. A HELOC acts psychologically like a savings account that you’re drawing from—it feels like your money, because it’s secured by your asset. Research from the Federal Reserve Bank of Cleveland (2021) found that HELOC borrowers consistently overestimate their repayment discipline and underestimate lifetime interest costs.

In the Atlanta case I opened with, the homeowner told me: “It felt like I was just using money that was already mine.” That reframing—equity as personal savings rather than leveraged debt—is exactly how homeowners find themselves “house rich and cash poor” while paying 8.5% on a kitchen they might not be in long enough to recoup.

When a HELOC Actually Makes Sense in 2026

Look, I’m not arguing that HELOCs are categorically bad products. They’re bad products used for the wrong purposes. There are legitimate use cases:

Situation 1: Specific, Appendable Home Improvements Adding a bedroom, replacing a roof that’s functionally failing, or upgrading HVAC in a home you plan to stay in for 10+ years can make HELOC financing rational—if the improvement demonstrably adds more value than it costs. Get an independent appraisal. Don’t rely on contractor estimates or Zillow.

Situation 2: Short-Term Bridge Financing If you have a large, expected, near-term cash inflow (stock vesting, inheritance, business sale) and need liquidity right now for a specific purpose (say, a real estate closing gap), a HELOC can serve as a short-term bridge with lower rates than alternatives. The key word is short-term. Defined. Time-bounded.

Situation 3: True Emergency Reserve Some financial planners advocate opening a HELOC but never drawing on it—keeping it as a “backstop” emergency fund in case of catastrophic income loss. This is a legitimate strategy, with caveats: HELOCs can be frozen or reduced by the bank if your home’s value drops or your creditworthiness changes.

[!IMPORTANT] What HELOCs should NOT fund in 2026:

- Consumer spending, vacations, or lifestyle inflation

- Volatile asset purchases (crypto, individual stocks, speculative real estate)

- Consolidating unsecured credit card debt (you’re converting unsecured risk to secured risk against your home)

- Starting a business without substantial safety margins

Better Alternatives: What to Consider Instead

Before accepting a HELOC offer, run the comparison against these alternatives:

| Option | Typical Rate (2026) | Your Home At Risk? | Best For |

|---|---|---|---|

| HELOC | 7.25–9.5% variable | ✅ Yes | Short-term, home improvements |

| HELOAN (Fixed) | 7.5–9.0% fixed | ✅ Yes | Larger, one-time home improvements |

| Cash-Out Refi | 6.5–7.5% fixed | ✅ Yes | Large lump sums, want to simplify |

| Personal Loan | 7.0–25.0% | ❌ No | Smaller amounts, faster funding |

| 0% APR Credit Card | 0% (intro period) | ❌ No | Short-term needs under $20,000 |

| FHA Title I Loan | ~6.5–8.5% | ❌ No (up to $7,500) | Home improvements, government-backed |

For home improvements specifically, a fixed-rate home equity loan (HELOAN) eliminates the rate variability risk while still leveraging your equity. You get a lump sum at a locked rate. It’s less flexible than a line of credit, but in a volatile rate environment, that lack of flexibility is the feature, not the bug.

The Daily Fiscal Verdict

HELOCs in 2026 are not the same product they were in 2021. The environment has changed—rates are higher, home value appreciation has stalled, and the psychological risks remain constant.

The homeowners most at risk right now are those who opened HELOCs in 2020-2022 at low rates and are now in the middle of their draw period, treating the line of credit like ongoing household income. They haven’t experienced the repayment cliff yet. When they do—typically at year 10—the payment shock will be significant.

If you’re considering a new HELOC in 2026, ask yourself three questions:

- Can I absorb this payment if the rate increases by 2% in the next 3 years?

- Is there a version of this project I could fund through savings, personal loans, or a fixed-rate alternative that doesn’t put my home at risk?

- What’s my concrete, written repayment plan, and what assumptions does it depend on?

If the answers to those questions aren’t satisfying, reconsider. Equity is an asset. A HELOC converts that asset into a liability—with your home as the collateral.

Your 5-Step HELOC Reality Check

- Calculate your true LTV: Get a current appraisal (not Zillow). Divide your total debt (mortgage + HELOC) by the new appraised value. If LTV exceeds 85%, you have very little buffer.

- Run the “repayment cliff” scenario: Take your outstanding/planned HELOC balance. Calculate the monthly payment assuming principal + interest at current rates + 2%. Is that number sustainable?

- Compare against a personal loan: For amounts under $40,000, check current personal loan rates at Credible or LendingTree (covered in our previous guide). Often the rate difference is smaller than you expect—and your home isn’t on the line.

[!TIP] Run the Numbers: Our HELOC vs. Personal Loan Comparator lets you model your specific loan amount, credit score, and repayment timeline side by side—including what a 2% rate rise on the HELOC would do to your total interest cost.

-

Check your bank’s freeze policy: Ask directly: under what conditions can the bank freeze or reduce my HELOC? Most agreements allow them to do so if your home’s appraised value drops materially. Get this in writing.

-

Understand your full housing cost picture: If you’re considering a HELOC to fund home improvements, make sure you understand the true cost of ownership in your market first. Our home affordability guide covers the full cost model — including the 1% maintenance rule that explains why so many homeowners end up needing equity draws in the first place.

-

Consult a fee-only advisor: For HELOC decisions over $50,000, a one-time consultation with a fee-only fiduciary financial advisor (find them at NAPFA.org) may be worth considering. The typical fee ranges from $300-$500 and, importantly, these advisors do not earn commissions from product sales—their compensation structure is more aligned with objective analysis. This is not a guarantee of any particular outcome; individual advice quality varies by advisor.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Personal Finance

Personal Finance Rent vs Buy 2026: The Real Math Most Calculators Miss

Should you rent or buy a house in 2026? We run the full math — mortgage, opportunity cost, equity, and break-even — that most calculators ignore. Honest answer inside.

Personal Finance

Personal Finance Best CD Rates 2026: Lock In 5%+ Before Rates Drop

We ranked the best CD rates of 2026 across 6 terms — 3-month to 5-year. CIT Bank leads at 5.10% APY. Full rate table, ladder strategy, and when NOT to use a CD.

Personal Finance

Personal Finance Best HYSA Rates 2026: 7 Accounts Ranked by True APY

We ranked 7 high-yield savings accounts on APY, fees, minimum balances, and FDIC coverage. UFB Direct leads at 5.25% APY. Full rate table and winner picks inside.