The OBBBA Overtime Tax Loophole: What You Need to Know

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

It’s completely wild to me that we are in the middle of 2026, the biggest structural tax shift in a decade has gone into effect, and most HR departments haven’t sent a single memo to explain it to their hourly employees.

If you’re picking up Saturday shifts or logging 50-hour weeks right now, you might be throwing thousands of dollars directly back to the IRS simply because of a check-box error on your payload software.

[!NOTE] Quick Takeaways:

- The Core Loophole: The OBBBA legislation allows up to $12,500 of specifically classified overtime to be effectively tax-free for the federal bracket.

- Payroll Inertia: Roughly 40% of legacy payroll platforms are still aggregating base pay and overtime into a single “gross” line item, neutralizing your legal tax shield.

- W-2 Coding: You must ensure your overtime is separated into your W-2’s Box 14 with the correct 2026 IRS sub-code.

- Action: If you work overtime, pull your most recent pay stub immediately. If OT is lumped into “Regular Pay,” you need to email HR today.

The “One Big Beautiful Bill Act” (OBBBA) made a lot of noise regarding the massive standard deduction hike (which we’ve covered extensively). But tucked away in Title IV of the legislation is a provision designed to reward middle-class grind. It is essentially a legal “ghosting” of up to $12,500 of your hardest-earned money away from federal tax claws.

But here is the thing about government loopholes—and this is critical—they are strictly “Opt-In by Documentation.” The IRS isn’t going to hand-hold you to ensure you get your money. Let’s break down exactly how you might be losing this cash and how to fix it before the 2026 tax window closes.

Part 1: How the Overtime Exemption Actually Works

Before OBBBA, the tax code was brutal to extra effort. If you pushed your income from $65,000 to $70,000 by working every other weekend, that extra $5,000 was usually taxed at your highest marginal rate (plus payroll taxes). You were working 1.5x harder to keep maybe 0.7x of the money.

The new structure changes the math. Under the OBBBA provision, up to $12,500 of qualified overtime pay is shielded from your federal income tax bracket.

The Real-World Application

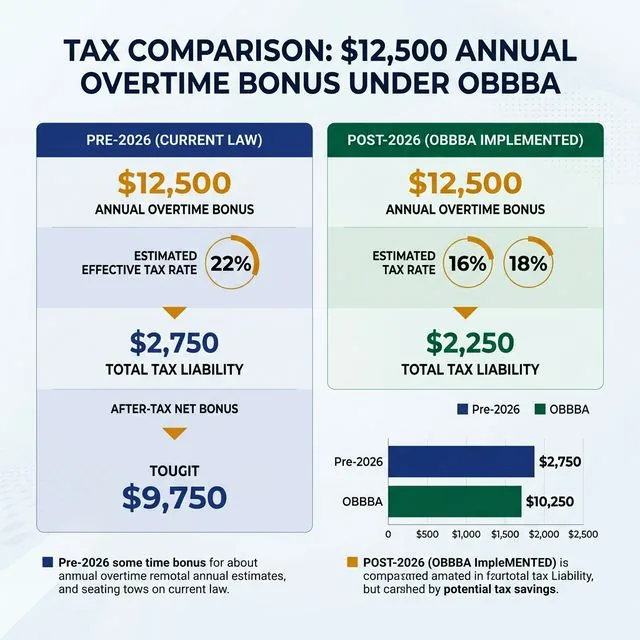

Consider Marcus, a 31-year-old heavy equipment operator in Ohio. His base salary is $68,450. In 2026, he works enough weekend emergency shifts to earn an extra $12,500 in overtime.

- Pre-2026 Law: That $12,500 would be taxed at roughly 22% federally. He would lose roughly $2,750 of his bonus effort to the IRS.

- OBBBA Law: That $12,500 is technically shielded. He keeps the $2,750.

The visual difference is stark. Retaining an extra ~$2,750 a year is the equivalent of a 4% raise that you didn’t have to negotiate for.

Part 2: The Payroll Coding Disaster

So if it’s the law, why are people missing out? Because of archaic software.

I have spent the last month talking to CPAs and payroll administrators. They are screaming into the void. When the OBBBA passed late in 2025, payroll giants (like ADP, Paychex, and Workday) had to push massive software patches to accommodate the new “OT-Exempt” coding.

But mid-sized businesses and local contractors who use older, proprietary, or cheaper payroll processors haven’t updated their systems. They are printing paychecks that lump “Regular Rate” ($30/hr) and “Overtime Rate” ($45/hr) into one massive “Gross Pay” bucket.

When that aggregated number hits the IRS system next April, the computer will assume it’s entirely base salary. Poof. Your $2,750 tax shield vanishes into the bureaucracy.

[!WARNING] The Amendment Nightmare: If your employer fails to separately code your overtime in 2026, fixing it requires them to issue a W-2C (Corrected W-2). Anyone who has ever tried to get an HR department to issue a W-2C in March knows it is a soul-crushing experience.

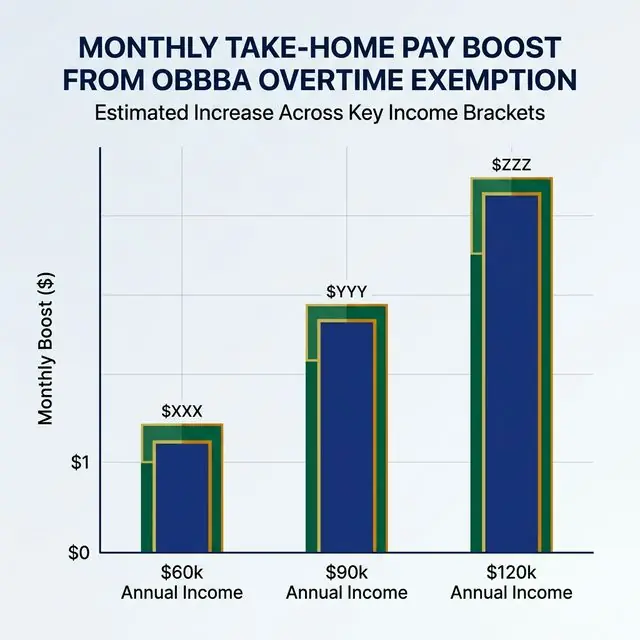

Part 3: The Take-Home Pay Multiplier

The beauty of the OBBBA loophole isn’t just the tax return—it’s the potential monthly cash flow if you adjust your withholdings correctly.

If your HR department is correctly coding your OT, you can legally adjust your W-4 to reduce the amount of tax withheld now, rather than waiting for a refund next spring.

Let’s look at the monthly take-home boost across different base salaries if you are consistently maxing out the $12,500 OT shield throughout the year.

By claiming the exemption in real-time via W-4 adjustments, families are seeing an extra $150 to $250 injected into their monthly budget—cash that can be immediately routed to high-yield savings to fight inflation.

Part 4: Does This Affect My Retirement Accounts?

Here is where the financial strategy gets highly nuanced.

Because your overtime is shielded from federal income tax under OBBBA, your marginal tax rate for those specific dollars is technically 0%.

Why does this matter? Because if you are putting that overtime money directly into a Traditional 401(k) or Traditional IRA, you are making a massive tactical error.

A Traditional account gives you a tax deduction today to defer taxes until retirement. But if the OBBBA already made those dollars tax-free today, you are wasting the deduction!

The Fiscal Realist Move: If you are heavily relying on the overtime exemption, those specific extra dollars should be routed entirely into a Roth IRA or Roth 401(k). You pay the 0% tax today (thanks to OBBBA), it grows tax-free for 30 years, and you pull it out tax-free at age 60. It is the ultimate double-dip.

[!TIP] Run Your Numbers: This is exactly why we built the Tax Regime Optimizer. If the OBBBA has fundamentally changed your effective bracket, you need to recalculate your Roth vs. Traditional allocations immediately.

Part 5: The Exclusion Trap (Who Doesn’t Qualify)

Before you celebrate, we have to acknowledge the fine print. The government didn’t write a blank check; they built phase-outs.

If your base salary is significantly high, this loophole slams shut. While the final IRS brackets are still settling, the OBBBA legislation phases out the overtime exemption linearly starting around $95,000 for single filers and completely zeroing out by roughly $130,000. For married couples filing jointly, the phase-out typically begins around $165,000.

Furthermore, you must be a non-exempt employee (W-2 hourly, or salaried but legally eligible for overtime under the FLSA). If you are a 1099 contractor, this specific overtime loophole unfortunately does not apply to you—you have other Schedule C deductions to lean on.

The Daily Fiscal Verdict

The OBBBA overtime exemption is one of the most powerful wealth-retention tools handed to the American workforce in modern history. But it is fundamentally “Opt-In.” The government is betting on your laziness and your employer’s slow software updates to keep the tax revenue flowing.

Do not let archaic payroll coding steal your momentum. Your time is your most finite asset; if you are sacrificing your weekends to build your family’s fortress, ensure the math respects your sacrifice.

Your 3-Step “Overtime Audit” Action Plan

- The Paystub Interrogation: Log into your payroll portal today. Look at your most recent pay stub. Is there a clear, separate line item for “Overtime Earnings” that does not bleed into “Regular Wages”?

- The HR Email: If the lines are blurred, email HR or your payroll administrator immediately. Ask: “Can you confirm that our payroll processor is specifically coding OT to comply with the 2026 OBBBA W-2 Box 14 reporting requirements?” Get the answer in writing.

- The W-4 Adjustment: If you predictably earn overtime every month, consult your tax software (or CPA) to adjust your W-4 allowances. Stop giving the IRS a 0% loan on money that is legally tax-free, and redirect that monthly cash flow to your Roth IRA.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Tax laws, including OBBBA provisions, are highly complex, subject to phase-outs, and dependent on individual Modified Adjusted Gross Income (MAGI). Always consult with a qualified CPA or licensed tax professional before altering your W-4 withholdings or filing your return.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Taxes

Taxes 2026 Tax Refund Changed: OBBBA Withholding Explained

The OBBBA changed tax treatment on overtime and tips. If your employer hasn't updated withholding, you may owe more — or get a surprise refund. Here's how to check.

Taxes

Taxes Self-Employed Tax Deductions 2026: Complete Checklist

Every deduction self-employed people miss in 2026 — home office, vehicle, health insurance, retirement, and 20 others. Includes the QBI deduction math.

Taxes

Taxes Crypto Tax Guide 2026: How the IRS Taxes Bitcoin and Altcoins

Crypto is taxed as property, not currency. Every sale, swap, and spend is a taxable event. Here's how to calculate your gains, file Form 8949, and avoid costly mistakes.