2026 Tax Refund Changed: OBBBA Withholding Explained

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

OBBBA Standard Deduction 2026: How It Changes Your Tax Refund

If you have already looked at your bank account this month, you might have noticed something unusual: The IRS is being… generous?

Early data from the 2026 tax filing season shows that the average tax refund represents a shock to the upside: $2,290. That is an 11% increase compared to this time last year.

Why the sudden windfall? It’s not luck. It’s the law.

The “One Big Beautiful Bill Act” (OBBBA)—legislation passed in 2025—has fully kicked in for this tax season. While the name is a mouthful, the math is simple: The government just made it significantly harder for the IRS to tax your first $32,000 of income.

[!NOTE] Quick Takeaways:

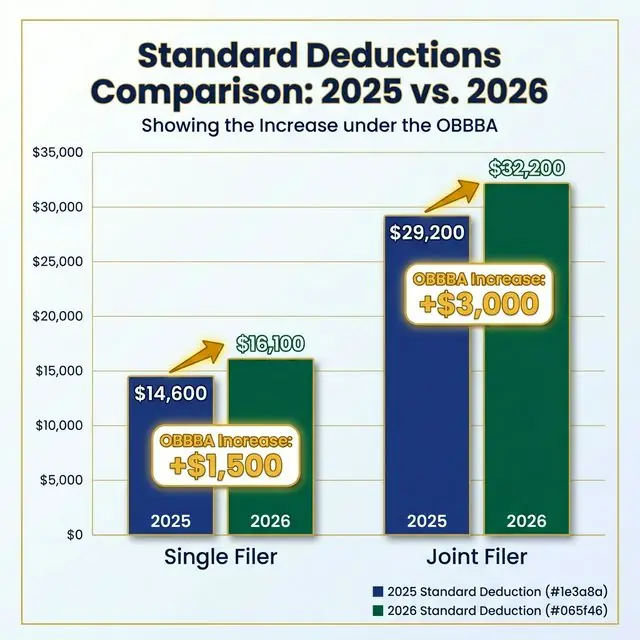

- Bigger Standard Deduction: Married couples can now earn $32,200 tax-free (up from ~$29k). Single filers get $16,100.

- Child Tax Credit Boost: Parents now get $2,200 per child, permanently.

- The “Blue Collar” Bonuses: New specific deductions for Overtime Pay and Tips are effectively tax-free for many workers.

- Action: If you traditionally “Itemize” your deductions, stop. The new Standard Deduction is likely higher than your itemized expenses, saving you hours of paperwork.

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: March 24, 2026

[!IMPORTANT] Verified Data Source: Standard deduction thresholds, tax brackets, and Child Tax Credit (CTC) provisions are sourced from IRS Publication 17/501 and the One Big Beautiful Bill Act (OBBBA) of 2025 legislative text. Last verified: March 2026.

Part 1: The “Standard Deduction” Super-Jump

The Standard Deduction is the amount of income the IRS lets you keep before they start touching your money.

For decades, this number crept up slowly with inflation. The OBBBA changed that trajectory.

- Married Filing Jointly: Now $32,200

- Single Filers: Now $16,100

- Heads of Household: Now $24,150

What this means for you: If you are a married couple earning $80,000 a year, your taxable income is instantly slashed to $47,800 before you even apply a single other credit. This massive reduction in taxable base is the primary driver of the $2,290 average refund we are seeing.

Part 2: The $2,200 Child Tax Credit (Permanent)

For parents, the constant “will they, won’t they” drama regarding the Child Tax Credit (CTC) is finally over.

The OBBBA has made the expanded credit permanent.

- Old Credit: $2,000 per child.

- New Credit: $2,200 per child.

- Inflation Protection: Starting in 2026, this number is indexed to inflation. If the cost of living goes up, so does your credit.

The Refundable Twist: Up to $1,700 of this credit is now “refundable.” That means if your tax bill is $0, the IRS will still write you a check for up to $1,700 per kid. For a family with two children, that is a potential $3,400 cash injection directly into your household budget.

Part 3: The “Overtime & Tips” Revolution

This is the most overlooked part of the new bill. The OBBBA specifically targeted hourly and service workers with two massive new benefits:

1. The Overtime Deduction

You can now deduct up to $12,500 of overtime pay (or $25,000 for couples).

- Scenario: You earn $50,000 base salary + $5,000 in overtime.

- Old Law: You pay taxes on $55,000.

- New Law: You pay taxes on $50,000. Your hard work is effectively tax-free.

2. The Tip Deduction

Service workers can now deduct up to $25,000 in qualified cash tips. This is a game-changer for bartenders, servers, and hospitality staff. It effectively legalizes the “tax-free tip” concept that many workers informally practiced, but now gives it the full protection of the law.

- Note: These deductions have income limits (phase-outs typically start at high income levels), so check with your tax software.

Part 4: Who Gets Left Behind? (The SALT Cap)

It’s not all good news.

If you live in a high-tax state like California, New York, or New Jersey, you might be frustrated by the SALT (State and Local Tax) Deduction Cap. While the OBBBA temporarily raised the cap to $40,000 (up from the punishing $10,000 limit of the previous era), it is still a cap.

- Good News: The jump to $40,000 solves the problem for 95% of homeowners.

- Bad News: If you pay $60,000 a year in property taxes, you are still losing out on $20,000 of deductions.

However, for the vast majority of Americans, the higher Standard Deduction ($32,200) renders itemizing irrelevant anyway.

The Daily Fiscal Verdict

The 2026 tax season is shaping up to be a “Refund Renaissance.” The combination of the higher Standard Deduction and the boosted Child Tax Credit means most middle-class families will pay significantly less federal income tax this year.

Don’t Spend It All at Once: If you receive that average $2,290 refund, consider the “30/30/40 Rule”:

- 30% to High-Interest Debt (Credit Cards).

- 30% to Savings (Lock in those 4.4% CDs we talked about!).

- 40% to Fun (You earned it).

Your Filing Checklist

- Wait for Forms: Ensure you have your W-2s and any new forms for Overtime/Tips verification.

- Check Your Status: If you got married or had a child in 2025, your refund could double.

- e-File Early: With these new complex credits, paper returns will be slower than ever. e-Filing guarantees a faster refund (typically 8-21 days).

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Tax laws are complex and subject to change. Always consult with a qualified tax professional or CPA before filing your taxes.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Taxes

Taxes The OBBBA Overtime Tax Loophole: What You Need to Know

The One Big Beautiful Bill Act created a tax-free overtime bracket that most workers haven't heard about. Here's how to claim it correctly on your 2026 tax return.

Taxes

Taxes Self-Employed Tax Deductions 2026: Complete Checklist

Every deduction self-employed people miss in 2026 — home office, vehicle, health insurance, retirement, and 20 others. Includes the QBI deduction math.

Taxes

Taxes Crypto Tax Guide 2026: How the IRS Taxes Bitcoin and Altcoins

Crypto is taxed as property, not currency. Every sale, swap, and spend is a taxable event. Here's how to calculate your gains, file Form 8949, and avoid costly mistakes.