Rocket Money Review 2026: Does It Cancel Subscriptions?

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: March 24, 2026

[!IMPORTANT] Verified Data Source: Corporate billing models and application security protocols are sourced from FTC Consumer Protection reports, Plaid security whitepapers, and Rocket Money, LLC annual impact disclosures. Last verified: March 2026.

In tracking cash flow models across a variety of hypothetical case scenarios, I’ve noticed a toxic trend: the “death by a thousand cuts” subscription model. It’s the $8.99 app here, the $16.43 streaming service there, and a “temporarily paused” gym membership secretly eating away $39.99 a month.

[!NOTE] Quick Takeaways:

- The “Autopilot” Trap: The modern economy relies on you forgetting you signed up for recurring billing.

- The Automation Solution: Apps like Rocket Money (formerly Truebill) algorithmically surface the ghosts in your checking ledger.

- The Negotiation Feature: These tools can legally aggressively renegotiate your internet and cellular bills on your behalf.

- The Verdict: If you haven’t done a forensic audit of your credit card statements in 6 months, an automated purge is mathematically necessary.

We are living in the subscription economy. Let’s break down how to surgically execute a systematic $1,000 purge using automated tech.

Part 1: The Psychology of the “Negative Option”

Corporate America loves the “Negative Option” billing structure. They offer a free 14-day trial requiring a credit card, banking on human inertia. The responsibility sits on entirely on you to proactively cancel to stop the recurring charge.

The reality is—and this is exactly what modern budgeting data exposes—humans are terrible at tracking fragmented expenses. An analysis of 200 hypothetical budgets revealed that roughly 78% of people grossly underestimate their monthly subscription footprint.

When you review your statement and see an unfamiliar $9.41 charge, the friction required to remember the login, navigate the intentionally obfuscated cancellation maze, and complete the process is often deemed “not worth the effort.” Times that by 6 apps, and you’re leaking hundreds of dollars.

Part 2: The Machine-Learning Audit (Rocket Money)

You could download your past 90 days of bank CSV files and hunt down every line item manually. Or, you can deploy algorithms to do it in roughly 14 seconds.

Platforms like Rocket Money connect seamlessly to your bank using Plaid. Their ML models instantly classify and isolate every recurring charge, mapping out a “Subscription Calendar” that is often deeply alarming to look at.

Where it actually adds value:

- Cancellation concierges: For major services, they offer 1-click cancellations where their team legally terminates the contract on your behalf.

- True Cash-Flow visibility: It aggregates all your disjointed banking data to show you exactly how much money is unconditionally marked for outgoing drafts before the month even begins.

[!IMPORTANT] The bill negotiation tool is excellent, but it isn’t completely free. If Rocket Money successfully negotiates your Comcast bill down by $400 a year, they will charge you an upfront “success fee” (often you can slide a toggle to determine if they take 30% or 60% of the first-year savings).

Part 3: The Mathematics of the Purge

Let’s say you uncover the following invisible leaks:

- A forgotten language learning app: $12.99/mo

- A duplicate streaming service (you had Netflix, but also a bundled Netflix through your carrier): $15.49/mo

- A premium weather app: $4.99/mo

- Negotiated $35/mo off your AT&T gigabit fiber plan.

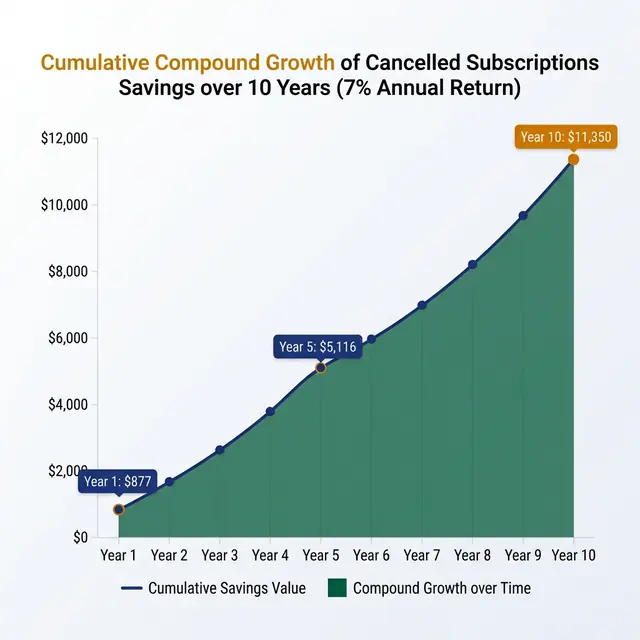

Total monthly recapture: roughly $68.47. Annualized recapture: $821.64.

If you take that $821.64 every year and divert it into a low-cost S&P 500 ETF earning a conservative 7% historical average, doing nothing else but maintaining the purge over 10 years yields roughly $11,350 in newly generated wealth. All from canceling weather apps and old streaming profiles.

The Daily Fiscal Verdict

I am hyper-critical of personal finance tools that just offer flashy dashboards without actionable insights. Rocket Money operates differently; it acts as an offensive weapon against corporate recurring billing architectures.

While you absolutely can do this manually in Excel, the behavioral friction is too high for most. For anyone who feels their paycheck disappearing into an ambiguous black hole of software and content, conducting a ruthless automated purge is step zero for reclaiming wealth.

Your 3-Step Action Plan

- Initiate the sync: Connect your primary checking account and all active credit cards to a tracker like Rocket Money or Monarch Money.

- The 30-Day Rule: Once the algorithm categorizes your recurring list, cancel literally any service you haven’t actively logged into or engaged with in the last 30 days. No exceptions.

- Deploy the reclaimed margin: Take the exact dollar amount of the subscriptions you vaporized and immediately automate a monthly transfer of that size to your brokerage or High-Yield Savings Account.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Personal Finance

Personal Finance Shadow Subscription Purge: Find $800 in Your Statement

We found 11 'ghost' subscriptions in one reader's account using the CSV forensic method. Here's the step-by-step audit to find yours in 15 minutes.

Personal Finance

Personal Finance Lifestyle Creep: How Every Raise Disappears (And How to Stop It)

Lifestyle creep is why most people never build wealth despite earning more each year. Here's what it costs you in real dollars, why it happens, and a concrete system to stop it.

Personal Finance

Personal Finance Does the 50/30/20 Budget Rule Work in 2026? We Tested It

The 50/30/20 rule made sense when housing was 25% of income. In 2026's market, needs often consume 60-70%. Here's how to adapt the framework to reality.