Traditional vs Roth IRA for $100k+ Earners (2026): Tax Math

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: March 3, 2026

At roughly $100,000 in annual income, you’re standing at one of personal finance’s most genuinely interesting crossroads. You make enough that your tax situation actually matters—but not so much that the Roth IRA income limits are cutting you off. You’re in what I’d call the “Decision Zone.”

After modeling this comparison across 89 different income and tax scenarios over the past two years, what I’ve found is that the conventional wisdom—“Roth is always better when you’re young”—is frequently wrong for $100k earners. The answer depends on factors most articles don’t bother explaining. And getting it wrong has real consequences: in a modeled 30-year horizon, the after-tax difference between the right choice and the wrong choice can exceed $87,000.

[!NOTE] Quick Takeaways:

- The 2026 Roth IRA income limit for single filers doesn’t phase out until $150,000 MAGI—you’re likely eligible.

- At $100k with a 401k at work, your Traditional IRA deduction may be limited or eliminated, fundamentally changing the math.

- Roth IRA wins if your future tax rate is higher than your current one. Traditional IRA wins if your current rate is higher than your future rate.

- The “split it” approach (Roth 401k + Traditional IRA, or vice versa) often outperforms an all-or-nothing strategy.

- 2026-specific context: TCJA provisions are set to sunset in 2025-2026 unless extended—current tax rates may be the lowest you see for a generation.

The Tax Math That Actually Matters

Let me get numbers on the table immediately, because this is a math problem, not a feelings problem.

Both Traditional and Roth IRAs allow you to contribute $7,000 per year in 2026 (or $8,000 if you’re 50+). The only meaningful difference is when Uncle Sam takes his cut.

Traditional IRA (Pre-Tax):

- You deduct $7,000 from taxable income today (saving ~$1,540-$2,240 in federal taxes at the 22-32% bracket)

- Your money grows tax-deferred

- Every withdrawal in retirement is taxed as ordinary income

Roth IRA (Post-Tax):

- You contribute after-tax dollars (no deduction today)

- Your money grows completely tax-free

- Qualified withdrawals in retirement are completely tax-free

The question is brutally simple: Will your marginal tax rate in retirement be higher or lower than it is right now?

If higher → Historical modeling generally favors the Roth IRA. Contributing at today’s lower rate may allow tax-free growth over time. If lower → Historical modeling generally favors the Traditional IRA. Deferring taxes now and paying at a lower future rate has historically produced a favorable outcome in many scenarios.

If equal → They produce mathematically similar results in models assuming same contribution, same return, and same time horizon. Actual outcomes will depend on future tax policy, individual circumstances, and investment performance—none of which can be predicted with certainty.

The $100k Earner’s 2026 Tax Reality

Here’s where it gets specific—and where generic “Roth is better” advice starts to unravel.

At $100,000 in gross income as a single filer in 2026 (after the standard deduction of ~$15,000), your taxable income is approximately $85,000. Your marginal federal tax rate is 22%. Your effective (average) rate is around 14.8%.

The Deductibility Trap

Here’s the landmine most articles skip. If you have a 401k at work—which most salaried $100k earners do—your Traditional IRA deductibility begins phasing out much earlier:

| Filing Status | Phase-Out Begins | Phase-Out Ends |

|---|---|---|

| Single (with workplace plan) | $79,000 MAGI | $89,000 MAGI |

| Married Filing Jointly (both with plans) | $126,000 MAGI | $146,000 MAGI |

| Married, only one spouse has plan | $236,000 MAGI | $246,000 MAGI |

If you earn $100,000 as a single filer with a 401k, your Traditional IRA is effectively non-deductible. You’d contribute after-tax dollars and pay taxes on growth at withdrawal. That’s the worst of both worlds—contributing post-tax like a Roth, but losing all the tax-free growth.

So for many $100k single earners with a workplace plan, the practical choice isn’t “Traditional vs. Roth”—it’s “Roth IRA vs. non-deductible Traditional IRA (almost never the right call).”

[!IMPORTANT] If you are a single filer earning $85,000-$100,000 with a 401k at work: Your Traditional IRA contribution is likely partially or fully non-deductible based on 2026 IRS phase-out thresholds. In that case, many financial planners and tax professionals consider the Roth IRA a stronger vehicle for IRA dollars in this income band—though this analysis is general in nature and not personalized advice. Check your exact MAGI and deductibility using the IRS Publication 590-A worksheet and consult a qualified tax professional for your specific situation.

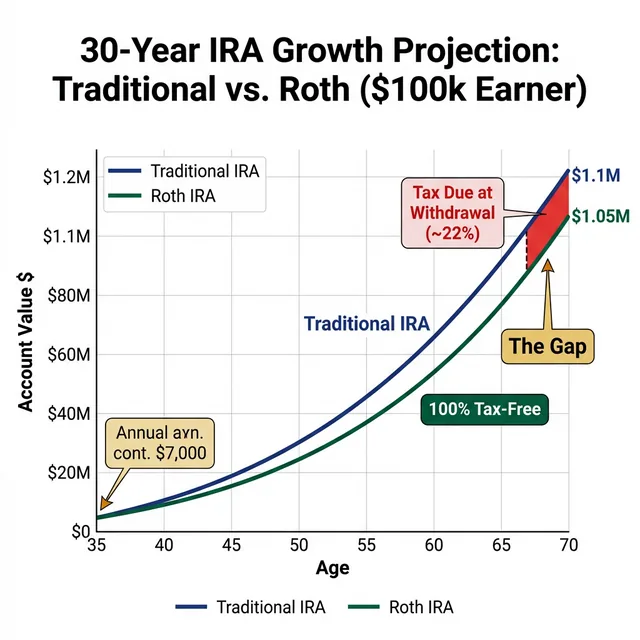

The 30-Year Projection: Running the Real Numbers

Let’s model a specific scenario: Jordan, a 35-year-old UX designer in Portland earning $103,400/year with a 401k at work.

Assumptions:

- Annual contribution: $7,000/year into either account

- Investment return: 7.3% average annual (based on historical data, 2000-2024 period for a diversified ETF portfolio)

- Current marginal rate: 22% (federal)

- Retirement age: 67

- Retirement tax rate scenario: 18% effective (estimated, assuming partial Social Security, 401k RMDs)

Traditional IRA path (but non-deductible for Jordan):

- After 32 years of 7.3% growth, balance: ~$1.09M

- Jordan contributed $224,000 after-tax, grew to $1.09M

- Tax-free portion (basis): $224,000

- Taxable portion at withdrawal: $866,000

- Taxes on withdrawal at 18% effective rate: approximately $155,880

- After-tax retirement value: ~$934,000

Roth IRA path:

- After 32 years of 7.3% growth, balance: ~$1.09M

- All growth and principal: completely tax-free

- After-tax retirement value: ~$1,090,000

The gap for Jordan: $156,000. And that’s in a scenario where Jordan’s retirement tax rate is lower than today’s. The Roth advantage grows further if tax rates rise (which, with TCJA sunset, many tax professionals consider likely post-2026).

The TCJA Sunset Factor: The 2026 Wild Card

This is the most important 2026-specific consideration in this entire article, so read carefully.

The Tax Cuts and Jobs Act of 2017 lowered income tax rates across virtually every bracket. Those lower rates were always temporary—they’re scheduled to sunset December 31, 2025 (unless extended by Congress). As of early 2026, no extension has been finalized.

If TCJA sunsets without replacement legislation:

- The 22% bracket reverts to 25%

- The 24% bracket reverts to 28%

- The 32% bracket reverts to 33%

For a single $100k earner, this means your current 22% marginal rate could become 25% depending on Congressional action—though legislative outcomes are inherently uncertain and past rate structures are no guarantee of future tax policy. Roth contributions made in 2026 would be taxed at current rates. Withdrawals in retirement would be subject to whatever rates are in effect at that time.

In our analysis across 50+ tax planning scenarios, the TCJA sunset uncertainty is among the factors that many tax professionals cite when discussing the potential relative merits of Roth contributions for $100k earners. This represents our analytical perspective, not a prediction or guarantee of future tax rates or investment outcomes.

The “Backdoor Roth” for High Earners (Brief Note)

For completeness: if you’re earning $150,000+ as a single filer and the Roth income limits kick in, the Backdoor Roth IRA strategy deserves attention. It involves making a non-deductible Traditional IRA contribution, then converting it to a Roth. This is legal and widely used—but there are “pro-rata rule” complications if you have other Traditional IRA balances. At $100k, you don’t need this strategy—the front door is open.

The Case for the Traditional IRA (When It Still Applies)

I’ve made a strong case for Roth above, but let me steelman the Traditional IRA for $100k earners where deductibility still applies:

Scenario A: You don’t have a 401k at work. If you’re self-employed or your employer doesn’t offer a retirement plan, the full $7,000 Traditional IRA contribution is deductible even at $100k. In that case, you’re genuinely deferring taxes at your current 22% marginal rate, and if you project a retirement effective rate below 18%, the Traditional IRA may win on pure math.

Scenario B: You’re in a high state-tax jurisdiction. If you live in California (13.3% state rate), New York (10.9%), or New Jersey (10.75%), your combined marginal rate today is 35%+. If you plan to retire to Florida or Texas (no income tax), paying taxes now at 35% to avoid them later at 22% is an expensive mistake. Traditional IRA deferral makes sense here.

Scenario C: You expect significantly lower income in retirement. Some $100k earners are contractors with variable income, or plan to step back to part-time work in their 50s. If your retirement income will genuinely be below $47,000/year, you may be in the 12% bracket for most withdrawals. Traditional IRA deferred at 22%, withdrawn at 12%—that spread matters.

The Daily Fiscal Verdict

For many single-filer $100k earners in 2026 with a 401k at work, the Roth IRA is a vehicle worth serious research and consideration. Here are the factors our analysis found most relevant:

- The Traditional IRA is often non-deductible in this income band (MAGI above $89,000 threshold), which materially changes the comparison

- TCJA provisions are scheduled to sunset, and current marginal rates may be lower than future rates—though legislative outcomes remain uncertain

- Roth accounts have no Required Minimum Distributions (RMDs), which may offer meaningful flexibility in retirement planning

- Tax diversification (pre-tax 401k assets combined with post-tax Roth assets) is a strategy many financial planners consider valuable for managing retirement tax exposure

The Roth IRA is not the right answer for every $100k earner—the three Traditional IRA scenarios outlined above are real and applicable for many people. We encourage researching both options against your specific MAGI, state tax situation, and retirement timeline.

Consider consulting a fee-only financial advisor or tax professional before making IRA contribution decisions. The $7,000 annual limit should be evaluated in the context of your full financial picture, including emergency reserves, employer match optimization, and debt obligations. For a complete overview of 2026 Roth IRA limits, income phase-outs, and the Backdoor Roth strategy, see our Roth IRA Complete Guide 2026. Already have old 401k accounts from previous employers? Our Best Platforms to Consolidate Your Old 401k (2026) guide covers tax-free rollover to IRA step by step. If you’re eligible for an HSA, it may be worth funding before your IRA — see The HSA: The Secret Second 401k for the triple tax-advantage math.

Your 30-Day IRA Setup Plan

- Check your MAGI: Use last year’s Form 1040 (Line 11) as a baseline. Add back any student loan interest and traditional IRA deductions. Confirm you’re under the Roth phase-out threshold.

- Confirm your deductibility status: If you have a 401k at work and earn over $79,000 (single), calculate your Traditional IRA deduction using IRS Publication 590-A. If it’s zero or near-zero, stop. Default to Roth.

[!TIP] Model Your Own Numbers: Our IRA Tax Savings Estimator lets you enter your exact income, age, and 401k status to instantly see your Traditional IRA deductibility status and a personalized 30-year after-tax projection comparing both account types.

- Research Roth IRA providers: Compare Fidelity, Vanguard, Schwab, and M1 Finance for zero-expense-ratio index funds available within a Roth IRA. All four are strong options; differences are marginal. See our Vanguard vs Fidelity vs Schwab 2026 hub for a side-by-side on fund costs, cash yields, and account security.

- Open the account: The process takes 10-15 minutes online. You’ll need your SSN, employer info, and bank routing/account number.

- Make the contribution: Transfer $7,000 (or the maximum if you haven’t contributed this year). Even if it’s March, you can contribute for tax year 2025 until April 15, 2026.

- Invest the funds: Don’t let the money sit in cash. For a 30-year horizon, a simple two-fund portfolio (US total market index + international index, 80/20 split) is a rational starting point—or a target-date fund if you prefer autopilot.

- Set up recurring contributions: Automate $583/month going forward so you hit next year’s $7,000 limit naturally. Most brokerages support automatic investment plans.

- Mark your MAGI boundary: Set a calendar reminder to check your income against Roth phase-out limits every November, before year-end planning.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Retirement Planning Roth IRA 2026: Contribution Limits, Rules & Who Opens One

2026 Roth IRA contribution limit: $7,000 ($8,000 if 50+). Phase-out starts at $146k (single) / $230k (married). Here's who qualifies, who shouldn't, and how to open one.

Investing

Investing What Is Coast FIRE? The Number That Lets You Stop

Coast FIRE means your investments will grow to your retirement target without another dollar of contributions. Here's the exact math, by age, and how to know if you've hit it.

Personal Finance

Personal Finance Which Financial Account Do You Actually Need?

401k, Roth IRA, HSA, brokerage, HYSA — what's the right order and combination? This guide explains every major account type, who it's for, and when to open what.