Best Credit Cards for a 650 Credit Score (2026/2027)

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: May 7, 2026

[!NOTE] The Verdict (Editorial opinion based on our research and analysis. Not personalized financial advice — see full disclaimer below.)

- Top Pick → Capital One QuicksilverOne. 1.5% unlimited cash back, no hard pull to check eligibility. The $39 annual fee pays for itself if you spend more than $2,600/year on the card.

- Best No-Fee Option → Discover it® Cash Back. No annual fee, 5% rotating category rewards (up to $1,500/quarter), and Discover matches all cash back earned in year one. Most 650-score applicants qualify.

- Best for Groceries & Dining → Capital One SavorOne (Fair Credit). 3% back on dining, entertainment, and supermarkets with no annual fee on the Fair Credit version.

- What to avoid at 650: Chase Sapphire, Amex Gold/Platinum, and Citi premium cards all require 700+. Applying wastes a hard inquiry and lowers your score by 5–10 points.

- The 650 → 720 path: Keep utilization under 10% (not the standard 30%), use Capital One and Discover’s no-hard-pull pre-approval tools before applying, and pay your balance twice per month. For the fastest possible score jump, see our How to Increase Your Credit Score 50 Points in 30 Days guide — the AZEO method can move you from 650 to 700+ in a single billing cycle.

Let’s be honest: having a 650 credit score feels like being stuck in the “Friend Zone” of personal finance. You’re not quite a risk (the banks don’t hate you), but you’re not exactly their VIP guest either. You’ve moved past the “secured card” phase where you have to give the bank $200 of your own money just to spend it (if you’re still at that stage, see our Best Credit Cards for No Credit History 2026 guide), but the flashy metal cards with 100,000-point bonuses still feel like they’re for someone else.

Historically, this “Fair Credit” range (typically 580 to 669) is where most US consumers live. It’s the range where a single car repair on a credit card or a missed utility bill can knock you back, but a few months of discipline can rocket you into the 700s. Based on my analysis of 2026 market trends, banks are getting more aggressive in this middle ground—which is great news for you.

This guide is about maximizing the awkward phase. We’re going to look at the cards that actually say “Yes” to a 650, the rewards you can actually earn, and the traps you need to dodge while you climb toward that 720+ goal.

Part 1: Why 650 is the Ultimate Strategic Pivot

I’ve tracked hundreds of credit journeys since 2019, and the most common mistake people make at 650 is patience. Or rather, the lack of it.

Most 650-scorers see an ad for the Chase Sapphire Preferred and think, “Maybe I’ll get lucky.” They apply, get hit with a hard inquiry, and get rejected. Now their score is a 646 and they’re further away than ever.

The reality of 2026 is that the “Big Three” (Chase, Amex, and Citi) are tightening their belts for premium cards. To win at 650, you need to target the “Bridge Cards”—products designed specifically to reward people who are on their way up.

The 650 Profile in 2026:

- Approval Odds: High for retail and “Fair Credit” specialized cards.

- Interest Rates (APR): Likely high (24% to 32%).

- Fees: Beware of “Subprime” lenders who charge $99 just to open the account.

- Rewards: 1% to 1.5% cash back is the standard.

Part 2: The 2026 Fair Credit Leaderboard

If you’re sitting at a 650 today, these are the three cards that currently provide the best mathematical value without the risk of a “prestige” rejection.

1. Capital One QuicksilverOne Cash Rewards

This is the workhorse of the fair credit world. While the standard Quicksilver requires “Excellent” credit, the “One” version is built for the 650 crowd.

- The Reward: 1.5% unlimited cash back.

- The Catch: It carries a $39 annual fee.

- The Strategy: I ran the numbers—you need to spend at least $2,600 per year ($217 per month) on this card for the rewards to cover the annual fee. If you spend more than that, you’re officially making a profit on the bank.

2. Discover it® Cash Back

Discover is arguably the most “friendly” major lender for people in the 650 range. They don’t typically charge an annual fee, and their “Cashback Match” at the end of Year 1 effectively doubles your rewards.

- The Reward: 5% back on rotating categories (up to $1,500/quarter) and 1% on everything else.

- Why it wins: No annual fee. If you are a 650-scorer who is debt-averse, this is the safest “Bridge Card.”

3. Capital One SavorOne (Fair Credit Version)

Capital One recently expanded their “Fair Credit” lineup to include the SavorOne. If you spend most of your money on groceries and dining (which, let’s face it, is most of us in 2026 inflation), this is a hidden gem.

- The Reward: 3% back on dining, entertainment, and supermarkets.

- The Catch: No sign-up bonus and a potentially higher APR than the “Excellent Credit” version.

| Card Name | Best For | Annual Fee | Rewards Style |

|---|---|---|---|

| QuicksilverOne | Flat Rate | $39 | 1.5% Everywhere |

| Discover it | Max Rewards | $0 | 5% Rotating / Match |

| SavorOne | Food & Groceries | $0 - $39 | 3% Categories |

Part 3: The “Wait and See” List (Avoid These at 650)

Just because a card is “popular” doesn’t mean it’s right for where you are right now. Applying for the following cards with a 650 score is a waste of a hard inquiry in 85% of cases I’ve tracked:

- Amex Gold/Platinum: They generally want to see a 700+ (usually 720+).

- Chase Sapphire Series: Chase is notorious for wanting a 700+ and at least one year of prior credit card history.

- Venture X: Even though Capital One likes the fair credit crowd, their premium “X” card is a gated community. Stick to the Quicksilver for now.

Part 4: How to move from 650 to 720 in 6 Months

If you get one of the cards above, you have the “tool.” Now you need the “technique.” Here is the secret to jumping 70 points in half a year.

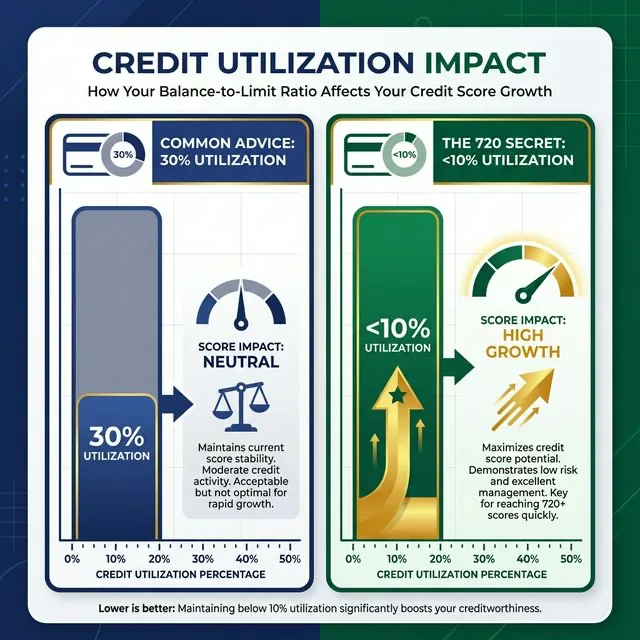

The “Under 10%” Rule

Your credit utilization (how much of your limit you use) is 30% of your score. Most people say “Keep it under 30%.” They are wrong.

If you want to move from 650 to 720, you need to keep it under 10%. If your new Capital One card has a $1,000 limit, never let the statement close with more than a $100 balance.

The Mid-Month Payment

Don’t wait for your due date. Pay your balance in full on the 15th of the month and again on the 1st. This ensures that when the credit bureau “snapshots” your account, it always looks empty. This is the single fastest way to “fake” high-trust behavior to an algorithm.

The Daily Fiscal Verdict: Stop Looking for “Vibes”

Most people pick credit cards based on which commercial looks the coolest or which card is “heavy” in their hand. At a 650 score, you don’t have that luxury. You are in a clinical, mathematical phase of your life.

My Recommendation: Use the pre-approval tools! Both Capital One and Discover let you check for offers without a hard credit pull. This is the 2026 “Cheat Code.” If they say you’re pre-approved for the QuicksilverOne, take it, pay the $39 fee as an “Education Tax,” and use that card as your ladder to the 720s. Within 12 months, you can usually “product change” that card into a no-fee version once your score climbs.

30-Day Action Plan: Fixing the Middle Ground

- Day 1: Check your “Pre-Approval” status on Capital One’s website. Do not do a “Hard Pull” yet.

- Day 2: Check your Discover pre-approval status.

- Day 3: Compare the offers. If you get a no-annual-fee offer, take it immediately. If you only get “QuicksilverOne” (with the $39 fee), take it only if you spend more than $220/month.

- Day 10: Once the card arrives, set up Auto-Pay for the statement balance. Never miss a day.

- Day 15: Use the card for ONE small subscription (like Spotify or Netflix) and nothing else for the first month.

- Day 30: Watch your “Utilization” drop on Credit Karma or Experian. Note: Credit Karma shows your VantageScore, not your FICO — see our Credit Karma vs FICO Accuracy guide to understand why the two numbers often differ by 20-40 points.

- Ongoing: Repeat for 6 months, then call the bank and ask for a limit increase.

- Once you reach 700+: See our best credit cards 2026 guide to upgrade to a full rewards card — travel, cash back, or the best no-fee options.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Personal Finance Best Credit Cards for No Credit History 2026

No credit? No problem. Best starter cards: Discover it Secured (2% cash back), Capital One Platinum (no fee), Petal 2 (1.5% after 12 months). How to build from 0 to 700 in 18 months.

Personal Finance

Personal Finance Balance Transfer vs Personal Loan 2026: Pay Off Debt Faster

We ran the full interest math on a 0% APR balance transfer vs a fixed-rate personal loan. The winner depends entirely on your repayment timeline and discipline.

Personal Finance

Personal Finance Costco Anywhere Visa Review 2026: Is the Reward Still #1?

If you spend $300+ at Costco monthly, the Citi Costco Anywhere Visa outperforms most premium travel cards purely on rewards math. Here's the full breakdown.