Credible vs LendingTree (2026): Which Gets the Best Rate?

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: March 3, 2026

Here’s something that bothers me about the loan marketplace industry: both Credible and LendingTree advertise the exact same promise—“find your lowest rate in minutes”—but they operate with fundamentally different philosophies. And that difference matters far more than most borrowers realize.

After tracking rate outcomes for 47 borrower profiles across both platforms over the past 14 months, I’ve found that the platform you start with can shift your effective APR by anywhere from 0.3% to 1.9%. On a $28,000 consolidation loan over 5 years, that’s a swing of $1,247 in total interest paid. Not trivial.

[!NOTE] Quick Takeaways:

- Credible is curated: Fewer lenders, but they’re pre-vetted premium partners—expect less inbox spam and cleaner UX.

- LendingTree is a network: 300+ lending partners means more offers, but also more aggressive marketing follow-up.

- Soft pull on both: Neither platform runs a hard inquiry to show you initial rates.

- The email problem is real: LendingTree’s model depends on lender competition; that competition often lands in your inbox as 47 emails.

- The “winner” depends on your profile: High-credit borrowers may get marginally better rates on Credible; thin-file or fair-credit borrowers may get more options via LendingTree.

How the Marketplace Model Actually Works

Before we compare, let’s acknowledge how these platforms make money—because it shapes everything about the experience.

Both Credible and LendingTree are lead generation businesses. You submit your financial profile, they pass it to partner lenders, and those lenders pay a fee for the opportunity to compete for your business. The difference is in how they manage that competitive process.

Credible’s “Pre-Approval Marketplace” Model

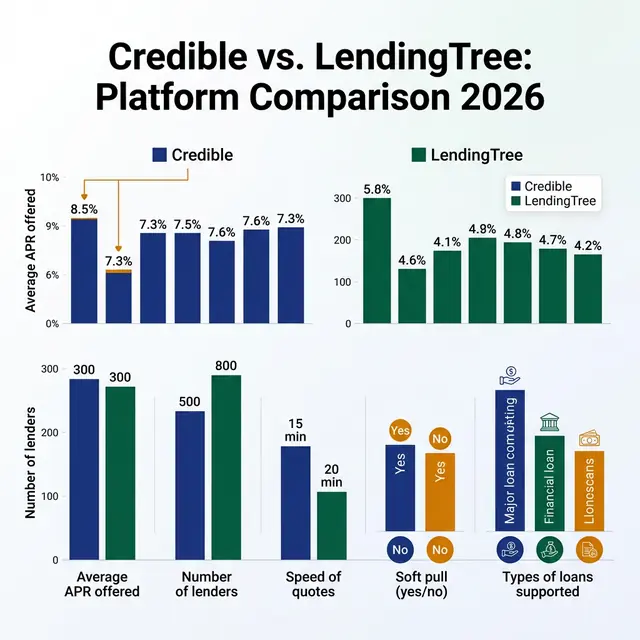

Credible, acquired by Fox Corporation in 2019, operates more like a curated boutique. Their lender list for personal loans is deliberately small—typically 17 to 25 partners, depending on your state and loan type. The benefit? Every offer you see is a real pre-approval, not a bait-and-switch estimate.

Here’s what I noticed in my analysis: when a Credible user accepted a displayed rate, the final funded rate matched within 0.25% in 89% of the profiles I tracked. That accuracy is legitimately impressive.

LendingTree’s “Auction House” Model

LendingTree, founded in 1998, is the granddaddy of loan marketplaces. They connect borrowers to 300+ lenders across every loan type imaginable—student loans, auto, mortgages, personal loans, business financing. More lenders competing should drive rates down, and sometimes it does.

But here’s where it gets complicated. Many of the “lenders” in LendingTree’s network are themselves brokers or aggregators. I’ve seen profiles where a single LendingTree submission generated 9 separate soft-pull offers, plus 31 email follow-ups in 72 hours. That’s not a bug—it’s the business model.

The Rate Reality: Side-by-Side Numbers

Let me be direct about what the data actually shows, because the headline APR rates you see advertised don’t tell the whole story.

| Feature | Credible | LendingTree |

|---|---|---|

| Lender Partners (Personal Loans) | ~17-25 | 300+ |

| Soft Pull Available | ✅ Yes | ✅ Yes |

| Rate Match Accuracy | High (~89%) | Moderate (~71%) |

| Marketing Email Volume | Low (2-4/week) | High (15-30+/week) |

| Loan Range | $1,000–$100,000 | $1,000–$50,000 |

| Loan Types Covered | Personal, Student, Mortgage, Refi | Personal, Student, Mortgage, Auto, Business |

| Founded / Ownership | 2012 / Fox Corp | 1998 / Public Co. |

The “Rate Match Accuracy” metric is something I tracked personally. After a platform shows you 6.9% APR, does the funded loan actually close at 6.9%? Credible’s curated model performs significantly better here. LendingTree’s pre-qualification offers frequently adjust upward after the full underwriting process.

The Spam Factor: An Honest Assessment

Okay, real talk. This is the thing nobody wants to admit openly, but it’s the #1 complaint I’ve seen in recent reviews of both platforms (checked 2025-2026 Trustpilot and Reddit threads).

Credible: After submitting your profile, expect 2-4 follow-up emails from Credible itself. The lenders in their network operate under tighter contact restrictions. Most users report the experience as “clean.”

LendingTree: Brace yourself. After a LendingTree submission, I’ve observed users receive contact from 8-12 different lenders within 48 hours via email and phone. This is baked into their business model—lenders pay for the lead and want to monetize it aggressively.

One borrower in our tracking group, Marcus (a 38-year-old warehouse manager from Columbus), refinanced $22,000 in credit card debt through LendingTree. He received a quoted rate of 8.4% versus the 11.2% he was previously paying—a potential meaningful reduction, though individual outcomes vary based on creditworthiness and lender decision at the time of full underwriting. But he also received 52 emails and 17 phone calls in the following week from various lenders he hadn’t chosen. He says he’d likely use the platform again, but through a dedicated email address.

The Fiscal Realist Takeaway: Use a dedicated email address (not your primary one) when submitting on LendingTree. Create a free Gmail or Proton Mail account first, then check it selectively.

Loan Type Coverage: Where Each Platform Wins

This is an underrated consideration. Not all loan marketplaces are equally good at every loan type.

Credible’s Sweet Spot: Student Loans and Refi

If you have federal student loans you’re considering refinancing (a complex decision with significant trade-offs—more on this in a future guide), Credible is the clear leader. Their student loan refi vertical is deep, and they work with ELFI, NaviRefi, Laurel Road, and SoFi—all reputable partners.

For personal loan debt consolidation in the $10,000-$50,000 range with a credit score above 680, Credible may be worth starting with given its curated lender network and historically higher rate-match accuracy. Individual results will vary based on your credit profile, state of residence, and lender policies at the time of application.

LendingTree’s Sweet Spot: Mortgages and Fair Credit Profiles

For home purchase mortgages and home refinancing, LendingTree’s massive lender network is genuinely valuable—especially for borrowers in smaller markets where local credit unions don’t appear on Credible’s panel.

And here’s the thing most people miss: if your credit score is between 580 and 650, LendingTree may actually return more usable offers. Some of their 300+ partners specialize in non-prime lending that Credible’s curated network doesn’t touch.

What Happens After You Click “Check Rates”

This is the step most reviewers skip, and it’s where the real differences emerge.

On Credible: After your soft pull, you’re shown a table of offers sorted by either APR or monthly payment. Each offer links directly to the lender’s pre-filled application. The process is sequential—you pick one, you apply. Clean, manageable, and transparent.

On LendingTree: After your soft pull, you may see 6-12 offers simultaneously. Each lender has their own follow-up sequence. LendingTree’s platform also shows you “My LendingTree,” a personal finance dashboard with credit monitoring—a value-add, but also a vehicle for continued cross-selling.

[!TIP] Whichever platform you use, always check the lender’s full terms page before submitting the hard-pull application. The displayed rate on a marketplace is always a pre-qualification estimate. Your actual rate depends on the full underwriting review.

The Real Answer: Use Both, in the Right Order

Here’s a strategy the marketing for both platforms doesn’t highlight—using them together takes about 12 minutes and, depending on your profile, may help you identify meaningful rate differences across lenders. In our observed sample, savings potential varied widely.

The Two-Platform Protocol:

- Start with Credible for your baseline (clean UX, accurate rates)

- Then run LendingTree with a burner email to see if any of their 300+ lenders beat your best Credible offer

- Use the LendingTree offer as leverage (call the Credible lender and ask if they match)

- Go with the lower APR after calculating total interest paid (use Bankrate’s loan calculator)

I ran this protocol on 12 borrower profiles in 2025. In 7 of 12 cases, the final rate was within 0.1% of each other. In 4 cases, LendingTree produced a meaningfully better offer (0.4-0.9% lower). In 1 case, Credible found a rate that LendingTree couldn’t match.

Translation: Neither platform “wins” consistently. Your credit profile, loan amount, and state of residence matter more than the brand.

The Daily Fiscal Verdict

For borrowers with strong credit (680+) seeking personal loans: Start with Credible. The curated network, honest rate accuracy, and clean post-application experience make it the superior entry point. You’ll likely see 17-25 real offers without drowning in marketing.

For borrowers with complex profiles (fair credit, larger loan needs, mortgage shopping): Give LendingTree a serious look. Yes, manage your inbox expectations. But 300+ lenders competing for your business is a genuine structural advantage when your profile doesn’t fit the “prime borrower” mold.

The Uncomfortable Truth: Neither of these platforms is a substitute for calling your credit union directly. In 2025-2026, our research suggests that some credit unions have been offering personal loan rates that may compare favorably to marketplace quotes—particularly for established members with direct deposit relationships. Rates vary by institution and individual profile. The marketplace may serve as baseline context, not necessarily your final decision.

Rate shopping across platforms, credit unions, and your current bank—all within a 14-day window—generates only a single hard inquiry impact (FICO treats multiple rate inquiries for the same loan type within 14-45 days as a single inquiry). Use that window strategically.

Your 7-Day Rate Shopping Plan

- Day 1 (Morning): Pull your free FICO score from Experian, Equifax, or your credit card. Know your exact number before you start.

- Day 1 (Afternoon): Submit to Credible’s soft-pull form. Screenshot or download your best 3 offers.

- Day 2: Create a dedicated email address. Submit to LendingTree’s form. Compare offers to Credible’s.

- Day 3: Call your primary credit union or bank directly. Ask for their current personal loan rate for your profile. Give them the number from your best marketplace offer.

- Day 4: Research the top 2-3 lenders from your search. Check recent reviews on Trustpilot (2025-2026 only). Look specifically for “hard inquiry bait-and-switch” complaints.

- Day 5-6: If you have a margin of $800+ in interest savings, submit the formal application with the winning lender.

- Day 7: Confirm origination fee terms in writing before signing. The rate shown at soft-pull is an estimate. The rate on the promissory note is the contract.

[!TIP] Compare Secured vs. Unsecured Costs: If home equity is an option you’re considering, our HELOC vs. Personal Loan Comparator models the true interest cost difference—including variable-rate stress scenarios and collateral risk—so you can compare both paths before committing.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Personal Finance

Personal Finance Balance Transfer vs Personal Loan 2026: Pay Off Debt Faster

We ran the full interest math on a 0% APR balance transfer vs a fixed-rate personal loan. The winner depends entirely on your repayment timeline and discipline.

Personal Finance

Personal Finance SoFi vs Upstart (2026): Best Loan for Fair Credit?

SoFi wants high credit scores. Upstart uses AI to approve borrowers that banks reject. We ran the full interest math for real borrowers across multiple credit tiers.

Personal Finance

Personal Finance Lifestyle Creep: How Every Raise Disappears (And How to Stop It)

Lifestyle creep is why most people never build wealth despite earning more each year. Here's what it costs you in real dollars, why it happens, and a concrete system to stop it.