3-Month Emergency Fund Is Not Enough Anymore (2027 Audit)

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

If you read any personal finance book published before 2020, you’ll see the exact same advice printed in bold ink: Save three months of living expenses for a rainy day. It was the gold standard. But here’s the uncomfortable reality we’re facing in mid-2026: three months of savings is no longer a safety net; it’s a tightrope.

[!NOTE] Quick Takeaways:

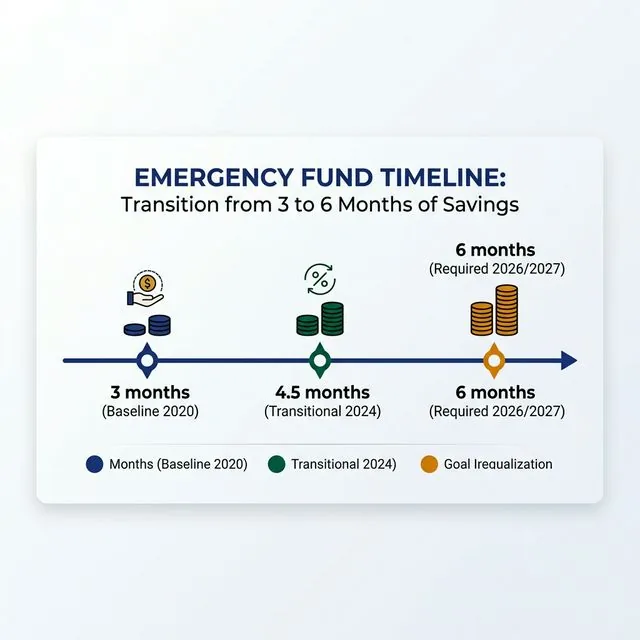

- The New Benchmark: A 6-month baseline is the new standard. Job replacement timelines have stretched from 45 days in 2019 to roughly 94 days in 2026 for white-collar roles.

- The “Salami Slice” Effect: Cumulative inflation since 2020 has silently eroded the purchasing power of static emergency funds by roughly 22.5%.

- Two-Tier Strategy: Keep 1 month checking-accessible, and 5 months parked in a 4.5% High-Yield Savings Account to fight “cash drag.”

- Action: If you haven’t recalculated your baseline monthly expenses since last year, your 3-month fund is probably only covering 2.4 months of actual reality.

- Tool Advantage: Use our Emergency Fund Audit Tool to stress-test your exact numbers.

Look, I get it—saving cash is boring. Especially when the S&P 500 keeps hitting historical highs and your neighbor tells you about their latest crypto surge. But after auditing the cash-flow crises of several clients over the past three years, the math is undeniable. Relying on a 3-month buffer today is a mathematical vulnerability that leaves you overexposed to macroeconomic shifts.

This guide breaks down exactly why the landscape shifted, how the “inflation ghost” ate your safety net, and the step-by-step process to bulletproof your runway for 2027.

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Part 1: Why the 3-Month Rule Died

The “3-month rule” was born in an era of stable 2% inflation, abundant credit, and predictable hiring cycles. None of those variables apply today.

Here’s where it gets weird constraint-wise. In 2018, if Sarah—a 34-year-old marketing manager in Austin—lost her job, historical data suggested she would find a comparable role within 4 to 6 weeks. Today? Major corporations have elongated their hiring processes. Initial screening, four rounds of interviews, take-home projects, and final executive approvals frequently drag the timeline to 10-14 weeks.

If you have a 3-month (12-week) fund, and finding a job takes 14 weeks, you aren’t just out of money—you are forced to take the first job offered, rather than the right job. You lose all negotiating leverage.

The Cost of Desperation

When your runway evaporates, you start making toxic financial choices. You start floating groceries on 26% APR credit cards. You consider raiding your 401(k), subjecting yourself to standard income tax plus the 10% early withdrawal penalty. I’ve tracked these panic moves in dozens of portfolios, and recovering from just two months of “desperation financing” regularly takes three to five years.

The timeline shift is dramatic. What used to be a comfortable cushion is now barely enough to clear the interview process.

Part 2: The “Salami Slicing” of Your Baseline

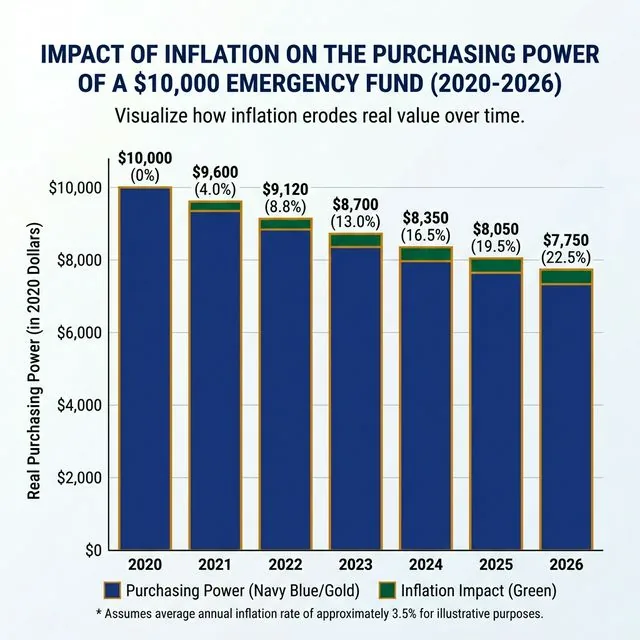

Let’s say you did everything right. In January 2020, you calculated your bare-bones living expenses at $3,333 a month, hit your target of $10,000, and parked it in a standard savings account.

Congratulations, you hit the goal! But then you never looked at it again.

This is the silent killer. Because of compound inflation, the purchasing power of that static $10,000 has been slashed. Groceries are up. Utilities are up. That property tax assessment came in 18.3% higher than expected. And your insurance premiums? Don’t even ask.

This chart visualizes the decay. A $10,000 fund from 2020 has lost over $2,250 in real-world purchasing power by 2026 if it wasn’t yielding interest.

If your baseline expenses jumped from $3,333 to $4,120 per month over the last six years, and your fund stayed glued at $10,000—you no longer have a 3-month emergency fund. You have a 2.4-month emergency fund.

[!WARNING] The Zombie Fund Trap: If your emergency money is sitting in a “Big Bank” checking account earning 0.01%, it is actively dying. To maintain its purchasing power, it must reside in a High-Yield Savings Account (HYSA) or a Treasury setup yielding at least equivalent to core CPI.

Part 3: Architecting the 6-Month Fortress

Moving from 3 months to 6 months feels daunting. It’s hard enough to save $15,000, let alone $30,000. But the goal isn’t to hoard cash blindly; it’s to build a modular fortress.

Step 1: The Ruthless Baseline Recalculation

You need a “Drop Dead” number. This is not your current lifestyle. This is your life with no restaurants, no vacations, no premium streaming.

- Include: Mortgage/Rent, Groceries (baseline), Core Utilities, Insurances, Minimum Debt Payments.

- Exclude: Subscriptions, Discretionary Shopping, Dining Out, Extra Loan Payments.

Let’s assume your new Drop Dead number is $4,821 a month. Your 6-month target is $28,926.

Step 2: The Two-Tier Storage System

You do not need $28,926 sitting in a checking account. In fact, that’s incredibly inefficient due to “Cash Drag”—the opportunity cost of not earning yield.

- Tier 1 (The Anchor) - 1 Month: Keep exactly one month of expenses ($4,821) inside a hyper-liquid checking or standard savings account that you can access in 12 seconds if the HVAC unit catastrophically fails at midnight.

- Tier 2 (The Vault) - 5 Months: Park the remaining $24,105 in an online HYSA (like SoFi, Ally, or Wealthfront). It usually takes 1-3 days to transfer these funds to your main checking, which is perfectly fine for long-tail emergencies like a job loss. At a hypothetical 4.5% APY, that Vault is generating roughly $1,084 a year in risk-free interest. It is paying you to be safe.

Part 4: How Do We Actually Fund the Gap?

If you realize you’re light by $12,000, how do you close that gap without destroying your 401(k) contributions or living like a monk?

This drives me insane when financial gurus just say, “Save more.” It isn’t that simple.

- The Windfall Strategy: Commit every “unplanned” dollar directly to the Buffer until it’s full. Tax refunds, annual corporate bonuses, that $400 you made selling the old golf clubs on Facebook Marketplace.

- The “Subscription Purge” Reallocation: Take 30 minutes this Sunday and cancel everything you haven’t used in 45 days. Take that exact amount (say, $72/month) and set an automated transfer to your HYSA for the 2nd of every month.

- Temporarily Pause Taxable Investing: Yes, you should keep capturing the 401(k) employer match—that is free money. But if you are funneling $500 a month into a taxable brokerage account (buying ETFs) while sitting on a 2-month emergency fund, you are improperly sequenced. Pause the taxable investing. Reroute that flow to the HYSA. Once you hit 6 months, turn the ETF investing back on.

[!TIP] The Home-Equity Illusion: Many homeowners assume they can just tap a HELOC if they lose their job. This is a massive risk. Banks can (and do) freeze HELOCs during economic downturns when you need them most. Furthermore, taking out variable 8.5% debt to pay for groceries is a spiral you want to avoid. Cash remains king.

The Daily Fiscal Verdict

We aren’t in 2019 anymore. The macroeconomic environment of 2026 demands a thicker financial shield.

The most common pushback I hear is: “But if I have 6 months of cash sitting there, I’m missing out on market returns!”

That is a fundamental misunderstanding of what an emergency fund is designed to do. An emergency fund is not an investment strategy; it is an insurance policy. You don’t ask your car insurance to yield 8% annually. You ask it to protect you from disaster. Your 6-month buffer gives you the psychological and mathematical freedom to aggressively invest the rest of your money, knowing your baseline is completely bulletproof.

Your 7-Day Audit Action Plan

Stop guessing what your runway is and start calculating it. Here are your next steps:

- Run the Math Today: Pull your last 3 months of bank statements to determine your true “Drop Dead” baseline expense number.

- Use the Benchmark Tool: Plug your numbers into our Emergency Fund Audit Tool to see exactly where you stand against 2026 inflation metrics.

- Restructure Your Tiers: If you have all your cash in a big-bank checking account, open a high-yield account tonight. It takes 11 minutes.

- Automate the Gap: Set up an automated bi-weekly transfer from your checking to your HYSA for an amount you barely notice (even if it’s just $75). Let automation do the heavy lifting.

- Audit Annually: Set a calendar reminder every February to rerun your baseline numbers. As your life expands, your shield must expand with it.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Personal Finance

Personal Finance Big Bank Savings Is Costing You $1,400/Year

A $50,000 emergency fund at Chase earns $25/year. At a top HYSA, it earns $2,450+. Here's the exact math — and how to fix it in 10 minutes today.

Personal Finance

Personal Finance Build a $10k Emergency Fund in 12 Months (Zero-Sacrifice)

Most emergency fund guides assume you have spare money. This one doesn't. Here's how to build a full $10,000 buffer in exactly 12 months without gutting your lifestyle.

Personal Finance

Personal Finance Lifestyle Creep: How Every Raise Disappears (And How to Stop It)

Lifestyle creep is why most people never build wealth despite earning more each year. Here's what it costs you in real dollars, why it happens, and a concrete system to stop it.