Fed Pivot Warning: Lock In CD Rates Before They Drop

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Best CD Rates to Lock In Right Now Before the Fed Pivots (2026 Guide)

For the last 18 months, being lazy with your money has been profitable.

You could leave $50,000 in a High-Yield Savings Account (HYSA), do absolutely nothing, and watch it generate $2,300 a year in risk-free interest. It was the “Golden Era” of Cash.

But after the Federal Reserve’s January 2026 meeting, the music is about to stop.

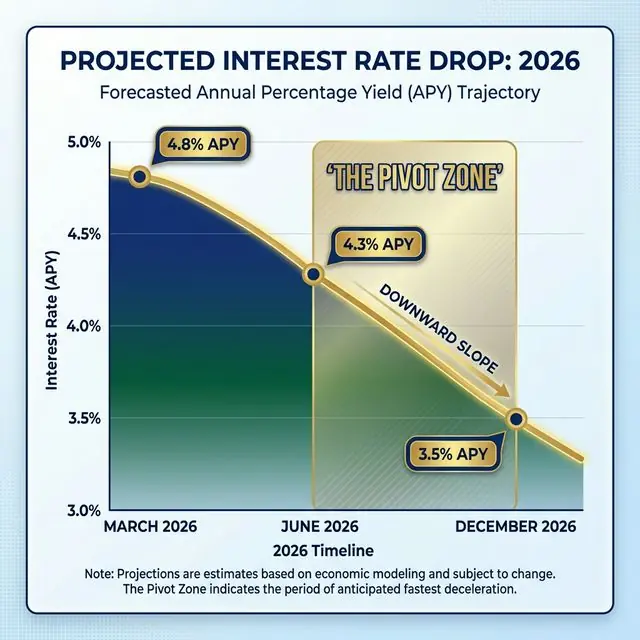

The Fed has officially signaled a “Pause,” and the bond market is screaming that a Rate Cut is coming by mid-year. What does this mean for you? It means the 4.2% - 4.6% APY you see on your savings app today is likely the highest it will be for the next decade.

[!NOTE] Quick Takeaways:

- The Window is Closing: Banks front-run the Fed. CD rates will start dropping weeks before the official rate cut announcement.

- Variable vs. Fixed: Your HYSA rate is variable (it will drop). A Certificate of Deposit (CD) is fixed (it stays high).

- The “Ladder” Strategy: Don’t lock all your cash up at once. Split it into 6-month, 12-month, and 18-month buckets to balance liquidity and yield.

- Inflation Hedge: With inflation cooling to 2.4%, a 4.4% guaranteed return is a massive 2.0% “Real Yield”—wealth building on autopilot.

- Action: If you have cash sitting in a checking account earning 0.01%, you are literally setting money on fire.

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: March 24, 2026

[!IMPORTANT] Verified Data Source: CD rate benchmarks and Federal Reserve policy projections are sourced from FDIC National Rate Averages, Bankrate Weekly surveys, and the Federal Open Market Committee (FOMC) target range projections for 2026. Last verified: March 2026.

Part 1: Why the “Pause” is Actually a Warning

When Jerome Powell and the Federal Reserve “Pause” rate hikes, it’s not a vacation. It’s a signal that they believe inflation is under control and the economy is cooling.

History Lesson: In every major rate cycle since 1990, the “Plateau” (the period where rates stay high) lasts roughly 6 to 9 months. We entered this plateau in late 2025. That puts the “Cut Zone” squarely in May or June 2026.

The “Bank Pre-Emption” Effect

Banks aren’t stupid. They know rates are going down. They don’t want to be stuck paying you 5% interest on a 5-year CD when the market rate drops to 3% next year. So, they will start slashing CD yields now. We are already seeing it.

- November 2025: 1-Year CD Average High: 5.15%

- February 2026: 1-Year CD Average High: 4.25%

That 0.9% drop happened while the Fed did nothing. Imagine what happens when they actually cut.

Part 2: The Logic of the “Lock-In”

This is a mathematical game of “Chicken.”

If you keep your money in a High-Yield Savings Account (like SoFi or Ally), you are enjoying ~4.3% APY right now. Scenario A (No Action):

- March: Rate stays 4.3%.

- June (Fed Cuts): Rate drops to 3.8%.

- September (Fed Cuts Again): Rate drops to 3.3%.

- December: Rate drops to 2.9%.

- Your Average 2026 Yield: ~3.5%.

Scenario B (The CD Lock):

- Today: You move $10,000 into a 12-Month CD at 4.4%.

- June: Interest rates crash. Your CD pays 4.4%.

- December: Interest rates crash further. Your CD pays 4.4%.

- Your Average 2026 Yield: 4.4%.

On a $50,000 emergency fund, the difference between taking action today and waiting six months is roughly $450 in lost passive income.

Part 3: The “CD Ladder” Defense (Don’t Trap Your Cash)

The biggest fear people have about CDs is “locking up” their money. What if you lose your job? What if your car explodes?

This is why smart money uses a CD Ladder.

Instead of putting $20,000 into a single 1-Year CD, you split it:

- $5,000 into a 6-Month CD (4.2% APY)

- $5,000 into a 12-Month CD (4.15% APY)

- $5,000 into an 18-Month CD (4.0% APY)

- $5,000 kept liquid in a HYSA.

Why this works: Every six months, a chunk of your money “matures” and becomes available penalty-free.

- If you need it? Take it.

- If you don’t? Re-invest it into a new long-term CD. This gives you the liquidity of a savings account with the yield protection of a bond.

Part 4: No-Penalty CDs (The “Cheat Code”)

If you are truly paranoid about needing access to your cash, look for “No-Penalty CDs” (Ally Bank and Marcus by Goldman Sachs are famous for these).

A No-Penalty CD allows you to withdraw your full balance and interest typically just 7 days after funding, with zero fees.

- Current Rate: ~3.8% - 4.0%

- Pros: Total freedom.

- Cons: Slightly lower rate than a standard CD.

Fiscal Verdict: In 2026, a No-Penalty CD is strictly better than a High-Yield Savings Account. It has the same liquidity (roughly), but the rate is fixed for 11 months. It’s a free insurance policy against the Fed.

The Daily Fiscal Verdict

We are living through the final days of risk-free 4.5% returns.

Future you—the version of you living in 2027 when savings rates are back down to 3%—will look back at February 2026 as the moment you either capitalized on the “Peak Rate” or let it slip through your fingers.

It takes roughly 15 minutes to open a CD online. Do it before the next Fed meeting.

Your 60-Day Action Plan

- Check Your Idle Cash: Look at your checking and savings. Keep 2 months of expenses liquid.

- Identify “Lazy Money”: Anything beyond 3 months of expenses should be working harder.

- Rate Shop: Look for 12-month CDs yielding above 4.2%. (Check Marcus, Capital One 360, and Ally).

- Ladder It: Split the deposit into 3 chunks with different maturity dates.

- Sleep Well: Enjoy your guaranteed return while the rest of the market panics about “Fed Cuts.”

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Investing

Investing Is Your HYSA Ghosting You? Banks Cut Rates Early

Banks pre-cut HYSA rates weeks before the Fed announces anything. Here's how to detect the quiet drop, lock in a CD at today's rate, and stop leaking yield.

Investing

Investing 20% Market Crash Impact on Your Portfolio (2026 Stress Test)

We stress-tested a standard $150,000 portfolio through a 20% drawdown. The pain is recoverable — if you don't panic sell. Here's the math that proves it.

Investing

Investing RSU Taxes 2026: What You Actually Keep After the IRS

RSUs look like free money until they vest and the tax bill arrives. Here's exactly how RSU taxation works, what your take-home actually is, and how to plan for the bill.