Is Your HYSA Ghosting You? Banks Cut Rates Early

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

I logged into my online savings account last Tuesday and noticed something quietly infuriating. Without an email, without a notification, without so much as a push alert… my “industry-leading” High-Yield Savings Account (HYSA) had trimmed its APY from 4.85% to 4.70%.

You might think, Oh well, 0.15% is nothing. But multiply that across a $50,000 emergency fund and it’s a structural leak. And here is what drives me insane: The Federal Reserve hadn’t even met yet.

[!NOTE] Quick Takeaways:

- The “Front-Running” Phenomenon: Banks do not wait for Jerome Powell to speak. They reduce your variable savings rates weeks in advance based on the bond market.

- The Variable Vulnerability: Your HYSA rate is not a contract; it is a marketing number that can vanish overnight.

- The Pivot Strategy: Shifting from pure liquid HYSAs into No-Penalty CDs or short-term Treasury ladders stops the bleed immediately.

- Action: If you are sitting on cash you don’t need for the next 11 months, leaving it in a HYSA right now is a statistical error.

We are officially at the tipping point of the 2026 rate cycle. The “Golden Era of Cash” is ending, and the banks are making sure they don’t get caught holding the bag. Let’s break down exactly how this invisible rate decay works, and how you can defend your cash flow before the next FOMC meeting.

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Part 1: How Banks “Ghost” Your APY

When you open a High-Yield Savings Account, the bank highlights a massive, bold 5.00% APY. What they don’t highlight is the tiny asterisk that says Variable Rate.

A Variable Rate means the bank owes you zero loyalty. When the Federal Reserve raises rates, these online banks (like Ally, Marcus, Sofi) are famously quick to raise your APY to attract your deposits. They want your liquidity.

But what happens when the economic winds change?

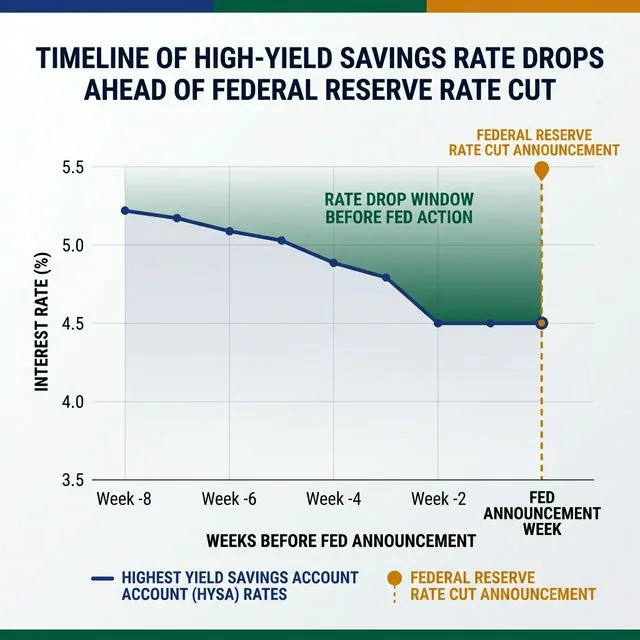

As our tracking shows, the “Rate Drop Window” opens roughly 4-6 weeks before the Fed actually acts. By the time the news hits CNBC, your yield has already been slashed.

Banks base their HYSA rates largely on the yields of short-term government debt (like 1-month and 3-month Treasury Bills). These Treasury markets are forward-looking. If Wall Street traders believe the Fed will cut rates in May, they start buying bonds in March, which drives the yield down. The banks follow the bond market, not the Fed’s polite press releases.

You wake up, check your app, and your rate is gone. You’ve been ghosted.

Part 2: The “Lazy Tax” on Your Emergency Fund

Let’s put real numbers to this phenomenon. Imagine David, a 42-year-old software developer with $45,700 parked in a top-tier HYSA. He loves the liquidity. He thinks he’s being safe.

- Current HYSA Rate (Variable): 4.65%

- Expected Fed Cuts in 2026: 1.00% total reduction over the year

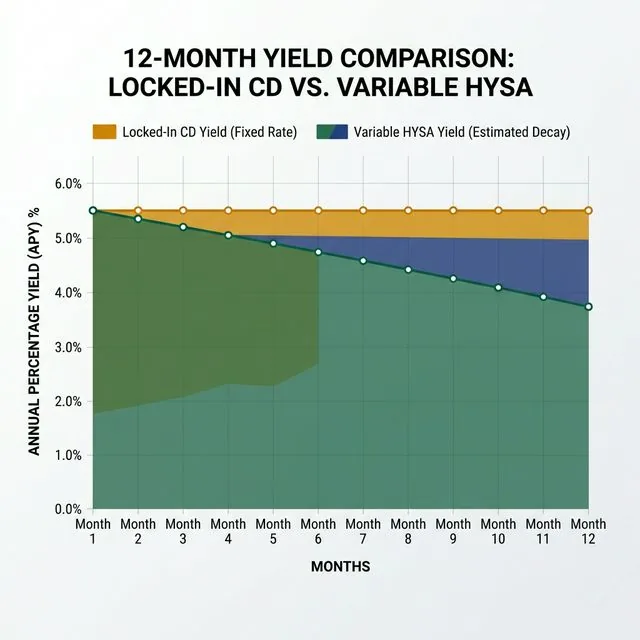

If David leaves his money there on “autopilot,” his average blended yield for the year won’t be 4.65%. As the bank slices his rate down to 3.65% over the next 8 months, his blended return will likely hover around $1,850.

Now, imagine David was proactive. He moves that same $45,700 into an 11-month “No-Penalty” CD or a standard 12-month CD yielding 4.50% Fixed. His guaranteed return? Exactly $2,056.

The orange line is your peace of mind. The green decay area represents the “Lazy Tax” you pay for staying in a variable account during a rate-cut cycle.

By refusing to adapt from a variable-defense to a fixed-defense, David is paying a $200+ “Lazy Tax” solely for the privilege of seeing his money listed under the “Savings” tab instead of the “CD” tab.

[!WARNING] Don’t Chase the Big Bank Trap: If you get frustrated with online banks and move your money back to Chase or Bank of America, you are committing financial self-sabotage. Their rates are typically 0.01%. A “ghosted” HYSA at 3.9% is still infinitely better than a Big Bank paying nothing.

Part 3: The Defensive Arsenal for 2026

If you want to protect your yield from the upcoming Fed cuts, you have three primary tools. None of them are complicated, but they require you to take 15 minutes of deliberate action this weekend.

Strategy 1: The “No-Penalty” CD

This is the ultimate cheat code for the risk-averse. A No-Penalty Certificate of Deposit gives you a fixed rate for the term (usually 11 months), but allows you to withdraw your entire balance plus interest with zero fees after the first 7 days.

- The Play: You get the fixed yield of a CD with the emergency liquidity of a HYSA. Marcus by Goldman Sachs often leads this category.

Strategy 2: The classic “CD Ladder”

If you don’t need the cash tomorrow, don’t lock it up all at once. Take your $30,000 and divide it:

- $10,000 in a 6-month CD

- $10,000 in a 9-month CD

- $10,000 in a 12-month CD

- The Play: As rates fall, you have locked in today’s high yields. Yet, every three months, a chunk of your money “matures” and becomes liquid again if you need it.

Strategy 3: Treasury Bills (T-Bills)

If you live in a high-income tax state (like California or New York), buying 4-week or 8-week Treasury Bills directly through TreasuryDirect.gov or your brokerage is mathematically superior.

- The Play: T-Bill interest is exempt from state and local taxes. A 4.3% T-Bill can essentially equal a 4.8% HYSA depending on your state bracket.

The Daily Fiscal Verdict

We’ve been spoiled for two years. Making 5% on cash by doing absolutely zero work created a false sense of security. But the era of the “Set It and Forget It” HYSA is closing temporarily.

The banks are aggressively managing their balance sheets to protect their profit margins ahead of the Fed’s 2026 pivot. If you aren’t managing your own balance sheet with the same ruthless efficiency, your wealth is leaking out the back door.

Transition your core emergency cash. Lock in a fixed rate. Stop letting the banks ghost your growth.

Your 3-Step Cash Flow Optimization

- Define Your Liquid Need: Determine exactly how much cash you must have accessible within 24 hours. (Usually 1 month of expenses). Keep this in your HYSA.

- Audit the Rest: Take the remaining “lazy cash” and run it through our HYSA vs. CD Calculator to see the exact dollar amount you are risking.

- Execute the Lock-In: Open a No-Penalty CD or standard fixed CD for the “lazy cash” portion. Most platforms let you fund it directly from your existing HYSA with two clicks. Make sure to select “Do Not Auto-Renew” at maturity so the funds revert back to your control next year.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Investing

Investing Fed Pivot Warning: Lock In CD Rates Before They Drop

The Fed's next move will crater HYSA rates overnight. Here's the exact CD ladder strategy to lock in today's near-peak yields for the next 2-3 years.

Investing

Investing SoFi vs Wealthfront (2026): Cash + Investing in One Place?

SoFi bundles checking, savings, and investing. Wealthfront automates your taxes. We compare both to find which all-in-one financial platform wins in 2026.

Investing

Investing RSU Taxes 2026: What You Actually Keep After the IRS

RSUs look like free money until they vest and the tax bill arrives. Here's exactly how RSU taxation works, what your take-home actually is, and how to plan for the bill.