Closing Your Oldest Credit Card Is a Mistake: Here's Why

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Why Closing Your Oldest Credit Card is a $5,000 Mistake You’re About to Make

It happens every Spring. You open your wallet (or your banking app), see that clutter—that old Gap card from 2018, the student credit card with a measly $500 limit—and you think, “I should clean this up.”

It feels responsible. It feels like “decluttering.”

But in the eyes of the FICO algorithm, you aren’t tidying up. You are erasing your history.

I’ve analyzed credit reports for clients who “cleaned house” before applying for a mortgage, only to find their scores drop 40 points overnight, pushing their interest rate up by 0.5%. On a $400,000 home, that mistake costs roughly $61,000 over the life of the loan. Even on a modest $25,000 auto loan, the difference between “Excellent” and “Fair” credit is easily $5,200 in interest.

[!NOTE] Quick Takeaways:

- Age Matters (15%): Your “Length of Credit History” is a key pillar of your score. Closing your oldest account shortens your average age.

- The Utilization Trap (30%): When you close a card, you lose its credit limit. This instantly spikes your utilization ratio on remaining balances.

- The “Memory” Myth: FICO scores count closed accounts for 10 years, but VantageScore (Credit Karma) often drops them immediately, causing panic.

- The Solution: Don’t close it—“Sock Drawer” it.

- Exception: If the card charges an annual fee you aren’t using, close it. Financial bleeding is worse than a temporary score drop.

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

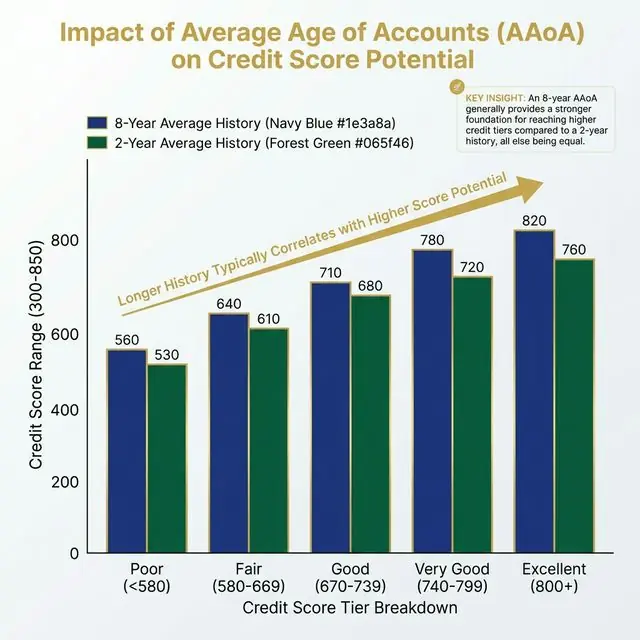

Part 1: The Math of “Credit Age” (Why Time is Money)

Credit scores are designed to predict one thing: Stability.

Lenders love boring people. They love people who have had the same job for 10 years, lived in the same house for 10 years, and kept the same credit card open since college.

Your FICO score calculates your “Length of Credit History” (15% of your total score) based on two factors:

- Age of Oldest Account: How long have you been in the game?

- Average Age of Accounts (AAoA): The mathematical average of every open trade line on your report.

The “New Card” Dilution Problem

Let’s say you have two credit cards:

- Card A (Old): 10 years old

- Card B (New): 2 years old

- Average Age: (10 + 2) / 2 = 6 Years.

6 years is a solid, respectable credit age. It signals “Mature Borrower.”

Now, you decide to close Card A because you “don’t use it anymore.”

- New Oldest Account: 2 years

- New Average Age: 2 years

You just went from a “Stable 6-Year Borrower” to a “Newbie 2-Year Borrower” in the blink of an eye.

Data Note: While FICO models may keep the closed account in your “Average Age” calculation for up to 10 years, newer models and VantageScore (used by landlords and some auto lenders) often drop it immediately. Why take the risk?

Part 2: The Utilization Trap (The Hidden Danger)

Here is where most people get burned. The bigger danger isn’t actually the “Age” drop—it’s the Utilization Spike.

Credit Utilization makes up 30% of your score. It is simply: Total Debt / Total Limit.

The Scenario:

- Card A (Old & Empty): $5,000 limit, $0 balance.

- Card B (Daily Driver): $5,000 limit, $2,000 balance.

- Total Profile: $10,000 limit, $2,000 debt.

- Utilization: 20% (Excellent).

You close Card A.

- New Limit: $5,000.

- New Debt: $2,000.

- New Utilization: 40% (Danger Zone).

Without spending a single extra dollar, you just crossed the threshold from “Responsible User” (<30%) to “High Risk User” (>30%). This single move can drop a score by 40-60 points in one billing cycle.

Part 3: The “Sock Drawer” Strategy (The Fix)

So, you have a card you hate. Maybe the rewards suck. Maybe the app is glitchy. You don’t want to use it, but you don’t want to tank your score.

In 2026, the savvy move is the “Sock Drawer Strategy.”

- Set up a “Micro-Subscription”: Put a tiny, recurring charge on the card. Think iCloud ($0.99/mo) or Netflix ($15/mo).

- Enable Auto-Pay: Set the card to automatically pay the full statement balance from your checking account every month.

- Destroy the Plastic: Cut the card up. Throw it away.

- Ignore It: The card is now a “Credit Age Anchor.” It sits in the background, aging like fine wine, adding positive payment history every single month, keeping your utilization low, and costing you zero mental energy.

Banks will eventually close accounts for inactivity (usually after 12-24 months of silence). The micro-subscription prevents this “Inactivity Closure.”

Part 4: When Should You Actually Close a Card?

I’m a “Fiscal Realist,” not a hoarder. There are two scenarios where closing a card is the smart move, regardless of the score impact.

1. The Annual Fee Bleed

If you have an old Amex Platinum or Chase Sapphire Reserve costing you $695 or $550 a year, and you aren’t using the benefits? Close it.

Paying $700 a year just to keep your credit score 10 points higher is bad math. The interest you save on a future loan likely won’t outweigh the guaranteed cash loss of the annual fee over 5 years.

- Pro Tip: Before closing, ask for a “Downgrade.” Most banks will let you swap a premium card for a no-fee version (e.g., Chase Sapphire to Chase Freedom) to keep the history alive without the fee.

2. The Predatory Lender

If you have a “Credit Repair” card from a subprime lender (like Credit One or First Premier) that charges monthly maintenance fees or “processing fees” just to pay your bill? Burn it. These cards are financial parasites. Get rid of them, take the temporary score hit, and rebuild with a reputable secured card from Capital One or Discover.

The Daily Fiscal Verdict

Your credit history is an asset, just like your 401k or your home equity. You wouldn’t burn down 10% of your house just because “you don’t use that room anymore.”

Before you click “Close Account,” run the numbers:

- Will my utilization spike above 30%?

- Is this my oldest account?

- Does it cost me $0 to keep it open?

If the answer to #3 is “Yes,” then put the scissors down. Put the card in a drawer, set up a $1 autopay, and let it work for you in silence. Your future mortgage rate will thank you.

Your Action Plan

- Audit Your Wallet: Identify your oldest card.

- Check the Fee: Is there an annual fee? If yes, call to downgrade to a no-fee version. Our best credit cards 2026 guide lists the strongest no-fee options worth downgrading to.

- Calculate Utilization: If you close it, will your remaining utilization jump?

- Execute: If it’s free, put your Netflix subscription on it today and set up autopay.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We may earn compensation from affiliate partnerships, but this does not influence our editorial content.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Personal Finance

Personal Finance Raise Your Credit Score 50 Points in 30 Days (Proven)

One method — the AZEO (All Zero Except One) technique — can move a 650 FICO score into the 700s within 30 days without opening a new card.

Personal Finance

Personal Finance Credit Karma vs Real FICO (2026/2027): Costly Score Illusion

Thinking of buying a home or car? Your Credit Karma score could be off by 50 points. Here is the exact mathematical difference and what lenders actually see.

Personal Finance

Personal Finance 7 Credit Score Myths That Are Hurting Your FICO

Checking your own score does NOT hurt it. Carrying a balance does NOT help it. These popular myths are silently sabotaging credit scores across the country.