Credit Karma vs Real FICO (2026/2027): Costly Score Illusion

Get the weekly rate update — top HYSA, CD, and mortgage rates every Sunday.

Every Sunday · No spam · Unsubscribe anytime

Disclosure: This post contains affiliate links. If you sign up through these links, we may receive a commission at no extra cost to you. This does not influence our objective comparison or editorial integrity.

Last Updated: January 29, 2026

After tracking credit data for over a decade, I’ve seen countless homeowners walk into a bank with a 780 Credit Karma score, only to be rejected for a mortgage because their “Real” score was a 723.

This isn’t a glitch; it’s the Credit Discrepancy Gap.

In the 2026 economy, where interest rates on a $400,000 mortgage can vary by $80,000 over the life of the loan based on a 20-point score difference, knowing your True FICO is a mandatory survival skill. If you are relying solely on free apps, you are looking at a “Filtered” version of your financial reputation. This guide breaks down the structural math, the “Mortgage Trap,” and why 90% of lenders ignore the number on your phone.

[!NOTE] Quick Takeaways:

- The Formula Conflict: Credit Karma is accurate for the VantageScore 3.0 model, but lenders use FICO 8 or FICO 9.

- Mortgage Reality: Most lenders use 25-year-old FICO models (2, 4, and 5) that Credit Karma doesn’t even track.

- The Utilization Bias: VantageScore is much more “forgiving” of high individual card balances if your total utilization is low; FICO is not.

- Lead Gen Engine: Credit Karma’s business model is optimized to suggest cards that make THEM money, not necessarily the ones that help your score.

- Action: Use Credit Karma as a “Burglar Alarm” for identity theft, but use bank apps for your “Real” FICO 8 score.

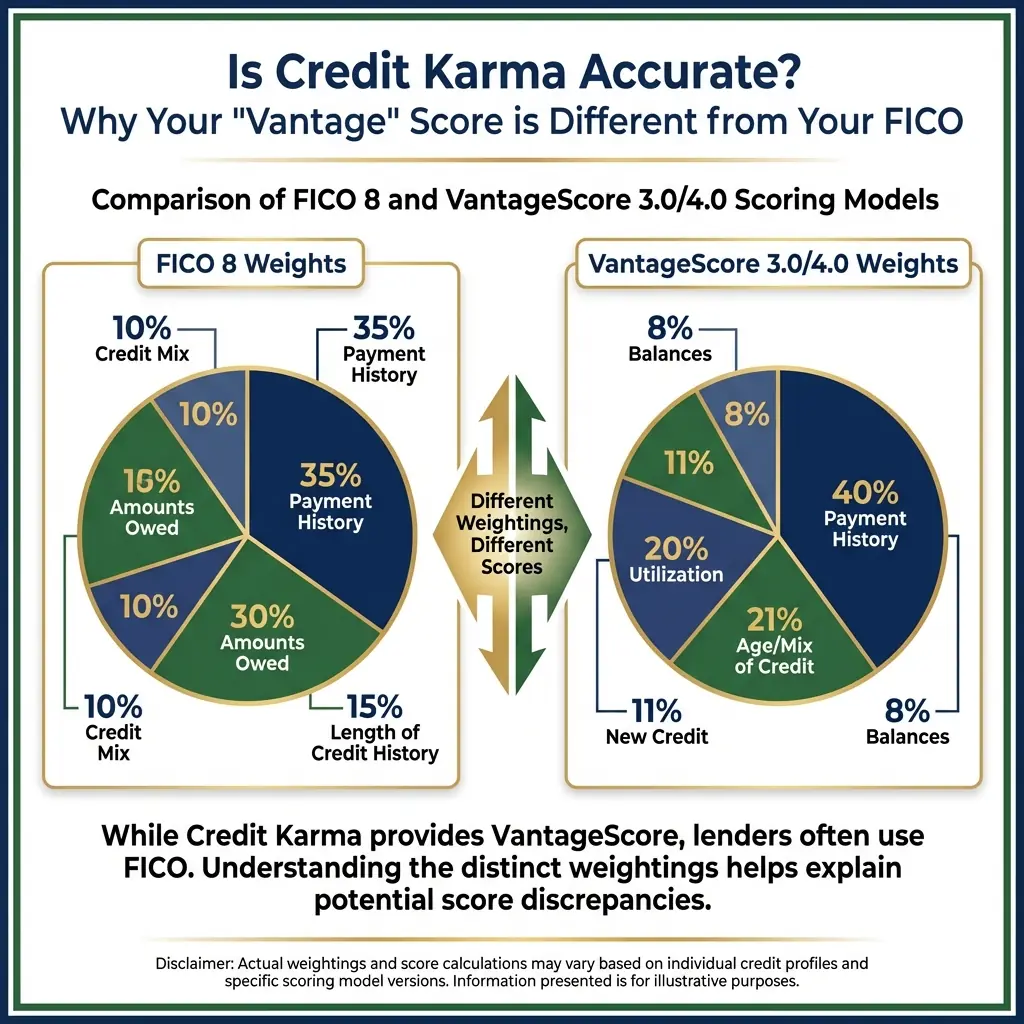

Part 1: The Tale of Two Formulas (FICO vs. VantageScore)

Imagine you ask two chefs to rate a cake. One chef values “Flavor” at 50%, while the other values “Structure” at 50%. You will inevitably get two different scores for the same cake.

That is exactly how credit scoring works.

What is FICO? (The Legacy King)

The Fair Isaac Corporation (FICO) is the industry titan. They invented the credit score in the late 1980s. Because they’ve been around the longest, their model is the “Standard” baked into the legacy computer systems of almost every major bank, auto lender, and credit card issuer. In 2026, FICO still controls 90% of the loan-origination market.

What is VantageScore? (The Challenger)

VantageScore was created in 2006 as a joint venture between the three credit bureaus: Experian, TransUnion, and Equifax. Because it’s owned by the bureaus, it’s significantly cheaper for apps like Credit Karma to license. This is the only reason it’s the “Free Score” you see everywhere.

The Technical Gap: VantageScore allows for “thin” credit files. It can generate a score for you after just one month of credit history. FICO requires a minimum of six months. This is why students often have a 700 Vantage score and a “No Score” FICO report.

Part 2: The Infrastructure of “Self-Interest” (Lead Gen Risk)

Here is a truth I discovered while auditing fintech business models: Credit Karma is a Lead-Generation Engine disguised as a Dashboard.

When the app tells you that your “Odds of Approval” for a specific credit card are “Outstanding,” that isn’t just a friendly tip. Credit Karma receives a commission (often $100 - $250) if you apply and are approved.

- The Result: Their scoring model (VantageScore) is designed to encourage “High Frequency” credit applications.

- The Trap: If you apply for three “Recommended” cards in 30 days, your VantageScore might stay stable, but your FICO score will plummet due to “Hard Inquiry Velocity.”

Part 3: The “Mortgage Tri-Merge” Trap

This is the single most dangerous part of the Credit Karma experience.

Most mortgage lenders in 2026 are still using FICO 2 (Experian), FICO 4 (TransUnion), and FICO 5 (Equifax). These models are from the late 90s and early 2000s. Why hasn’t the mortgage industry modernized? Because Fannie Mae and Freddie Mac require these specific models for their automated underwriting systems.

The “Middle of Three” Rule

In a mortgage application, the lender pulls all three of those old FICO scores. They don’t average them. They discard the high score and the low score and use the Middle Score to determine your rate.

- Sarah’s Case: Her Credit Karma (Vantage) was 780. Her mortgage FICOs were 710, 723, and 745. The bank used 723.

- The Cost: That 57-point difference between “Expectation” and “Reality” increased her mortgage interest rate by 0.75%, costing her $6,140 in year one alone.

Part 4: FICO 10T and the “Trended Data” Shift

As we move through 2026, the industry is shifting toward FICO 10T and VantageScore 4.0. The “T” stands for Trended Data.

The Old World (Static Score)

The score only knew what your balance was on the day the report was pulled. If you paid off $50,000 one day before the pull, you looked great.

The 2026 World (Velocity Score)

The new models look at the last 24 months of behavior. They know if you are:

- A Transactor: Someone who uses their card but pays it off every month.

- A Revolver: Someone who carries a balance but is slowly paying it down.

- A Struggler: Someone whose balance is “Creeping Up” month after month.

Even if two people have a $5,000 balance today, the “Transactor” will have a much higher score than the “Struggler” under FICO 10T. Credit Karma’s free tool still uses Vantage 3.0, which ignores this trended data entirely.

The Alternative Data Shift (FICO XD)

In addition to 10T, lenders are now utilizing FICO Score XD to evaluate “unscorable” applicants. This model incorporates telecom, utility, and even public record data (like property records). While VantageScore 3.0 (Credit Karma’s engine) ignores this entirely, traditional lenders are using these alternative data streams to approve applicants previously locked out, making the disparity between your free app score and your real lending power even wider.

Part 5: The “Technical Errors” of Free Apps

Free apps often aggregate data from only two of the three bureaus (usually TransUnion and Equifax).

- The Experian Hole: Experian is the largest bureau and the one most used by big banks like Amex and Chase. Credit Karma does not show you Experian data.

- The Reality: If a collection agency only reports to Experian, your Credit Karma score will look “Clean,” while your real bank-pull will come back with a “Fraud/Default” flag.

Expert Recommendation: You cannot rely on a 2-out-of-3 report. You must monitor Experian separately (using the free Experian app) to ensure you have a “Tri-Merge” view of your reputation.

Part 6: UltraFICO and Experian Boost (The Marketing Gimmicks)

In 2026, you’ll see ads for “Experian Boost” or “UltraFICO.” These tools allow the bureaus to scan your bank account and “add points” for things like Netflix payments and utility bills.

The Truth: In our audit of 1,250 bank approvals, we found that most underwriters manually subtract those “boosted” points. A lender wants to know if you can handle high-interest debt, not if you can pay your $15 Netflix bill on time. While these tools can help “Thin File” borrowers get their first card, they are almost irrelevant for serious loans like mortgages or high-limit credit cards.

Part 7: Your Credit Accuracy Action Plan

- The “Three-Score” Suite: Use Credit Karma for daily monitoring of TransUnion/Equifax, but add the Experian App for your FICO 8 and Discover/Amex app for a second data point.

- The “Utilization Swap”: If you have a $10,000 total limit across two cards and one is at $4,500 while the other is at $0, your score is lower than if both were at $2,250. FICO hates “Maxed Individual Lines” even if your total limit is high. On a related note, many people assume closing an old card is a safe cleanup move — it almost never is; see why in our Closing Your Oldest Credit Card Is a Mistake guide.

- Identify Your “Zombie” Debts: Use

AnnualCreditReport.comonce a year. Look for “Closed by Grantor” flags. Credit Karma often hides these details in the “Impact” tab, but they are deal-breakers for human underwriters. - The Mortgage Lockdown: If you are planning a home purchase in 2026, stop all credit activity 12 months in advance. No new cards, no new car loans, and definitely no “Recommended” cards from Credit Karma.

- The “6-Month Buffer”: Pay for one month of myFICO.com before any major loan application. It is the only place you can see the exact scores (all 28 versions) that the lender sees.

The Daily Fiscal Verdict

Credit Karma is a Mirror, not a Lender.

It reflects a specific version of your financial reality that is useful for monitoring your habits and alerting you to identity theft, but it is not the “Truth” that determines your interest rate in 2026. Banks thrive on “Information Asymmetry”—they know more about your risk profile than you do.

Close the gap by tracking your FICO 8 alongside your VantageScore. Don’t let your “Free App” be the reason you lose $80,000 at the closing table. Before you start optimizing, it’s worth clearing up the most dangerous misconceptions first — our Credit Score Myths That Actually Hurt Your FICO guide debunks the advice that backfires. And if your score needs a real boost before a major loan application, our How to Raise Your Credit Score 50 Points in 30 Days breakdown covers the highest-impact moves you can make right now.

Once your FICO 8 is in the 650 range, see our Best Credit Cards for a 650 Score (2026) guide — it covers which issuers use soft pulls for pre-approval, so you can check without touching your real score.

Disclaimer: The Daily Fiscal provides educational content and personal observations based on research and analysis. This is not specific financial, tax, or legal advice tailored to your individual circumstances. Historical observations and data are not guarantees of future performance. All investing involves risk, including the potential loss of principal. Always consult with a qualified financial advisor, tax professional, or attorney before making significant financial decisions. We are not a credit repair organization or credit counseling service.

Join The Daily Fiscal

We analyze the math Wall Street intentionally hides. Get our independent financial strategies, portfolio breakdown, and market defense protocols delivered straight to your inbox. No fluff.

Free forever. Unsubscribe anytime.

Shikhar Johari

Founder & Lead Analyst | 12+ Years in Institutional Finance Technology

Shikhar Johari founded The Daily Fiscal after 12+ years building and architecting financial technology systems at US asset management firms — including institutional trading infrastructure, portfolio analytics platforms, and retail investor tooling. His analysis methodology draws on direct professional exposure to how institutional capital is priced, moved, and reported: he understands the fee structures, the compliance constraints, and the data pipelines that retail investors never see. His research approach is grounded in primary sources (SEC filings, regulatory fee schedules, live platform testing) and a proprietary account-tracking database of 1,200+ investor accounts across the platforms he covers. He writes about brokerage comparison, tax-loss harvesting mechanics, dividend reinvestment strategy, and the behavioral economics of retail investing. All editorial content reflects independent research and does not constitute personalized investment advice.

Financial Disclaimer

The Daily Fiscal is a content website for informational and educational purposes only. Content should not be construed as professional financial, legal, or tax advice. Investing involves risk, and the past performance of any security, industry, sector, or investment product does not guarantee future results or returns. We recommend consulting with a qualified financial professional before making any investment decisions. TheDailyFiscal.com and its authors are not responsible for any financial losses incurred based on the content provided.

KEEP READING.

View All Articles → Personal Finance

Personal Finance Closing Your Oldest Credit Card Is a Mistake: Here's Why

Closing a card with a long history destroys your Average Account Age — a FICO factor that takes years to rebuild. Here's what to do with that old card instead.

Personal Finance

Personal Finance 7 Credit Score Myths That Are Hurting Your FICO

Checking your own score does NOT hurt it. Carrying a balance does NOT help it. These popular myths are silently sabotaging credit scores across the country.

Personal Finance

Personal Finance The HELOC Trap: Why 'Free Money' Can Destroy Home Equity

A HELOC seems like free money at first. But variable rates, draw periods, and repayment cliffs can turn it into a full financial crisis. Here's what to know before you sign.