Credit Card Guides

Card-by-card comparisons ranked by your actual spending, credit score improvement guides, and the debt payoff math that banks hope you never see.

How We Evaluate Credit Cards

We calculate rewards on a real $3,500/month spending budget across grocery, gas, dining, and travel. We don't just list sign-up bonuses — we calculate the net value after annual fees over a 2-year horizon. A card advertising "$750 cash back" may net you $150 in year 2 after the $599 fee is deducted.

For credit score guides, we use real FICO methodology — not credit karma estimates. The AZEO method, the utilization cliff at 30%, and the AAoA impact of closing old cards are all tested against confirmed FICO scoring models. No guesswork.

Essential Credit Guides

Credit FAQ

How do I choose the best credit card for my spending?

The best card depends on your largest monthly expense. If you spend heavily on groceries and dining, a tiered rewards card like the Amex Gold or SavorOne is best. For general spending, a flat 2% cash back card simplifies your rewards.

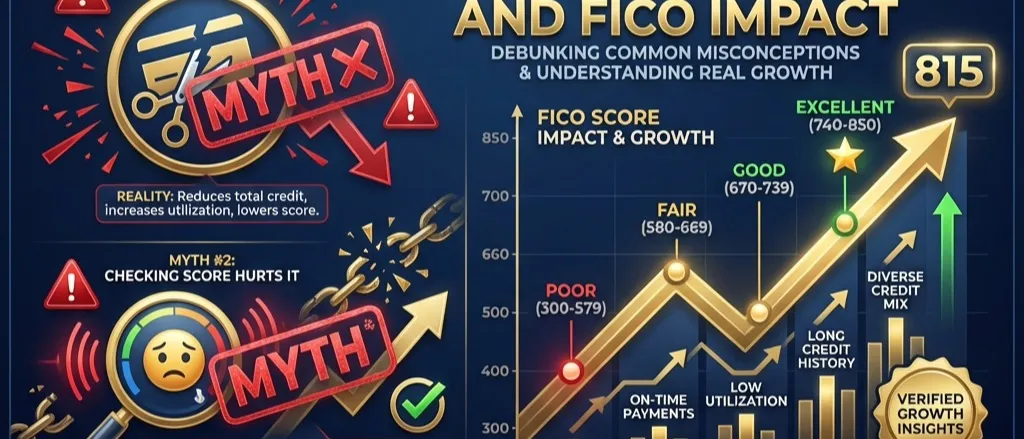

Does carrying a balance on my credit card help my score?

No. This is a common myth. Carrying a balance only results in high interest charges. The best way to build credit is to pay your balance in full every month, which maintains a low credit utilization ratio.

Should I close a credit card I no longer use?

Generally, no — especially if it's one of your oldest accounts. Closing a card can reduce your average age of accounts and your total available credit, both of which can negatively impact your FICO score.

All Credit Guides

15 guides Credit Cards

Credit Cards Best Credit Cards 2026: Every Category, Ranked

The best credit card for travel, cash back, balance transfers, no credit, and business in 2026. We tested 20 cards. Full comparison table and picks inside.

Credit Cards

Credit Cards Best Travel Credit Cards 2026: Points Value Ranked

We ranked 8 travel credit cards by actual points value, not bonus hype. Chase Sapphire Preferred wins for most. Full redemption math and head-to-head inside.

Personal Finance

Personal Finance Best Credit Cards for No Credit History 2026

No credit? No problem. Best starter cards: Discover it Secured (2% cash back), Capital One Platinum (no fee), Petal 2 (1.5% after 12 months). How to build from 0 to 700 in 18 months.

Personal Finance

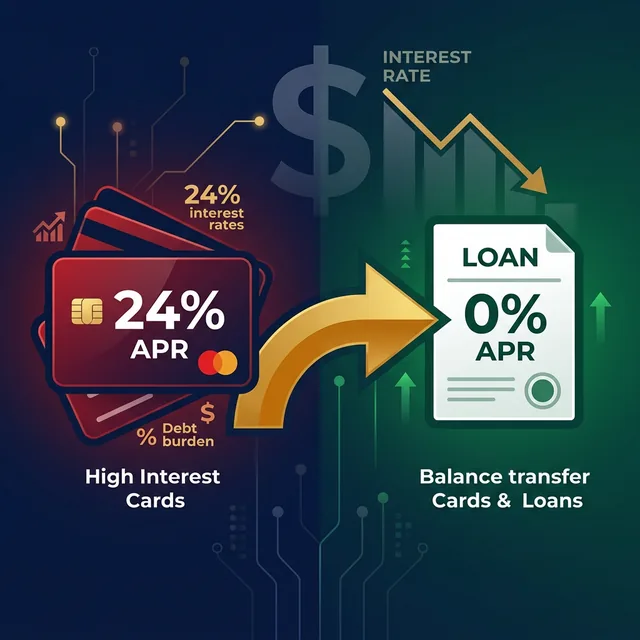

Personal Finance Balance Transfer vs Personal Loan 2026: Pay Off Debt Faster

We ran the full interest math on a 0% APR balance transfer vs a fixed-rate personal loan. The winner depends entirely on your repayment timeline and discipline.

Personal Finance

Personal Finance Costco Anywhere Visa Review 2026: Is the Reward Still #1?

If you spend $300+ at Costco monthly, the Citi Costco Anywhere Visa outperforms most premium travel cards purely on rewards math. Here's the full breakdown.

Personal Finance

Personal Finance Secured vs Unsecured Cards (2026): Which Rebuilds Credit?

A secured card isn't always worse than unsecured. We compare interest rates, graduation timelines, and credit bureau reporting quality for credit rebuilders.

Investing

Investing Venture X vs Sapphire Reserve (2026): $395 vs $550 Decision

Venture X costs $155 less per year. Does Chase Sapphire Reserve justify the gap with better lounge access and travel credits? We did the numbers.

Personal Finance

Personal Finance Best No-Fee Cash Back Cards (2026): Zero-Cost Rewards

We calculated actual cash back on a $3,500/month budget across grocery, gas, and dining. These zero-fee cards outperform most premium cards.

Personal Finance

Personal Finance Closing Your Oldest Credit Card Is a Mistake: Here's Why

Closing a card with a long history destroys your Average Account Age — a FICO factor that takes years to rebuild. Here's what to do with that old card instead.

Personal Finance

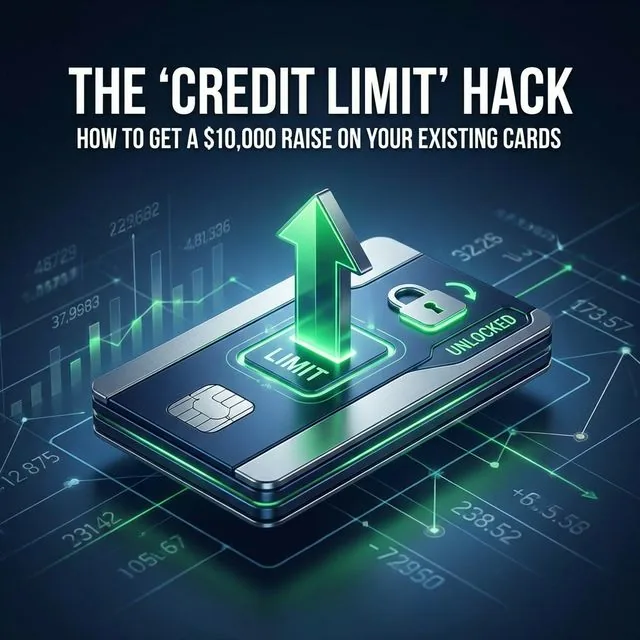

Personal Finance How to Get a Credit Limit Increase in 2026 (The Script)

The timing and phrasing of your credit limit request matters more than most people realize. Here's the script — and the exact timing — that consistently gets approved.

Personal Finance

Personal Finance Raise Your Credit Score 50 Points in 30 Days (Proven)

One method — the AZEO (All Zero Except One) technique — can move a 650 FICO score into the 700s within 30 days without opening a new card.

Credit Cards

Credit Cards Amex Gold vs Chase Sapphire Preferred (2026): Which Wins?

Both charge around $250/year. Both offer strong travel and dining perks. But the math on real-world spending rewards only works in one direction.

Personal Finance Best Credit Cards for a 650 Credit Score (2026/2027)

650 FICO qualifies for unsecured rewards cards. Top picks: QuicksilverOne (1.5% back), Discover it (5% rotating). Plus: how to jump to 720 in 6 months.

Personal Finance

Personal Finance Credit Karma vs Real FICO (2026/2027): Costly Score Illusion

Thinking of buying a home or car? Your Credit Karma score could be off by 50 points. Here is the exact mathematical difference and what lenders actually see.

Personal Finance

Personal Finance 7 Credit Score Myths That Are Hurting Your FICO

Checking your own score does NOT hurt it. Carrying a balance does NOT help it. These popular myths are silently sabotaging credit scores across the country.